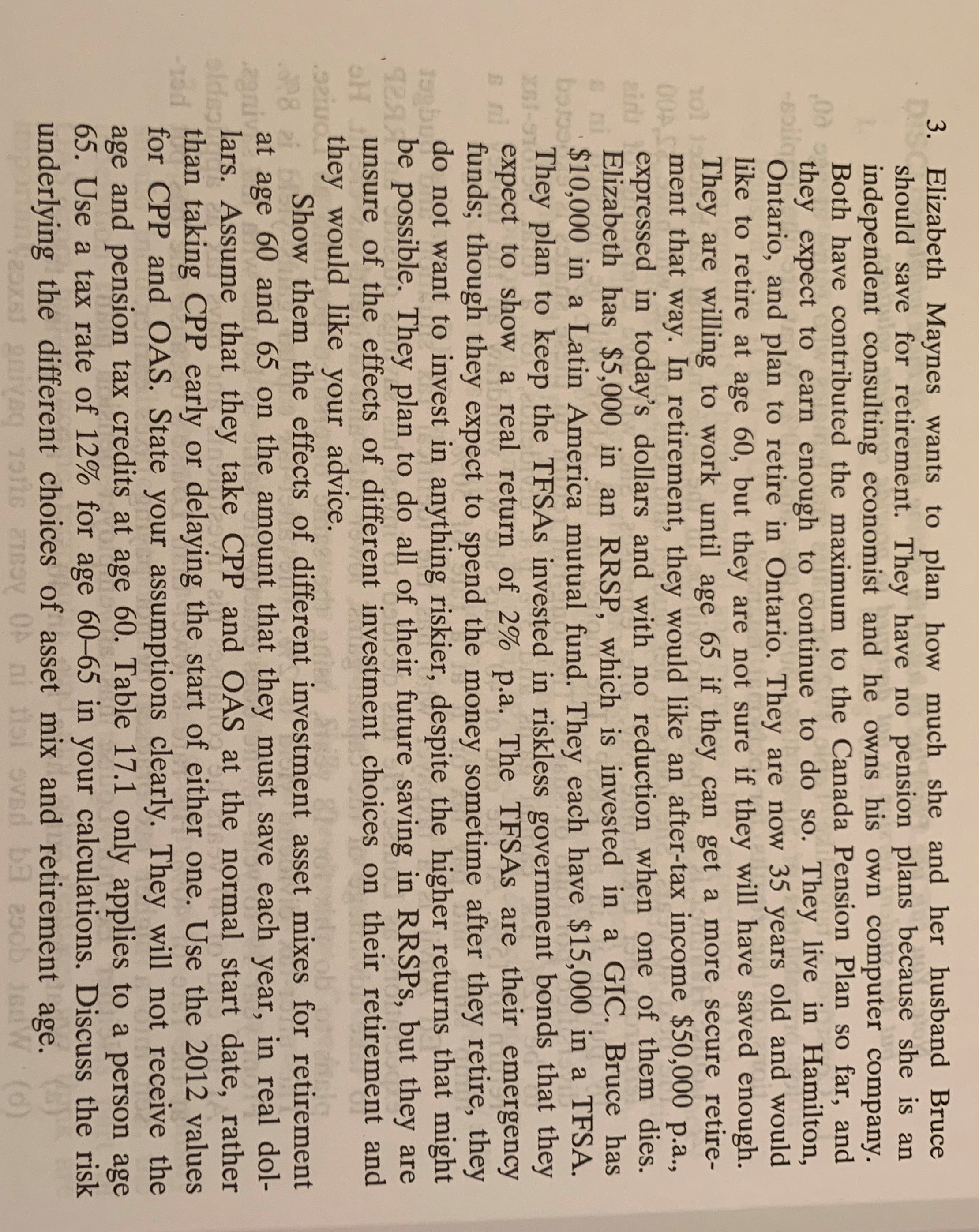

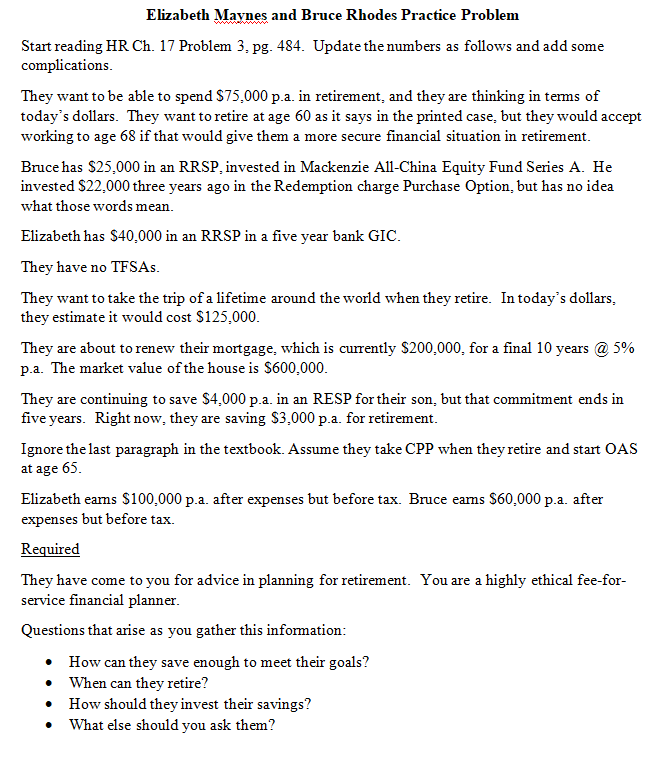

Question: Hello Tutors! Below I have attached a practice problem. However, for this problem there were some alterations that we had to do which I have

Hello Tutors! Below I have attached a practice problem. However, for this problem there were some alterations that we had to do which I have also attached below. I am having real trouble with this mini case. I was wondering if anyone could assist me in solving this problem and explaining the solution? It would really help my understanding and would really appreciate it. This was all the information that was given to us. Thank you.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock