Question: help This question compares performance statistics of weekly returns series against a 52 weeks moving average returns series. Which of the following statements is incorrect?

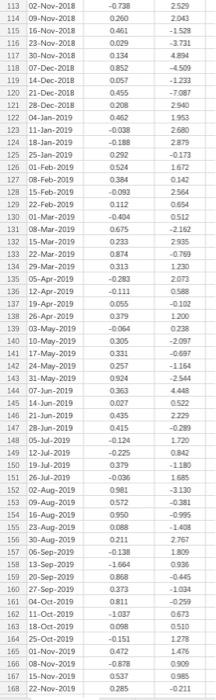

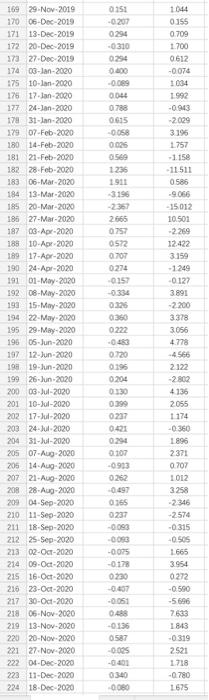

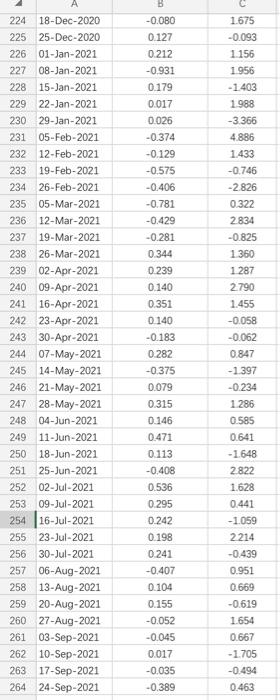

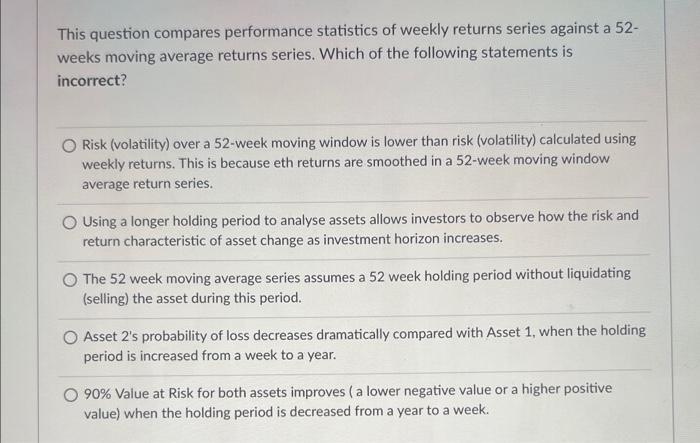

This question compares performance statistics of weekly returns series against a 52 weeks moving average returns series. Which of the following statements is incorrect? Risk (volatility) over a 52-week moving window is lower than risk (volatility) calculated using weekly returns. This is because eth returns are smoothed in a 52 -week moving window average return series. Using a longer holding period to analyse assets allows investors to observe how the risk and return characteristic of asset change as investment horizon increases. The 52 week moving average series assumes a 52 week holding period without liquidating (selling) the asset during this period. Asset 2's probability of loss decreases dramatically compared with Asset 1 , when the holding period is increased from a week to a year. 90% Value at Risk for both assets improves ( a lower negative value or a higher positive value) when the holding period is decreased from a year to a week

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts