Question: Help me answer question 5 below: Problem 5. Suppose that on February 23, 1998, Wall Street Journal listed the following prices for European call options

Help me answer question 5 below:

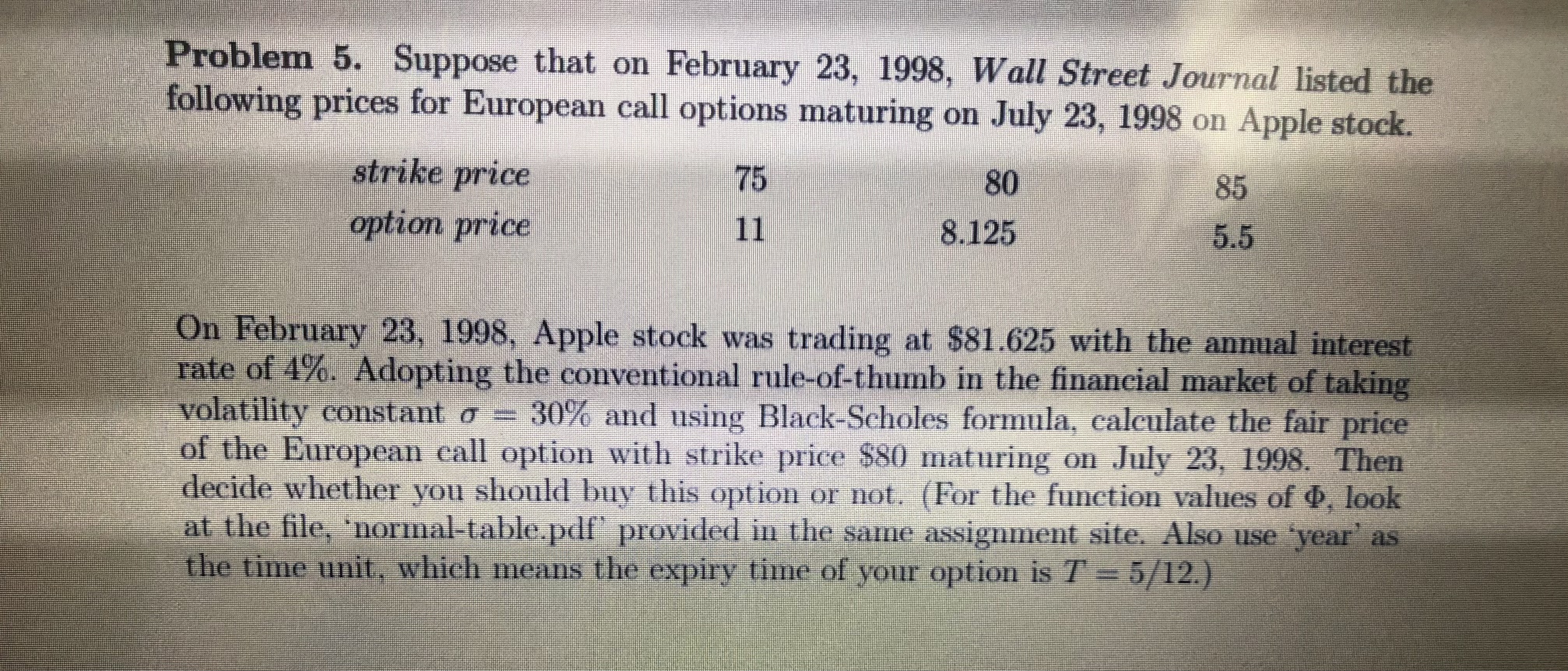

Problem 5. Suppose that on February 23, 1998, Wall Street Journal listed the following prices for European call options maturing on July 23, 1998 on Apple stock. strike price 75 80 85 option price 11 8.125 5.5 On February 23, 1998, Apple stock was trading at $81.625 with the annual interest rate of 4%. Adopting the conventional rule-of-thumb in the financial market of taking volatility constant o - 30% and using Black-Scholes formula, calculate the fair price of the European call option with strike price $80 maturing on July 23, 1998. Then decide whether you should buy this option or not. (For the function values of &, look at the file, 'normal-table.pdf provided in the same assignment site. Also use 'year' as the time unit, which means the expiry time of your option is 7 - 5/12.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts