Question: Help with #2 and #3 please thanks! Calculate M^2 for BA and (Portfolio + BA), use SPY as a proxy for the Market Portfolio. a.

Help with #2 and #3 please thanks!

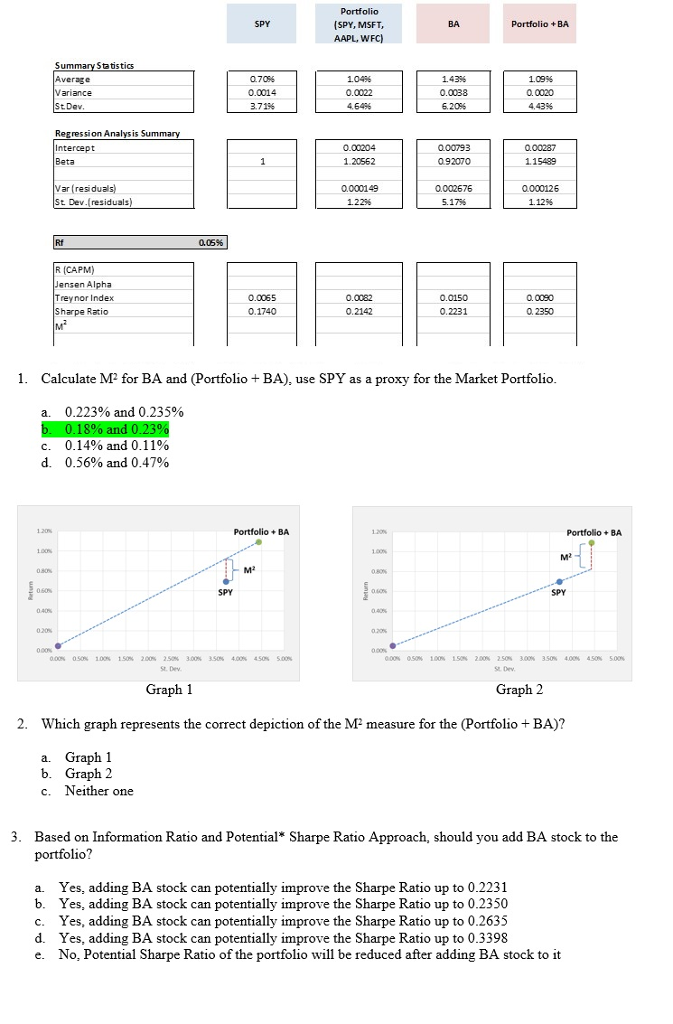

Calculate M^2 for BA and (Portfolio + BA), use SPY as a proxy for the Market Portfolio. a. 0.223% and 0.235% b. 0.18% and 0.23% c. 0.14% and 0.11% d. 0.56% and 0.47% Which graph represents the correct depiction of the M^2 measure for the (Portfolio + BA)? a. Graph 1 b. Graph 2 c. Neither one Based on Information Ratio and Potential* Sharpe Ratio Approach, should you add BA stock to the portfolio? a. Yes, adding BA stock can potentially improve the Sharpe Ratio up to 0.2231 b. Yes, adding BA stock can potentially improve the Sharpe Ratio up to 0.2350 c. Yes, adding BA stock can potentially improve the Sharpe Ratio up to 0.2635 d. Yes, adding BA stock can potentially improve the Sharpe Ratio up to 0.3398 e. No, Potential Sharpe Ratio of the portfolio will be reduced after adding BA stock to it

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts