Question: Help in answering this 7. (5 points) You are constructing Table M for a particular risk with a retrospective rating plan. (a) (1 point) Express

Help in answering this

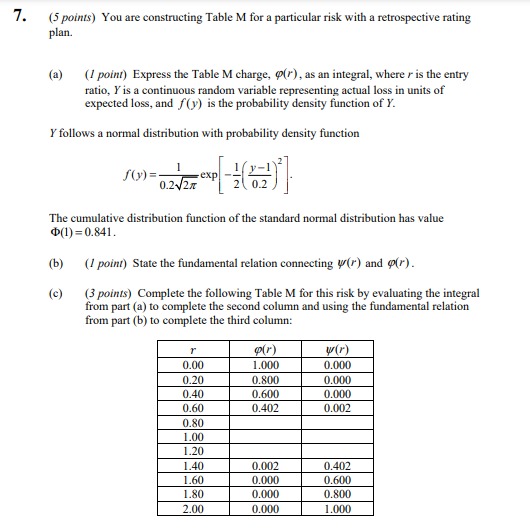

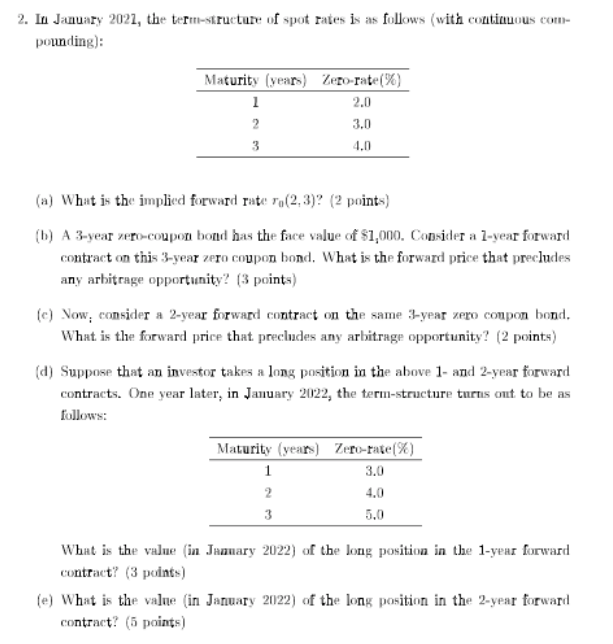

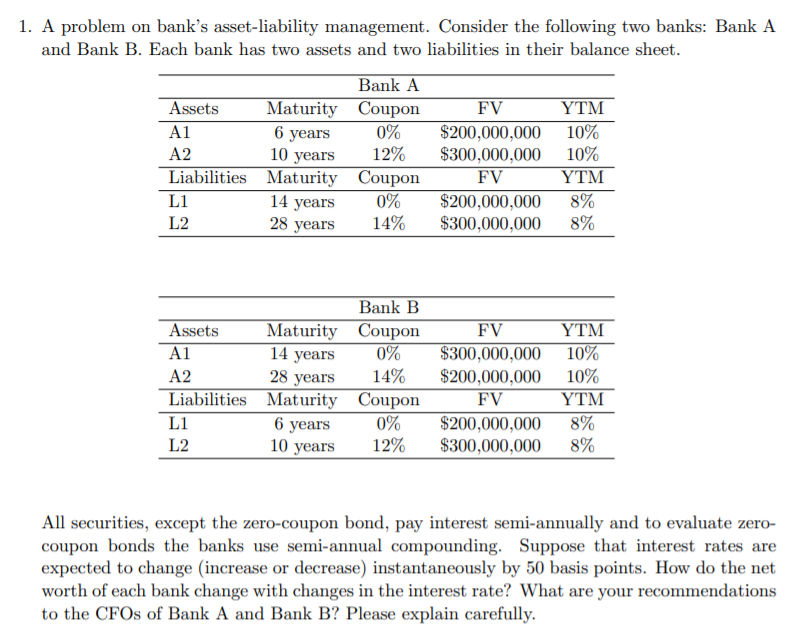

7. (5 points) You are constructing Table M for a particular risk with a retrospective rating plan. (a) (1 point) Express the Table M charge, p(), as an integral, where r is the entry ratio, Y is a continuous random variable representing actual loss in units of expected loss, and f()) is the probability density function of Y. Y' follows a normal distribution with probability density function f())= = - expl 0.2-/2x The cumulative distribution function of the standard normal distribution has value D(1) =0.841. (b) (/ point) State the fundamental relation connecting y(r) and (r). (c) (3 points) Complete the following Table M for this risk by evaluating the integral from part (a) to complete the second column and using the fundamental relation from part (b) to complete the third column: r 0.00 1.000 0.000 D.20 0.800 0.000 0.40 0.600 0.000 0.60 0.402 0.002 D.80 1.00 1.20 1.40 0.002 0.402 1.60 0.000 3.600 1.80 0.000 0.800 2.00 0.000 1.0002. In January 2021, the term-structure of spot rates is as follows (with continuous com- pounding): Maturity (years) Zero-rate (%) 2.0 3.0 4.0 (a) What is the implied forward rate ro(2,3)? (2 points) (b) A 3-year zero-coupon bond has the face value of $1,000. Consider a 1-year forward contract on this 3-year zero coupon bond. What is the forward price that precludes any arbitrage opportunity? (3 points) (c) Now; consider a 2-year forward contract on the same 3-year zero coupon bond. What is the forward price that precludes any arbitrage opportunity? (2 points) (d) Suppose that an investor takes a long position in the above 1- and 2-year forward contracts. One year later, in January 2022, the term-structure turns out to be as follows: Maturity (years) Zero-rate (%) 3.0 4.0 5.0 What is the value (in January 2022) of the long position in the 1-year forward contract? (3 points) (e) What is the value (in January 2022) of the long position in the 2-year forward contract? (5 points)1. A problem on bank's asset-liability management. Consider the following two banks: Bank A and Bank B. Each bank has two assets and two liabilities in their balance sheet. Bank A Assets Maturity Coupon FV YTM A1 6 years 0% $200,000,000 10% A2 10 years 12% $300,000,000 10% Liabilities Maturity Coupon FV YTM L1 14 years 0% $200,000,000 8% L2 23 years 14% $300,000,000 8% Bank B Assets Maturity Coupon FV YTM A1 14 years We $300,000,000 10% A2 28 years 14% $200,000,000 10% Liabilities Maturity Coupon FV YTM L1 6 years 0% $200,000,000 8% L2 10 years 12% $300,000,000 8% All securities, except the zero-coupon bond, pay,r interest semi-annually and to evaluate zero- coupon bonds the banks use semi-armual compounding. Suppose that interest rates are expected to change (increase or decrease) instantaneously by 50 basis points. How do the net worth of each bank change with changes in the interest rate? What are your recommendations to the CFOs of Bank A and Bank B? Please explain carefully