Question: HELP CREATE A CASE BRIEF FOLLOWING FORMAT: FACTS, ISSUE, HOLDING, RATIONALE STATE OF MAINE KENNEBEC, ss. MAINE BOARD OF TAX APPEALS DOCKET NO. BTA-2019-21 [INDIVIDUAL

HELP CREATE A CASE BRIEF FOLLOWING FORMAT: FACTS, ISSUE, HOLDING, RATIONALE

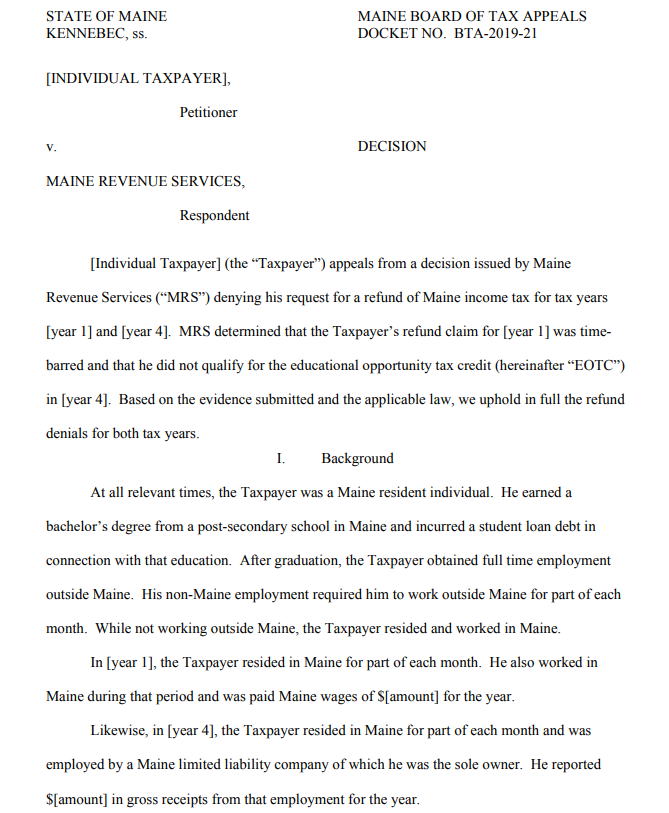

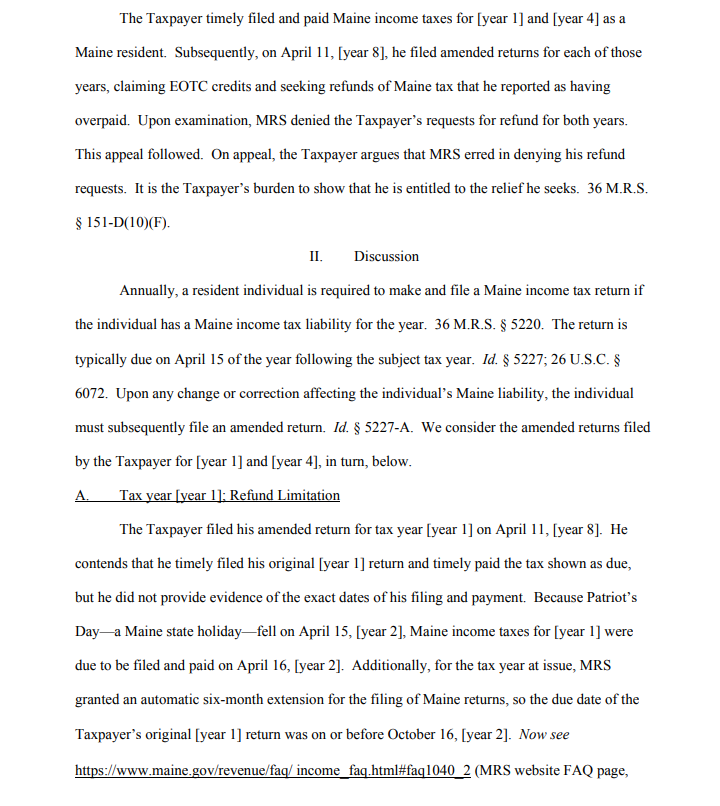

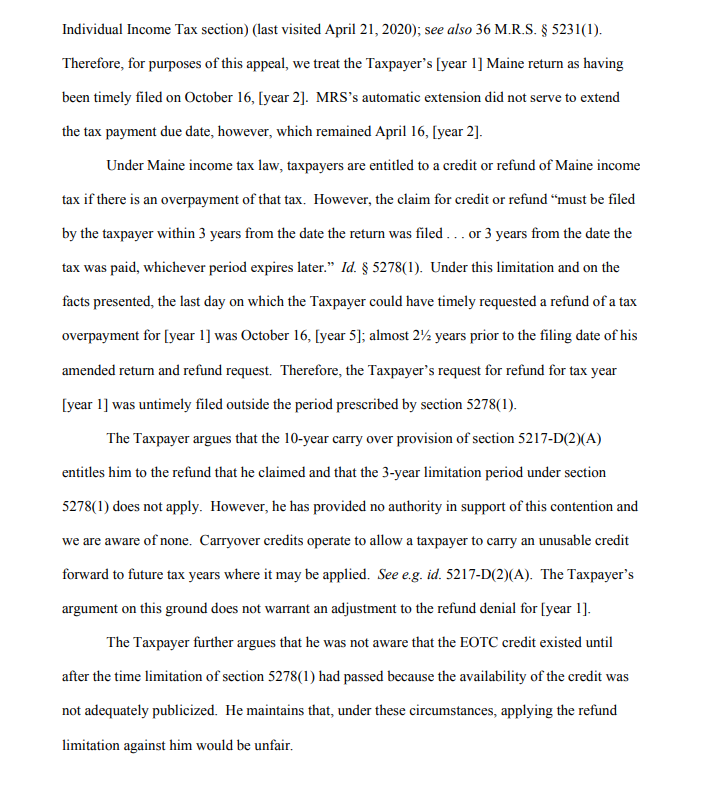

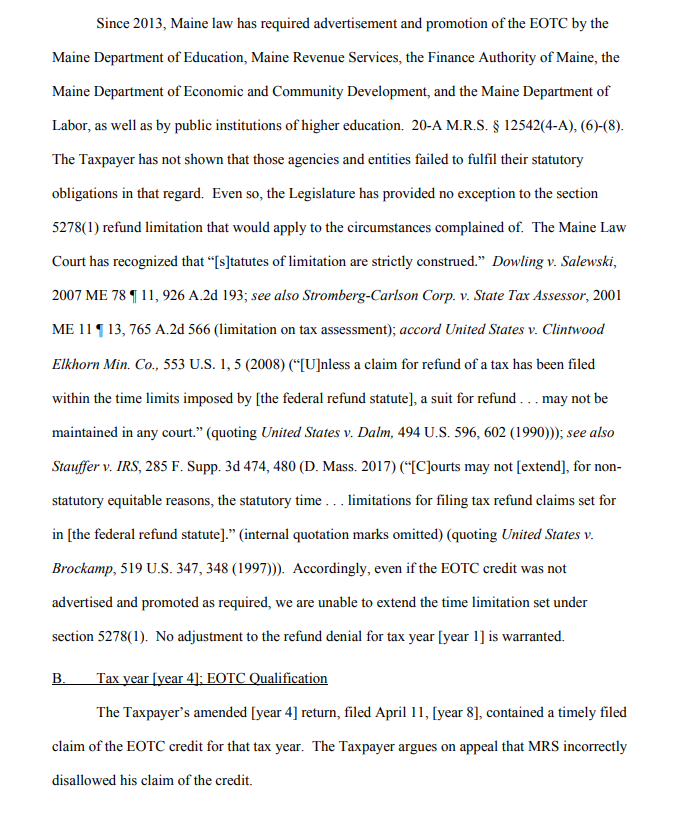

STATE OF MAINE KENNEBEC, ss. MAINE BOARD OF TAX APPEALS DOCKET NO. BTA-2019-21 [INDIVIDUAL TAXPAYER], Petitioner V. DECISION MAINE REVENUE SERVICES, Respondent [Individual Taxpayer] (the Taxpayer) appeals from a decision issued by Maine Revenue Services ("MRS) denying his request for a refund of Maine income tax for tax years [year 1] and [year 4]. MRS determined that the Taxpayer's refund claim for [year l] was time- barred and that he did not qualify for the educational opportunity tax credit (hereinafter EOTC") in [year 4]. Based on the evidence submitted and the applicable law, we uphold in full the refund denials for both tax years. I. Background At all relevant times, the Taxpayer was a Maine resident individual. He earned a bachelor's degree from a post-secondary school in Maine and incurred a student loan debt in connection with that education. After graduation, the Taxpayer obtained full time employment outside Maine. His non-Maine employment required him to work outside Maine for part of each month. While not working outside Maine, the Taxpayer resided and worked in Maine. In [year 1], the Taxpayer resided in Maine for part of each month. He also worked in Maine during that period and was paid Maine wages of S[amount] for the year. Likewise, in [year 4], the Taxpayer resided in Maine for part of each month and was employed by a Maine limited liability company of which he was the sole owner. He reported $[amount] in gross receipts from that employment for the year. The Taxpayer timely filed and paid Maine income taxes for [year l] and [year 4] as a Maine resident. Subsequently, on April 11, [year 8], he filed amended returns for each of those years, claiming EOTC credits and seeking refunds of Maine tax that he reported as having overpaid. Upon examination, MRS denied the Taxpayer's requests for refund for both years. This appeal followed. On appeal, the Taxpayer argues that MRS erred in denying his refund requests. It is the Taxpayer's burden to show that he is entitled to the relief he seeks. 36 M.R.S. $ 151-D(10)(F). II. Discussion Annually, a resident individual is required to make and file a Maine income tax return if the individual has a Maine income tax liability for the year. 36 M.R.S. $ 5220. The return is typically due on April 15 of the year following the subject tax year. Id. 5227; 26 U.S.C. S 6072. Upon any change or correction affecting the individual's Maine liability, the individual must subsequently file an amended return. Id. 5227-A. We consider the amended returns filed by the Taxpayer for [year l] and [year 4], in turn, below. A. Tax year [year 1]: Refund Limitation The Taxpayer filed his amended return for tax year [year 1] on April 11, [year 8]. He contends that he timely filed his original [year l] return and timely paid the tax shown as due, but he did not provide evidence of the exact dates of his filing and payment. Because Patriot's Daya Maine state holiday-fell on April 15, [year 2], Maine income taxes for [year l] were due to be filed and paid on April 16, [year 2). Additionally, for the tax year at issue, MRS granted an automatic six-month extension for the filing of Maine returns, so the due date of the Taxpayer's original [year l] return was on or before October 16, [year 2]. Now see https://www.maine.gov/revenue/faq/income_faq.html#faq1040_2 (MRS website FAQ page, Individual Income Tax section) (last visited April 21, 2020); see also 36 M.R.S. 5231(1). Therefore, for purposes of this appeal, we treat the Taxpayer's [year 1] Maine return as having been timely filed on October 16, [year 2). MRS's automatic extension did not serve to extend the tax payment due date, however, which remained April 16, [year 2). Under Maine income tax law, taxpayers are entitled to a credit or refund of Maine income tax if there is an overpayment of that tax. However, the claim for credit or refund must be filed by the taxpayer within 3 years from the date the return was filed ... or 3 years from the date the tax was paid, whichever period expires later. Id. 5278(1). Under this limitation and on the facts presented the last day on which the Taxpayer could have timely requested a refund of a tax overpayment for [year 1] was October 16, [year 5]; almost 2/2 years prior to the filing date of his amended return and refund request. Therefore, the Taxpayer's request for refund for tax year [year 1] was untimely filed outside the period prescribed by section 5278(1). The Taxpayer argues that the 10-year carry over provision of section 5217-D(2)(A) entitles him to the refund that he claimed and that the 3-year limitation period under section 5278(1) does not apply. However, he has provided no authority in support of this contention and we are aware of none. Carryover credits operate to allow a taxpayer to carry an unusable credit forward to future tax years where it may be applied. See e.g. id. 5217-D(2)(A). The Taxpayer's argument on this ground does not warrant an adjustment to the refund denial for [year 1]. The Taxpayer further argues that he was not aware that the EOTC credit existed until after the time limitation of section 5278(1) had passed because the availability of the credit was not adequately publicized. He maintains that, under these circumstances, applying the refund limitation against him would be unfair. Since 2013, Maine law has required advertisement and promotion of the EOTC by the Maine Department of Education, Maine Revenue Services, the Finance Authority of Maine, the Maine Department of Economic and Community Development, and the Maine Department of Labor, as well as by public institutions of higher education. 20-A M.R.S. $ 12542(4-A), (6-8). The Taxpayer has not shown that those agencies and entities failed to fulfil their statutory obligations in that regard. Even so, the Legislature has provided no exception to the section 5278(1) refund limitation that would apply to the circumstances complained of. The Maine Law Court has recognized that [s]tatutes of limitation are strictly construed. Dowling v. Salewski, 2007 ME 78 911,926 A.2d 193; see also Stromberg-Carlson Corp. v. State Tax Assessor, 2001 ME 11 913, 765 A.2d 566 (limitation on tax assessment); accord United States v. Clintwood Elkhorn Min. Co., 553 U.S. 1, 5 (2008) ("[U]nless a claim for refund of a tax has been filed within the time limits imposed by [the federal refund statute), a suit for refund ... may not be maintained in any court." (quoting United States v. Dalm, 494 U.S. 596, 602 (1990))); see also Stauffer v. IRS, 285 F. Supp. 3d 474, 480 (D. Mass. 2017) ([C]ourts may not [extend], for non- statutory equitable reasons, the statutory time ... limitations for filing tax refund claims set for in [the federal refund statute]. (internal quotation marks omitted) (quoting United States v. Brockamp, 519 U.S. 347, 348 (1997))). Accordingly, even if the EOTC credit was not advertised and promoted as required, we are unable to extend the time limitation set under section 5278(1). No adjustment to the refund denial for tax year [year l] is warranted. B. Tax year [year 4]: EOTC Qualification The Taxpayer's amended (year 4] return, filed April 11, [year 8], contained a timely filed claim of the EOTC credit for that tax year. The Taxpayer argues on appeal that MRS incorrectly disallowed his claim of the credit. To qualify for the EOTC, an individual must be a Maine resident for the tax year in question, must meet certain academic criteria, and must have worked at least part time in this State for an employer or as a self-employed individual.... 36 M.R.S. 8 5217-D(1)(G)(1), (4)- (5). The Taxpayer's Maine residency and academic qualifications are undisputed, and we find that he has met those requirements. We now consider the Taxpayer's employment qualifications for [year 4] under section 5217-D. The Taxpayer contends that he worked in Maine on a part-time basis for at least part of every month of the [year 4] tax year. Pursuant to section 5217-D(1)(D), part-time work is defined as work with a normal workweek of between 16 and 32 hours. Furthermore, an individual who worked in this State for any part of a month during the Maine residency period of the taxable year is considered to have worked in this State for the entire month.... Id. 5217- D(2)(B). The Taxpayer stated that he could not provide documentation to show that he met the Maine work requirement for EOTC eligibility in [year 4]. Rather, in the Response to Request for Additional Information that he submitted on appeal, he asserted that his routine Maine work week for that year consisted of working greater than 32 hours a week and most often working at least 35 hours to 50 hours a week, for all but 5 of the weeks...." He explained that, in [year 4], he did often work 5-7 days a week as a necessity to balance [his] customer's needs, with the Maine weather forecast, with scheduling availability. In addition, [his] routine Maine work schedule in [year 4] was daily 6:00AM until 5:00PM plus one additional work day at 7:30AM until 12 Noon. Id. Although it is possible that the Taxpayer met the Maine EOTC employment requirement in some months, the evidence submitted is insufficient to show that he met the employment requirement in any particular month during the tax year at issue. The Taxpayer has not shown that MRS erroneously denied his claim for the EOTC credit for tax year [year 4]. No adjustment to the refund denial for that year is warranted. III. Decision Based on the law and evidence presented, we uphold MRS's denial of refund for tax years [year 1) and (year 4] in full. The Board may, in limited circumstances, reconsider its decision on any appeal. If either party wishes to request reconsideration, that party must file a written request with the Board within 20 days of receiving this decision. Contact the Appeals Office at 207-287-2864 or see the Board's rules, available at http://www.maine.gov/boardoftaxappeals/lawsrules/, for more information on when the Board may grant reconsideration. If no request for reconsideration is filed within 20 days of the date of this proposed decision, it will become the Board's final administrative action. If either party wishes to appeal the Board's decision in this matter to the Maine Superior Court, that party must do so within 60 days of receiving this decision. Issued by the Board: July 24, 2020

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock