Question: Help me to solve this task please:) Problem A company has a liability of $100, 000 in two years time. The two year rate is

Help me to solve this task please:)

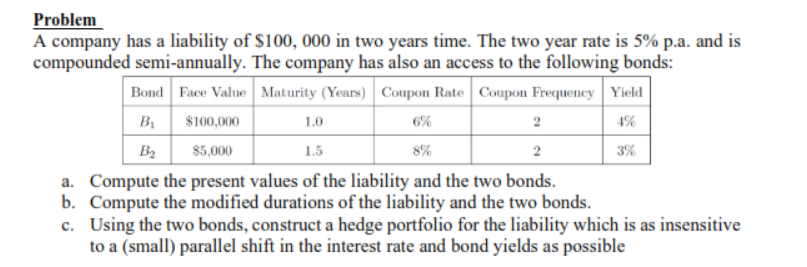

Problem A company has a liability of $100, 000 in two years time. The two year rate is 5% pa. and is compounded semi-annually. The company has also an access to the following bonds: Bond Face Value Maturity (Years) Coupon Rate Coupon Frequency Yield BI $100,000 1.0 6% 2 4% B2 $5.000 1.5 8% 2 3% a. Compute the present values of the liability and the two bonds. b. Compute the modified durations of the liability and the two bonds. c. Using the two bonds, construct a hedge portfolio for the liability which is as insensitive to a (small) parallel shift in the interest rate and bond yields as possible

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts