Question: help with #7 acaulay's Duration: Modified Duration: Macaulay's Duration Modified Duration =- 1+ y Projected % Change in Bond Price Example 7: Calculate the expected

help with #7

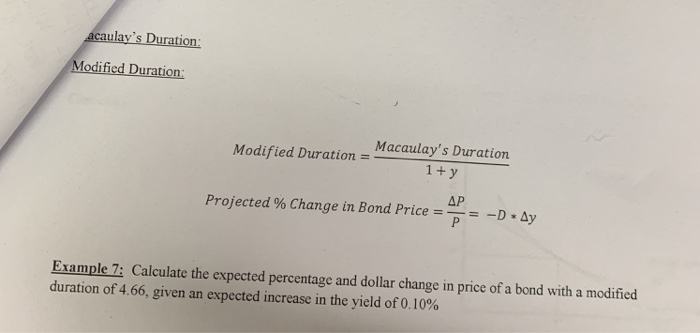

acaulay's Duration: Modified Duration: Macaulay's Duration Modified Duration =- 1+ y Projected % Change in Bond Price Example 7: Calculate the expected percentage and dollar change in price of a bond with a modified duration of 4.66, given an expected increase in the yield of 0.10%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock