Question: Hello - I'm struggling with the Black-Scholes Model. Please Help! Thank you!!! Problem My Calculations Black-Scholes Model Assume that you have been given the following

Hello - I'm struggling with the Black-Scholes Model. Please Help! Thank you!!!

Problem

My Calculations

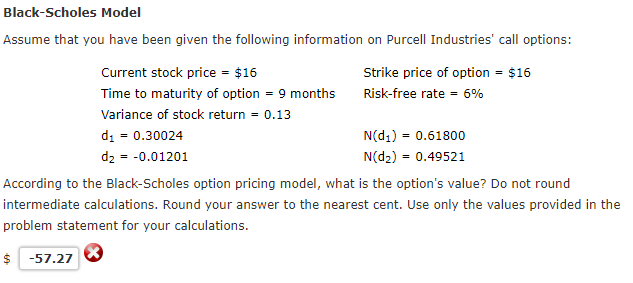

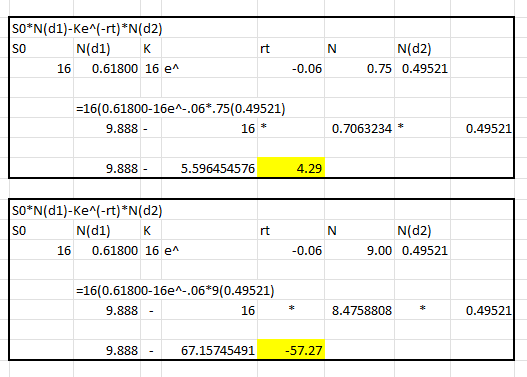

Black-Scholes Model Assume that you have been given the following information on Purcell Industries' call options: Currentstockprice=$16Timetomaturityofoption=9monthsVarianceofstockreturn=0.13d1=0.30024d2=0.01201Strikepriceofoption=$16Risk-freerate=6%N(d1)=0.61800N(d2)=0.49521 According to the Black-Scholes option pricing model, what is the option's value? Do not round intermediate calculations. Round your answer to the nearest cent. Use only the values provided in the problem statement for your calculations

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock