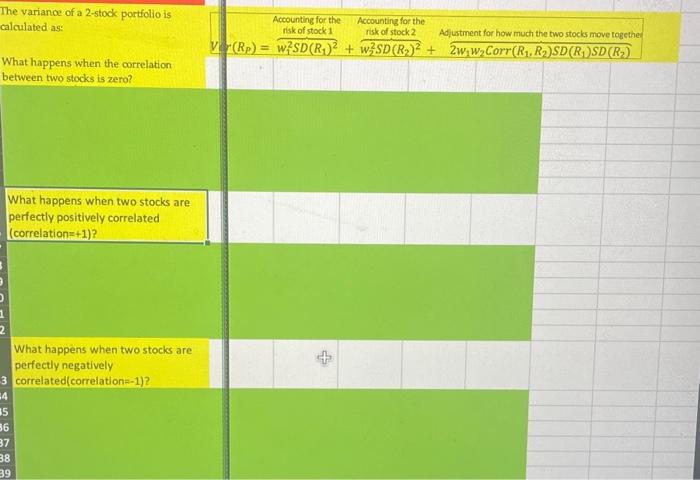

Question: help ! move togethe SD(R2) variance Cf a portfolio is What happens When the between VO What happens when two stocks are perfectly positively correlated

help !

move togethe SD(R2)

variance Cf a portfolio is What happens When the between VO What happens when two stocks are perfectly positively correlated (correlation: What happens when two stocks are perfectly negatively t he risk 2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock