Question: Hello, I need help with solving this exercise. I know it's long but please explain it as thoroughly as you can. Consider we have the

Hello, I need help with solving this exercise. I know it's long but please explain it as thoroughly as you can.

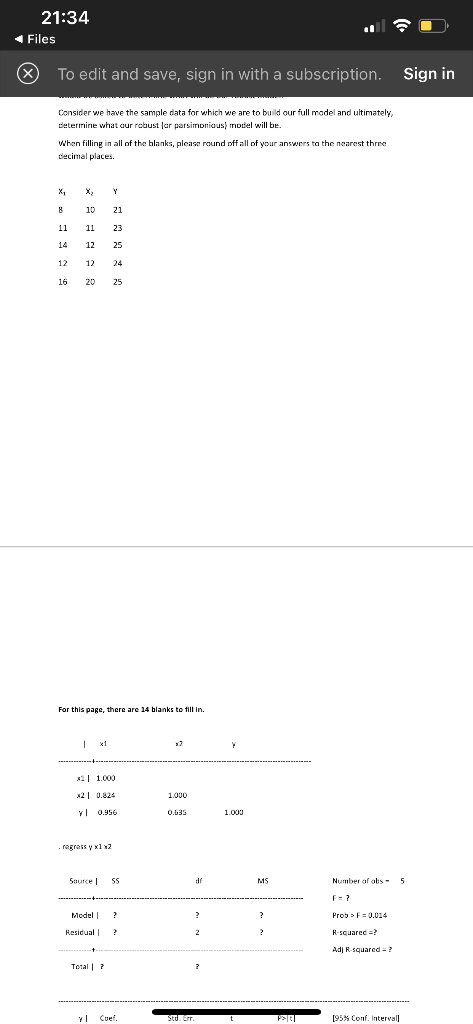

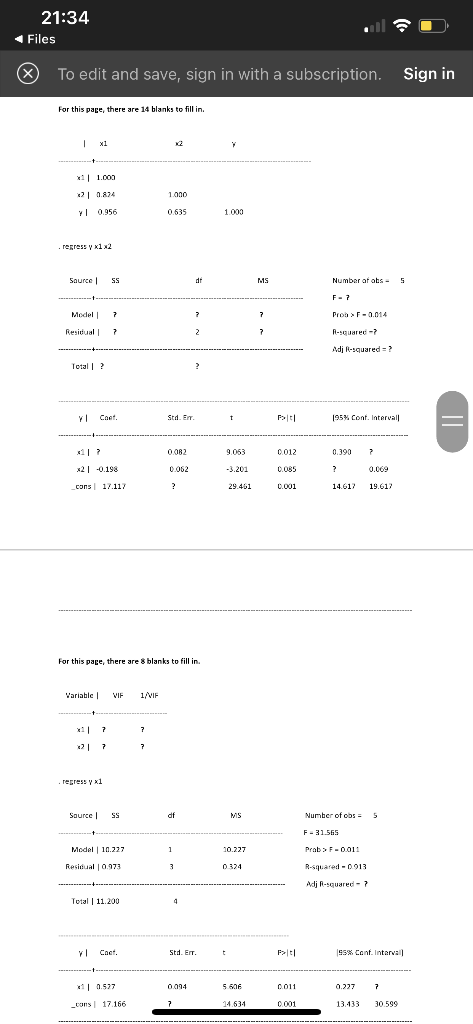

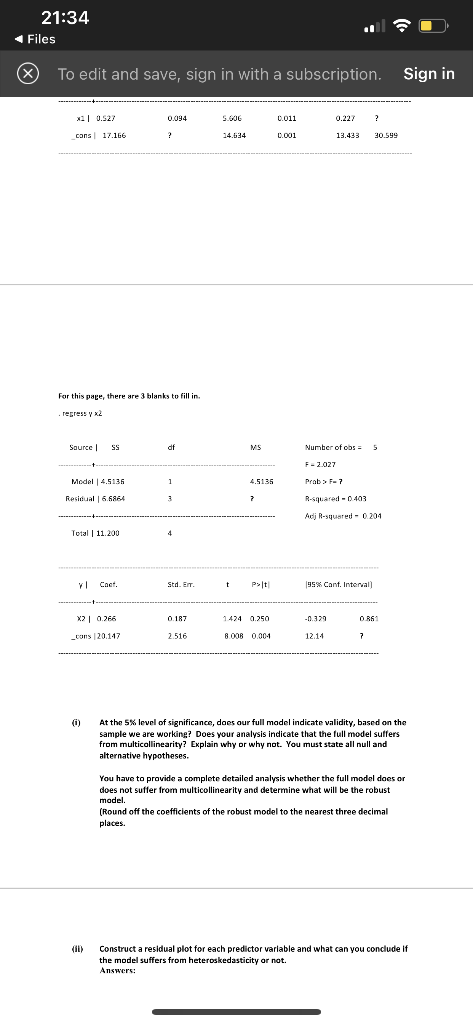

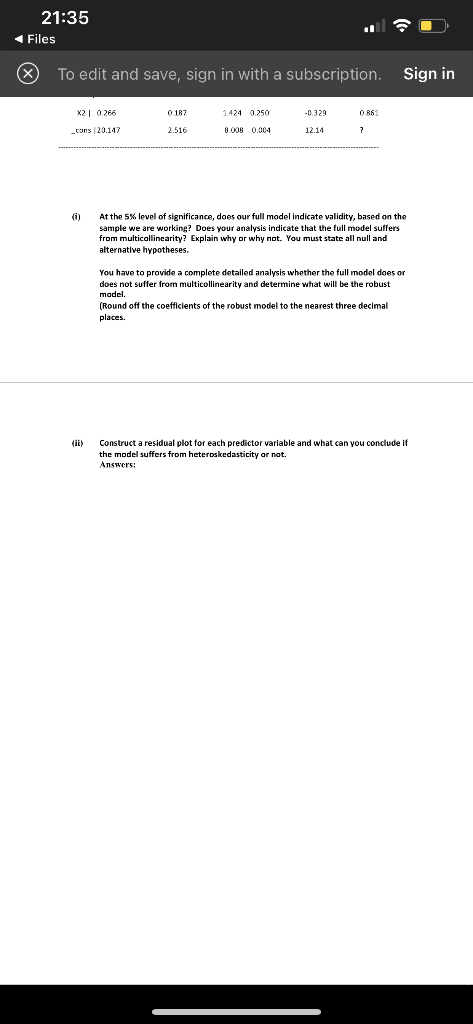

Consider we have the sample data for which we are to buld our full model and ultimately, determine what dur robust \{ar parsimonious\} model will be. When filling in all of the blanks, please round off all of your answers to the nearest three decimal places. For this page, there are 14 blanks to fill in. For this page, there are 14 blanks to fill in. - regrese 712 For this page, there are 8 blanks to fill in. To edit and save, sign in with a subscription. For this page, there are 3 blanks to fill in. . regress 2 (i) At the 5% level of significance, does aur full model indicate validity, based on the sample we are working? Does your analysis indicate that the full model suffers from multicallinearity? Explain why or why not. You must state all null and alternative hypotheses. You have to provide a complete detailed analysis whether the full model does or does not suffer from multicollinearity and determine what will be the robust madel. (Round off the coefficients of the robust model to the nearest three decimal plates. (iii) Construct a residual plot for each predictor variable and what can you conclude if the model suffers from heteroskedasticity ar not. Answers: To edit and save, sign in with a subscription. (i) At the 5% level of significance, does our full model indicate validity, based on the sample we are working? Does your analysis indicate that the full model suffers. from multicallinearity? Explain why or why not. You must state all null and alternative hypotheses. You have to provide a complete detailed analysis whether the full model does or does not suffer from multicollinearity and determine what will be the robust madel. (Round off the coefficlents of the robust model to the nearest three decimal places. (ii) Construct a residual plot for each predictor variable and what can you conclude if the model suffers from heteroskedasticity ar nat. Ansprers: Consider we have the sample data for which we are to buld our full model and ultimately, determine what dur robust \{ar parsimonious\} model will be. When filling in all of the blanks, please round off all of your answers to the nearest three decimal places. For this page, there are 14 blanks to fill in. For this page, there are 14 blanks to fill in. - regrese 712 For this page, there are 8 blanks to fill in. To edit and save, sign in with a subscription. For this page, there are 3 blanks to fill in. . regress 2 (i) At the 5% level of significance, does aur full model indicate validity, based on the sample we are working? Does your analysis indicate that the full model suffers from multicallinearity? Explain why or why not. You must state all null and alternative hypotheses. You have to provide a complete detailed analysis whether the full model does or does not suffer from multicollinearity and determine what will be the robust madel. (Round off the coefficients of the robust model to the nearest three decimal plates. (iii) Construct a residual plot for each predictor variable and what can you conclude if the model suffers from heteroskedasticity ar not. Answers: To edit and save, sign in with a subscription. (i) At the 5% level of significance, does our full model indicate validity, based on the sample we are working? Does your analysis indicate that the full model suffers. from multicallinearity? Explain why or why not. You must state all null and alternative hypotheses. You have to provide a complete detailed analysis whether the full model does or does not suffer from multicollinearity and determine what will be the robust madel. (Round off the coefficlents of the robust model to the nearest three decimal places. (ii) Construct a residual plot for each predictor variable and what can you conclude if the model suffers from heteroskedasticity ar nat. Ansprers

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts