Question: Help with taxation 2B Question 1 (20 Marks) You are the financial manager of Emperors (Phy) Lid, a property company earning is income from both

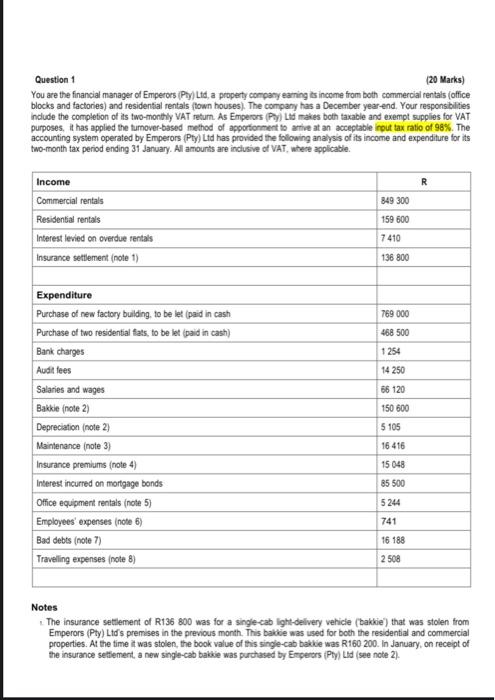

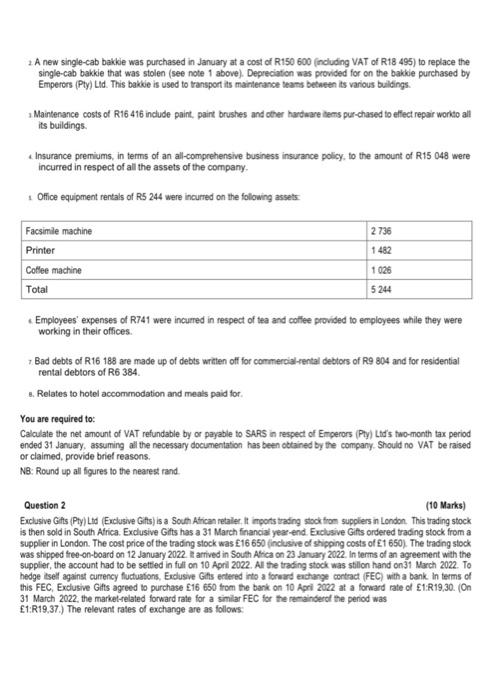

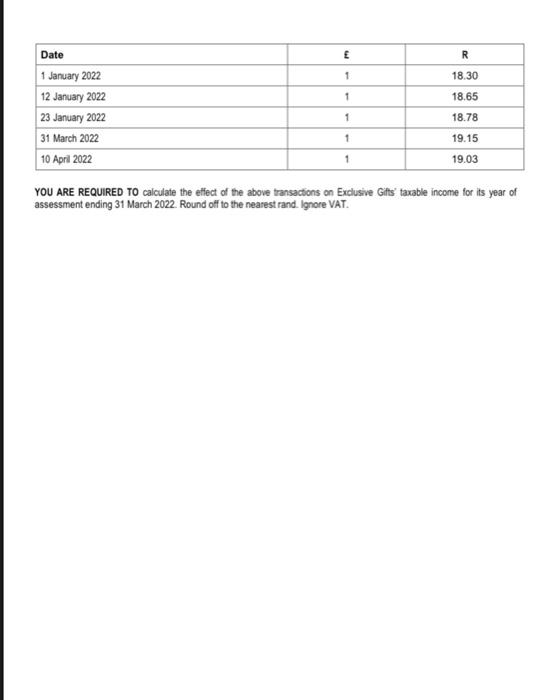

Question 1 (20 Marks) You are the financial manager of Emperors (Phy) Lid, a property company earning is income from both commercial rentals (office blocks and factories) and residential rentals (town houses). The company has a December year end. Your responsibilities indude the completion of its two-monthy VAT retum. As Emperors (Pay) Lif makes both taxable and exempt supplies for VAT purposes, th has applied the turnover-based method of apportonment to artive at an acceptable irout tax ratio of 98%. The accounting system operated by Emperors (Pty) Ltd has provided the following analysis of its income and expenditure for its two-month tax period ending 31 January. All amounts are inclusive of VAT, where applicable. Notes 1. The insurance setternent of R136 800 was for a single-cab light-delvery vehicle (bakkie') that was stolen from Emperors (Pty) Ltd's premises in the previous month. This bakie was used for both the residential and commercial properties. At the time it was stolen, the book value of this single-cab bakbe was R160 200. In January, on receipt of the insurance settement, a new single-cab bakie was purchased by Erceers (Pty) LAd (see note 2). 2. A new single-cab bakkie was purchased in January at a cost of R150 600 (including VAT of R18 495) to replace the single-cab bakkie that was stolen (see note 1 above). Depreciation was provided for on the bakkie purchased by Emperors (Pty) Lid. This bakie is used to transport its mainterance teams between its various buldings. Maintenance costs of R16 416 include paint, paint brushes and other hardware tems pur-chased to effect repair workto all its buildings. 4. Insurance premiums, in terms of an all-comprehensive business insurance policy, to the amount of R15 048 were incurred in respect of all the assets of the company. 1. Office equipment rentals of R5 244 were incurred on the following assets: . Employees' expenses of R741 were incurred in respect of tea and collee provided to employees while they were working in their offices. 7. Bad debts of R16 188 are made up of debts wrtten off for commercial-rental debtors of R9 804 and for residential rental debtors of R6 384 . 8. Relates to hotel accommodation and meals paid for. You are required to: Calculate the net amount of VAT refundable by or payable to SARS in respect of Emcerors (Pty) Ltif's two-month tax period ended 31 January, assuming all the necessary documentation has been obtained by the company. Should no VAT be raised or claimed, provide brief reasons. N8: Round up all figures to the nearest rand. Question 2 (10 Marks) Exclusive Gifts (Pty) Lid (Exclusive Gifts) is a Soum. Atrican retaler, it imports trading stock from supplers in London. This trading stock is then sold in South Africa. Exclusive Gifts has a 31 March financial year-end. Exclusive Gifts ordered trading stock from a supplier in London. The cost price of the trading stock was E16 650 (inclusive of shipping costs of E1 650). The trading stock was shipped tree-on-board on 12 January 2022 . I artived in South Alica on 23 January 2022 . In terms of an agreement with the supplier, the account had to be settled in full on 10 April 2022. All the trading stock was stilion hand on31 March 2022. To hedge tsell against currency fluctuations, Eidusive Gits entered into a forward exchange contract (FEC) with a bank in terms of this FEC, Exclusive Gitts agreed to purchase E16 650 trom the bank on 10 Apri 2022 at a forward rate of E1:R19,30. (On 31 March 2022, the market-related forward rate for a similar FEC for the remainderct the period was E1:R19,37.) The relevant rates of exchange are as follows: YOU ARE REQUIRED TO calculate the effect of the above transactions on Exclusive Gifts' taxable income for its year of assessment ending 31 March 2022. Round off to the nearest rand. lgnore VAT

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts