Question: hello I try this but pretty difficult to me , I hope you help me asap. thank you The following balance sheet information is available

hello I try this but pretty difficult to me , I hope you help me asap. thank you

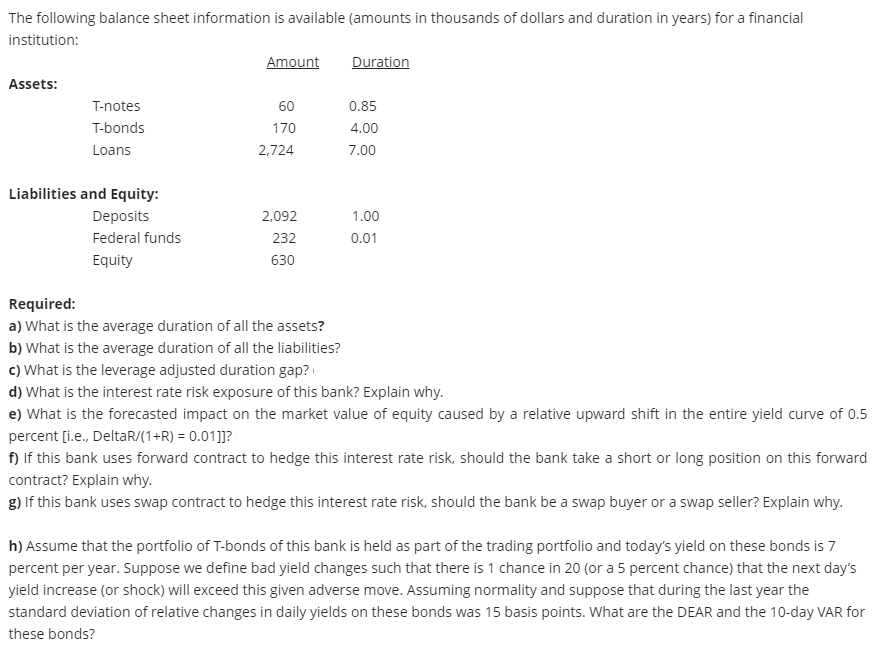

The following balance sheet information is available amounts in thousands of dollars and duration in years) for a financial institution: Amount Duration Assets: T-notes 60 0.85 T-bonds 170 4.00 Loans 2,724 7.00 Liabilities and Equity: Deposits 2,092 1.00 Federal funds 232 0.01 Equity 630 Required: a) What is the average duration of all the assets? b) What is the average duration of all the liabilities? c) What is the leverage adjusted duration gap? d) What is the interest rate risk exposure of this bank? Explain why. e) What is the forecasted impact on the market value of equity caused by a relative upward shift in the entire yield curve of 0.5 percent [i.e., DeltaR/(1+R) = 0.01]]? f) If this bank uses forward contract to hedge this interest rate risk, should the bank take a short or long position on this forward contract? Explain why. g) If this bank uses swap contract to hedge this interest rate risk, should the bank be a swap buyer or a swap seller? Explain why. h) Assume that the portfolio of T-bonds of this bank is held as part of the trading portfolio and today's yield on these bonds is 7 percent per year. Suppose we define bad yield changes such that there is 1 chance in 20 (or a 5 percent chance) that the next day's yield increase (or shock) will exceed this given adverse move. Assuming normality and suppose that during the last year the standard deviation of relative changes in daily yields on these bonds was 15 basis points. What are the DEAR and the 10-day VAR for these bonds

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts