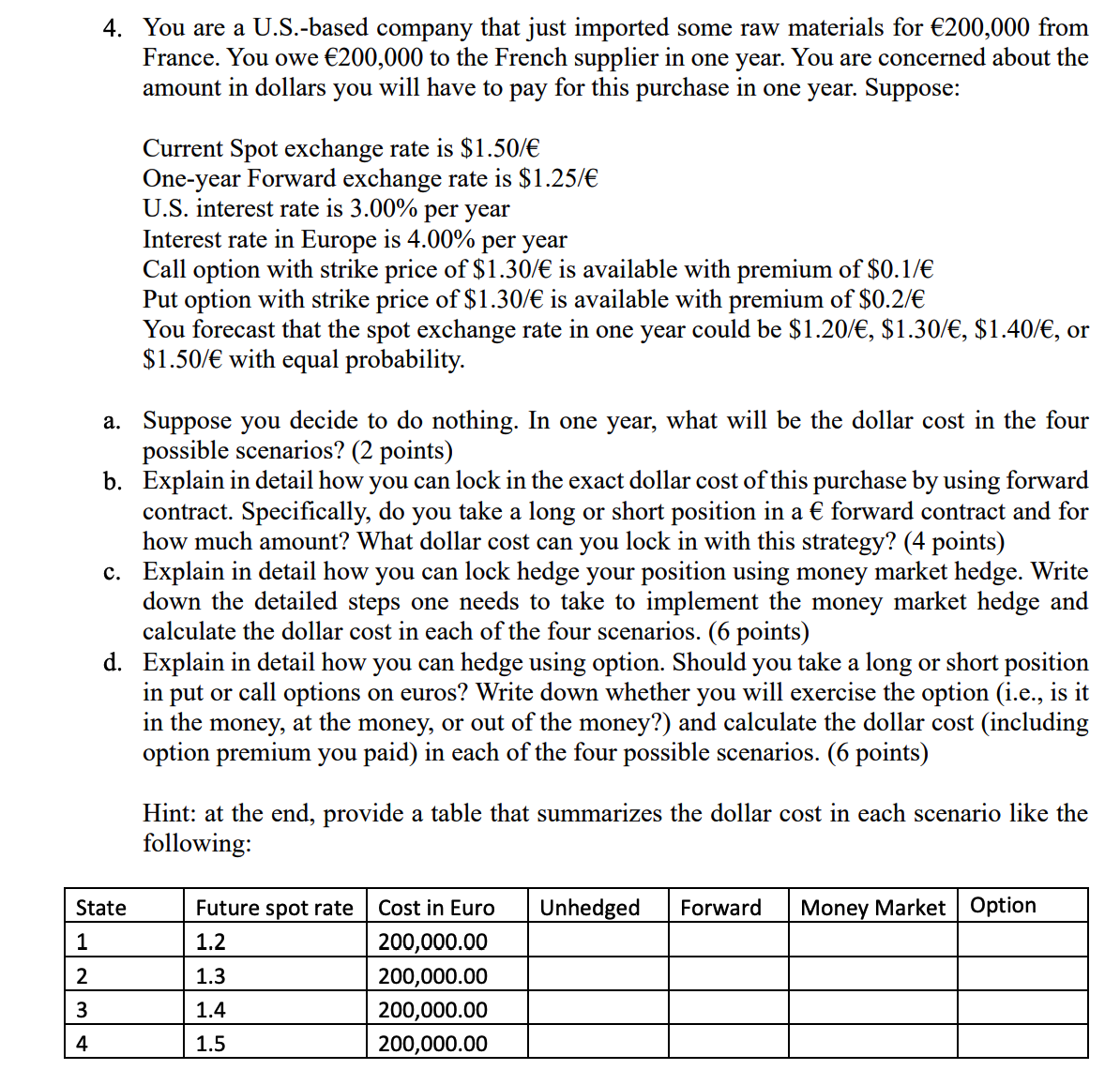

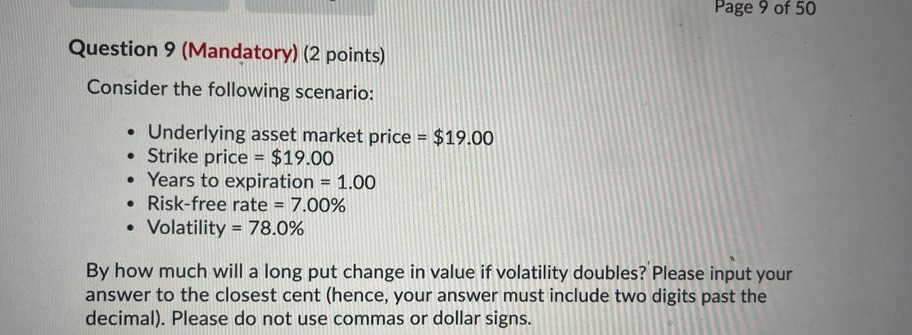

Question: Help me understand. . You are a U.S.-based company that just imported some raw materials for 200,000 from France. You owe 200,000 to the French

Help me understand.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock