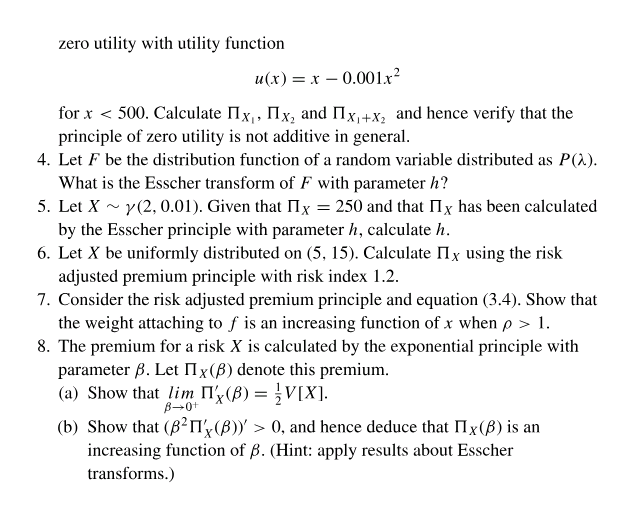

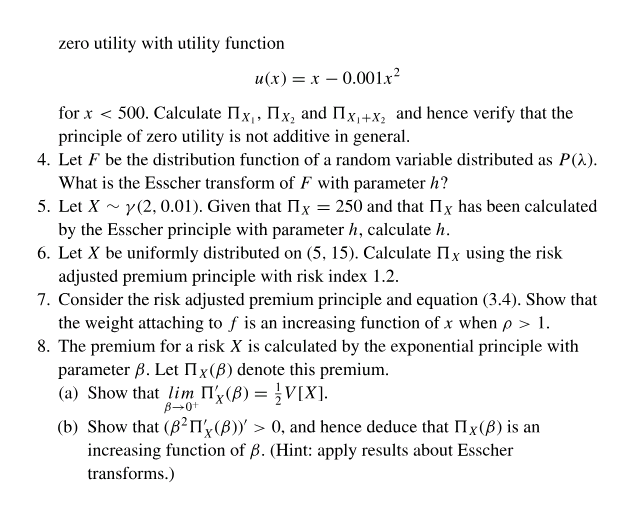

Question: Hello tutors. Help me solve these questions. zero utility,r with utilitv function ctr) = .t - 0.01:]le for x c 500. Calculate 1'] .'r. .

![function ctr) = .t - 0.01:]le for x c 500. Calculate 1']](https://s3.amazonaws.com/si.experts.images/answers/2024/06/66750b9669734_71066750b9656b70.jpg)

Hello tutors. Help me solve these questions.

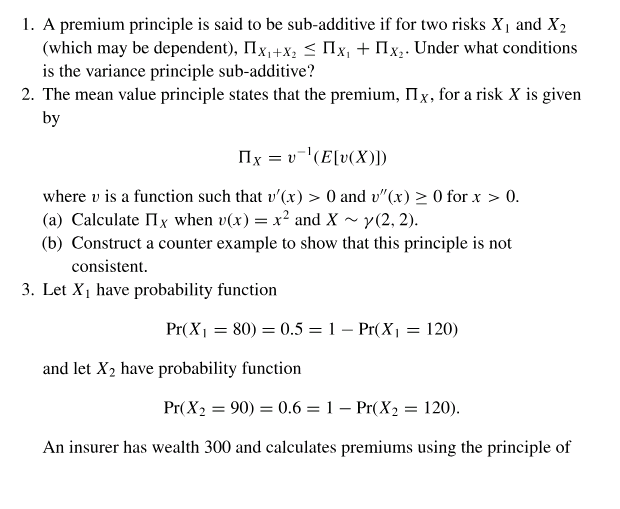

zero utility,r with utilitv function ctr) = .t - 0.01:]le for x c 500. Calculate 1'] .'r. . IT at; and 1'13;J +32 and hence verify that the principle of zero utilityr is not additive in general. 4. Let F be the distribution function of a random variable distributed as PEA}. What is the Esscher transform of F with parameter it? 5. Let X on p12. 0.01). Given that Hg = 25C! and that 11;; has been calculated by the Esscher principle with parameter a, calculate it. ti. Let X be uniformly distributed on {5. 15}. Calculate [I I using the risk adjusted premium principle with risk index 1.2. T. Consider the risk adjusted premium principle and equation (3.4). Show that the weight attaching to f is an increasing function of a: when p a: l. 8. The premium for a risk X is calculated by the exponential principle with parameter ,6. Let 1'] 31:46) denote this premium. (a) Show that ling; I'l'xt) = HX]. {b} Show that {znfpth' a t}, and hence deduce that I'll-{,3} is an increasing function of ,6. (Hint: apply results about Esscher transforms.) 1. A premium principle is said to be sub-additive if for two risks X , and X2 (which may be dependent), Ix,+x, 0 and v"(x) > 0 for x > 0. (a) Calculate IIx when v(x) = x- and X ~ y (2, 2). (b) Construct a counter example to show that this principle is not consistent. 3. Let X1 have probability function Pr(X1 = 80) = 0.5 =1 - Pr(X] = 120) and let X2 have probability function Pr(X2 = 90) = 0.6 = 1 - Pr(X2 = 120). An insurer has wealth 300 and calculates premiums using the principle of

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts