Question: help me explain why please 5. Using annual data on stocks returns for Nike and Adidas, you estimate the following two single-factor regressions Nike, t

help me explain why please

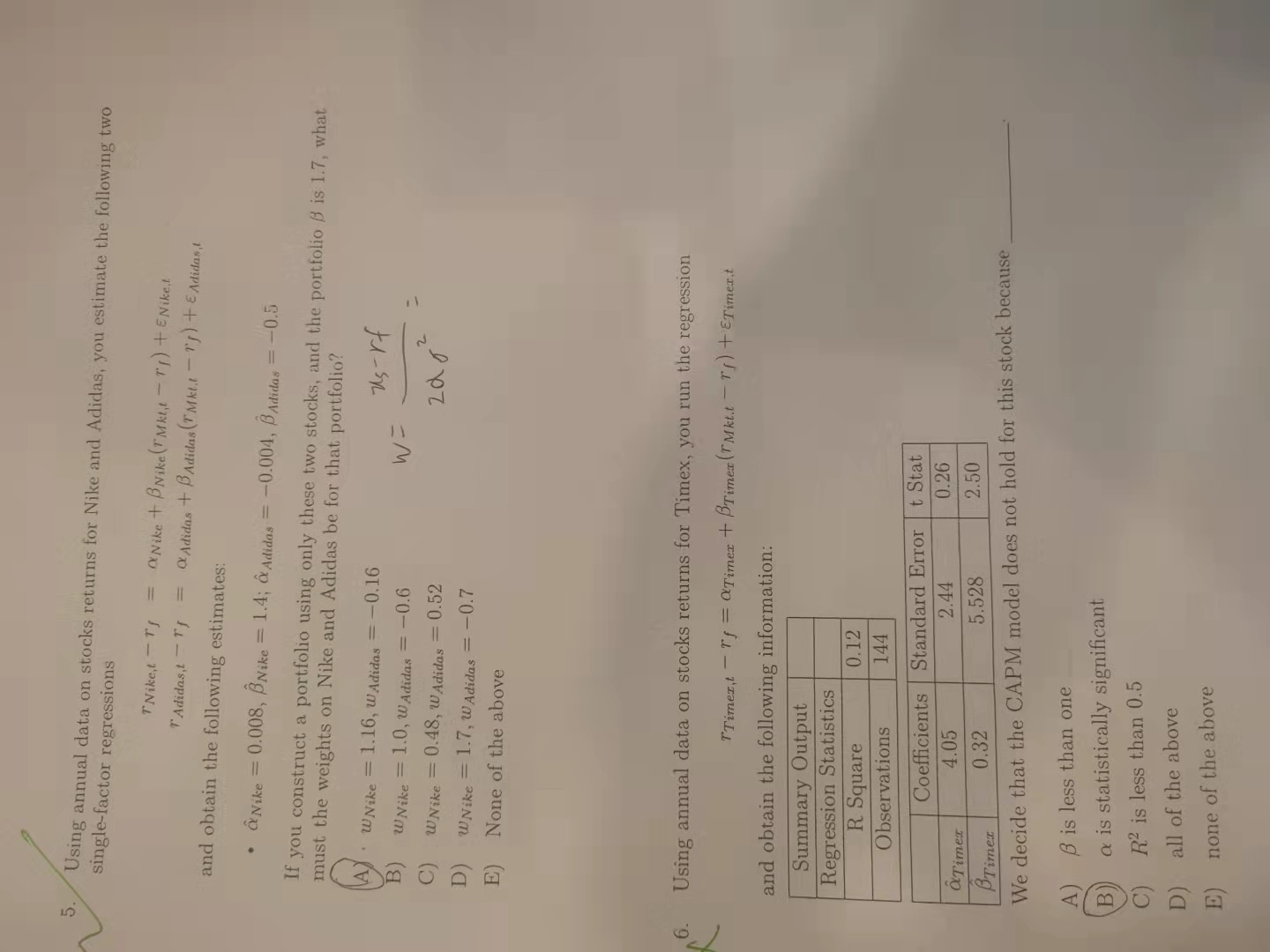

5. Using annual data on stocks returns for Nike and Adidas, you estimate the following two single-factor regressions Nike, t - OxNike + B Nike(TMkt, -ri) + ENiket Adidas, tas Adidas + BAdidas (TMkl-ri) + E Adidas, 1 and obtain the following estimates: & Nike = 0.008, BNike = 1.4; & Adidas = -0.004, B Adidas = -0.5 If you construct a portfolio using only these two stocks, and the portfolio B is 1.7, what must the weights on Nike and Adidas be for that portfolio? KA WNike = 1.16, W Adidas = -0.16 Us-rf B) W Nike = 1.0, W Adidas = -0.6 W= C) W Nike = 0.48, W Adidas = 0.52 zdo D) W Nike = 1.7, W Adidas = -0.7 E) None of the above 2 6. Using annual data on stocks returns for Timex, you run the regression Timez,t-ry=dTimex + BTimex (Tmkt.t-Tn) + Etiment and obtain the following information: Summary Output Regression Statistics R Square 0.12 Observations 144 t Stat Coefficients Standard Error 4.05 2.44 0.32 5.528 ATimes 0.26 2.50 BTimes We decide that the CAPM model does not hold for this stock because A B B is less than one a is statistically significant R2 is less than 0.5 all of the above C D) E) e none of the above

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts