Question: Here are the questions (with guidelines): Question 1 Why do Molex have to hire an external auditor? ? It is required by the SEC according

Here are the questions (with guidelines):

Question 1 Why do Molex have to hire an external auditor? ? It is required by the SEC according to the security laws. ? Why the security laws make such requirement? ? Information asymmetry between investors and company management ? Using of the financial statements as a means by the company to communicate with investors ? Credibility of financial statements is certified by external auditors ? Auditors therefore play a key role in assuring investors that the financial information produced by management is reliable. Without their assurance, investors would not be able to rely on the firm's financial reports Question 2 What was the financial reporting problem at Molex? How would thecorrection of the problem be recorded in Molex's financial statements? (IMPORTANT: Please show a table of the updated financial statements of the changes made!) ? The company had not eliminated profits from inter-company sales between its subsidiaries which had not been sold to an external customer by year-end. For example, assuming that Subsidiary A sold merchandise that cost $40 million to Subsidiary B during the year for $48 million. This inventory had not been sold by Subsidiary B at the end of the reporting year. The following record keeping would be used to account for the sale and purchase in the books of each subsidiary (without any adjustment). Therefore, consolidated inventory was overstated by $8 million. Group earnings are overstated by $5.8 million, the after-tax effect of the intra-company sale. ? To make the adjustment, Inventory decrease by $8 million, Tax Expense decrease by $2.2 million, and Net Income decrease by $5.8 million. Question 3 What factors do you think influenced management's decision not toraise the issue with the auditors? ? Is $8 million overstatement in Inventory and $5.8 million overstatement in Net Income material? ? What amount is considered as material in the agreement between the company and Deloitte for purposes of the management representation letter? ? What's the percentage impact of the problem on sales, net income, and earning per share (EPS)? ? Whose opinion is more important, auditors' or management's? ? Would investors think it is material? ? Would the reporting EPS beats or falls below the investors' consensus, if the adjustment was made? ? Would investor still trust the company if they find out the management withheld such information from disclosure? ? What would short sellers on the market do if they are aware of the problem? Question 4 Why were the auditors so concerned about the reporting problem atMolex? If you were a member of the board, do you agree with their concerns? ? What the auditor hoped to achieve by requesting a new CFO/CEO? ? What are the risks for the auditor in this case? ? The role of CFO in this case ? The role of CEO in this case? Who is the one to be trusted? CEO? CFO, or Both? Question 5 As a member of Molex's board, what would you do to respond to theauditor's request that the CFO (and possibly the CEO) be replaced? No matter what your opinion on the culpability of Bullock and King in the accounting problem, the board has to make a tough decision. ? If it refuses to fire Bullock, the auditors will probably quit. What impact will this event have on the firm? ? What requirements will another large audit firm place on Molex's board before signing on to become the auditor?

Here is the case/ relevant information:

Page 1

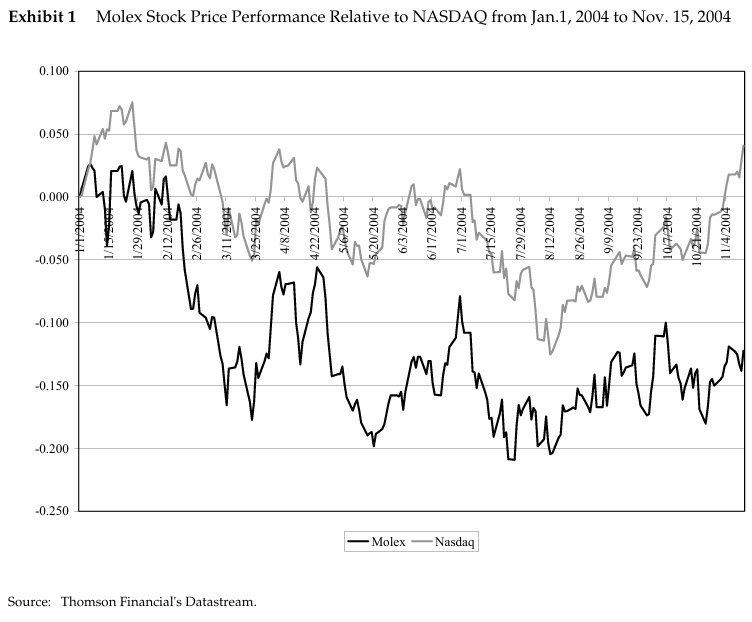

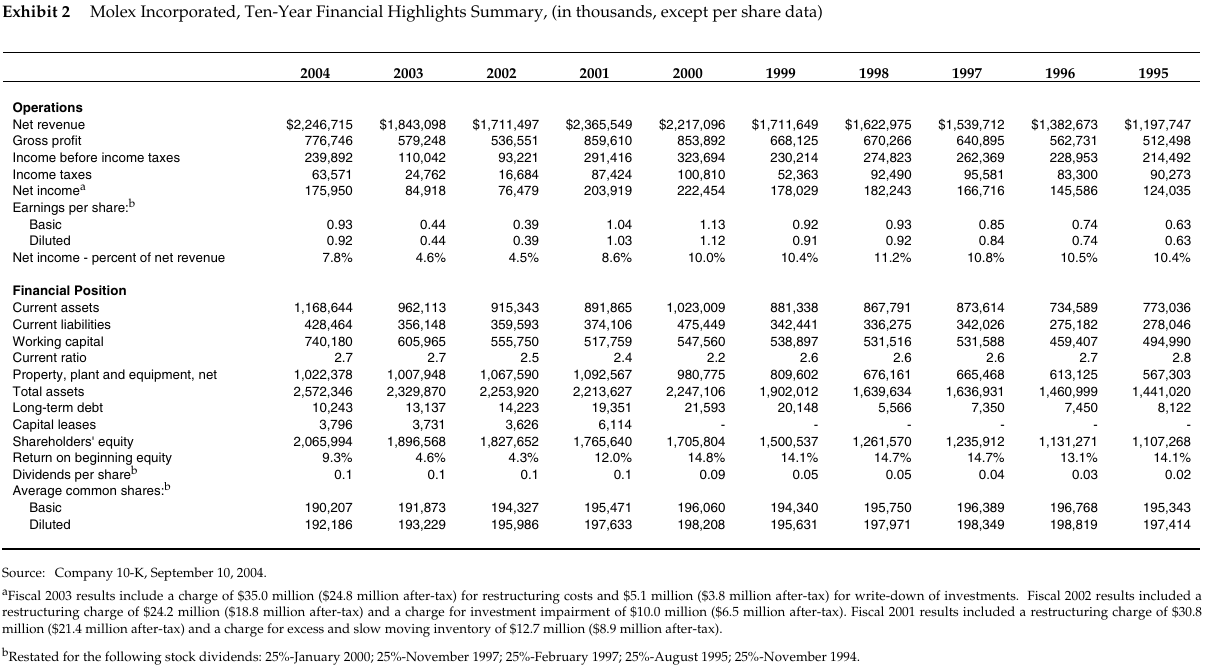

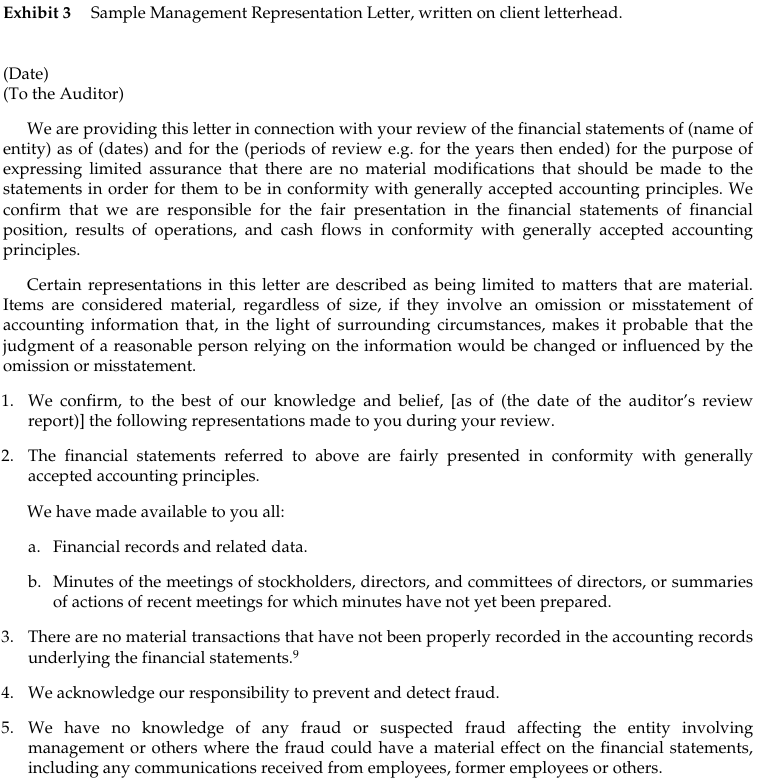

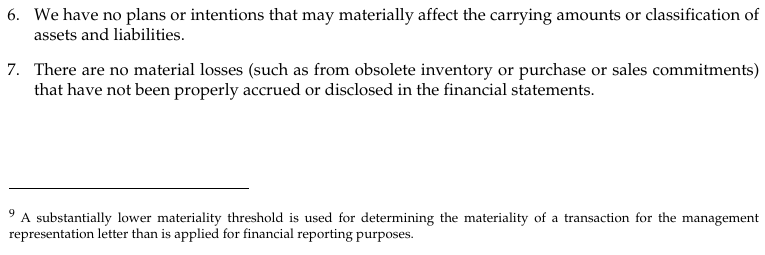

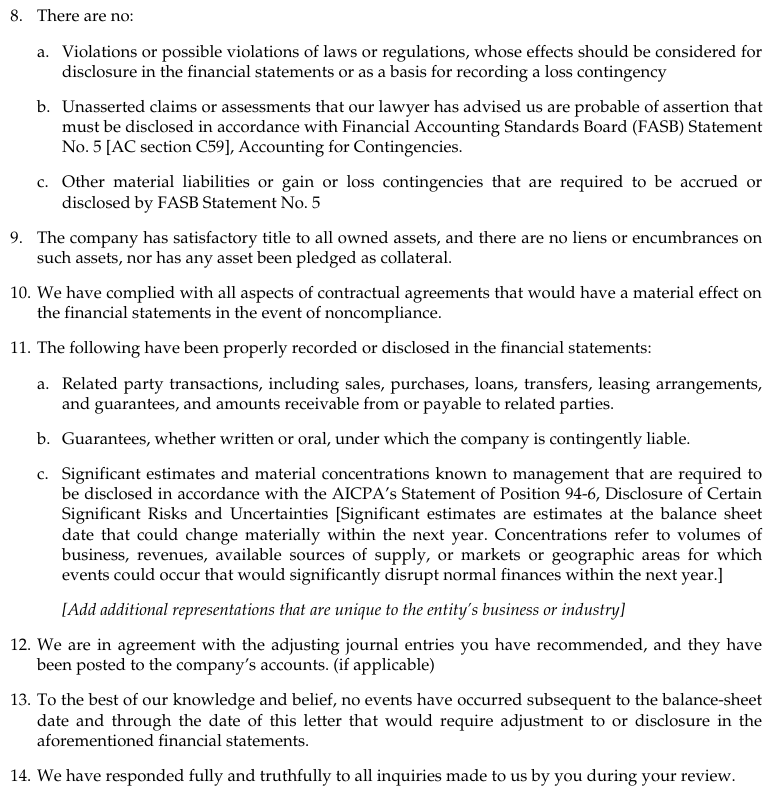

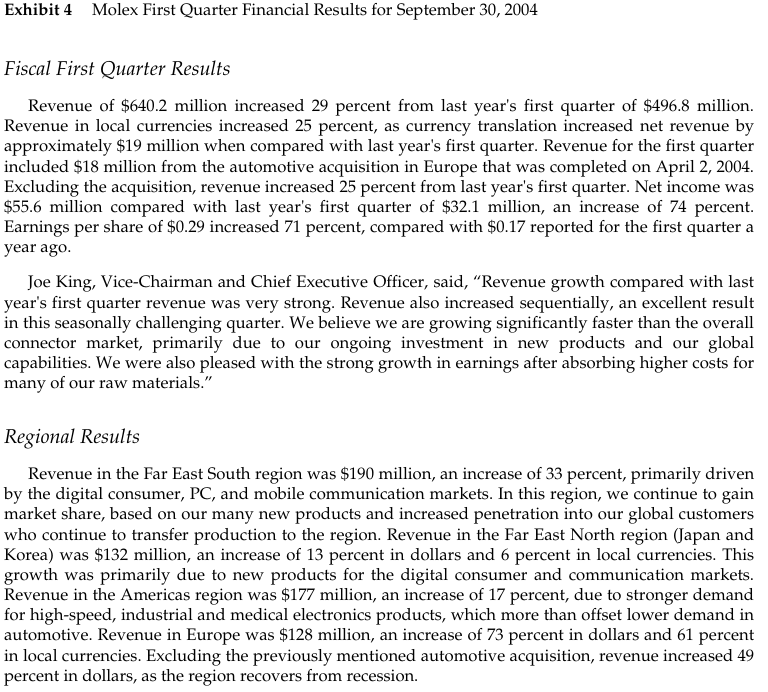

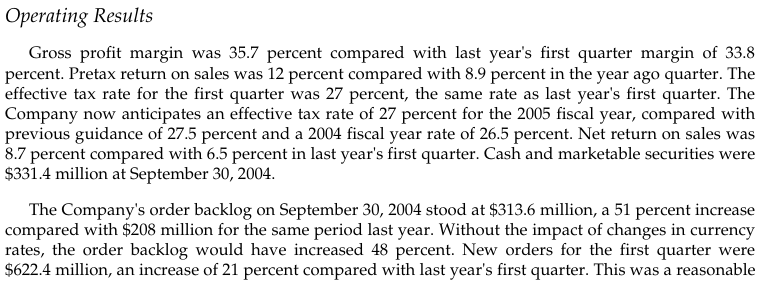

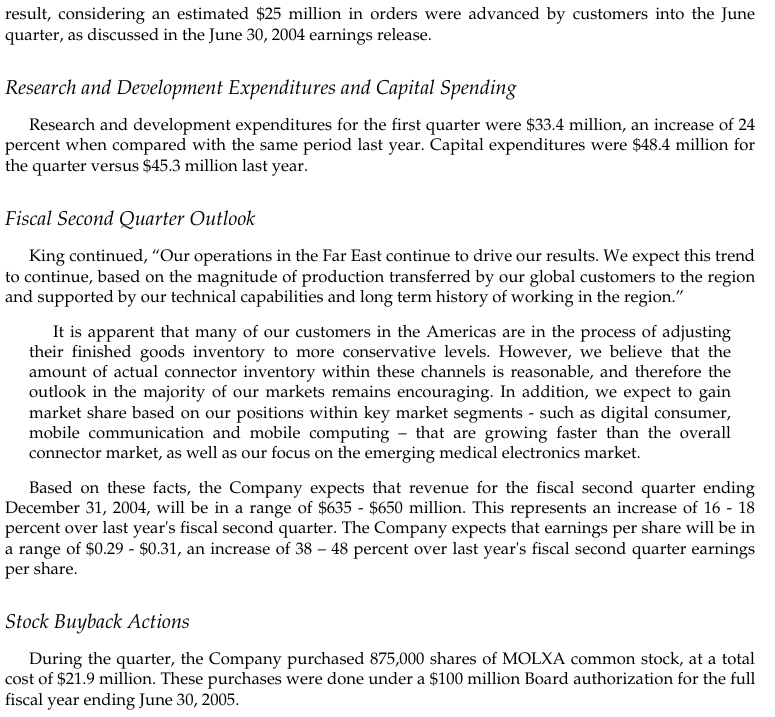

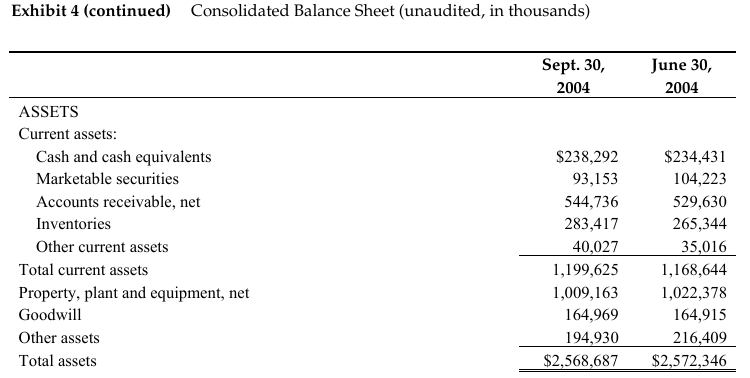

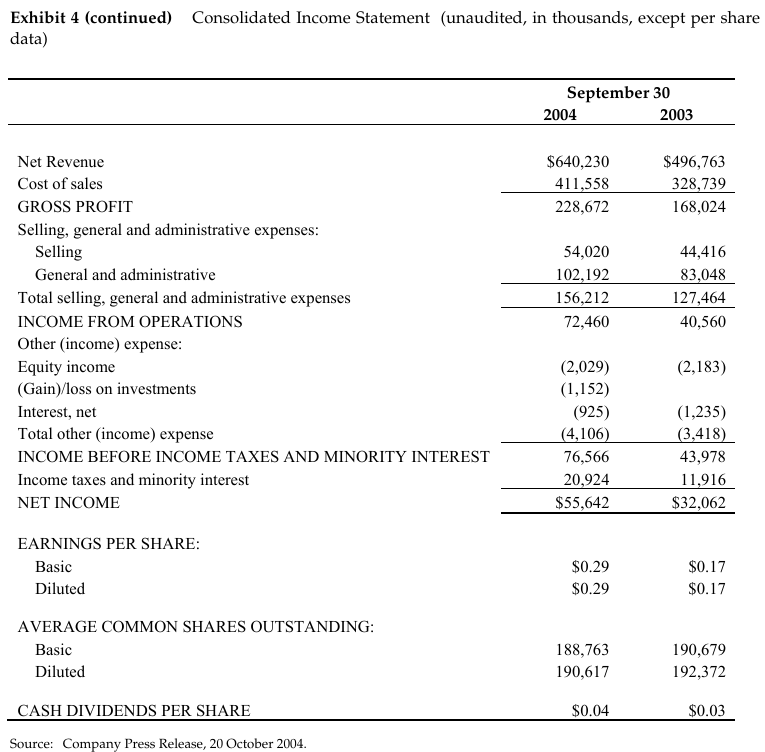

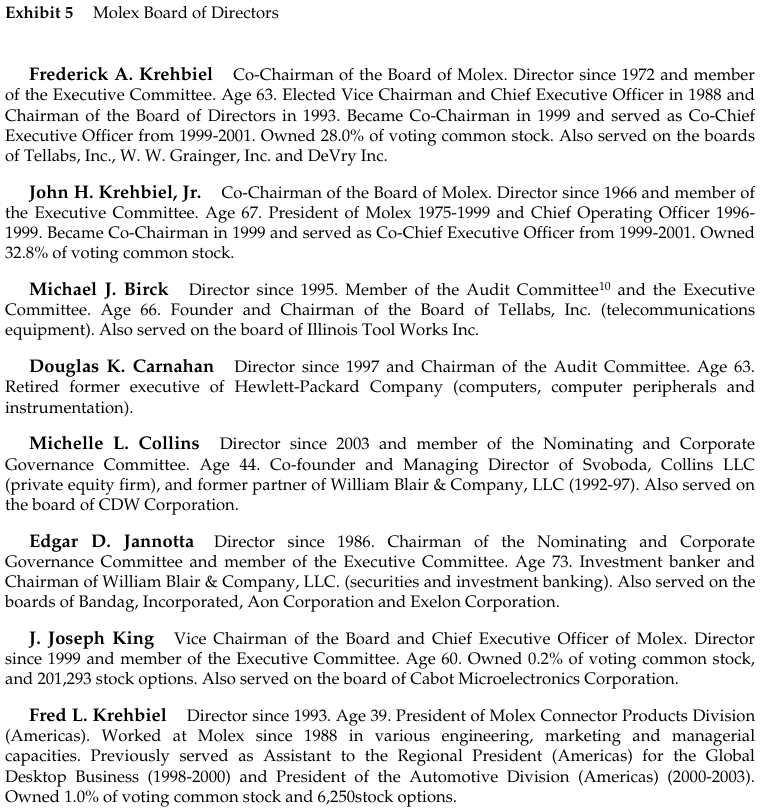

Financial Reporting Problems at Molex, Inc. (A) In mid-November 2004, Molex's Board of Directors met to decide the future of Joe King and Diane Bullock, the company's CEO and CFO respectively. Molex's external auditors, Deloitte & Touche, had accused both of failing to disclose an $8 million pre-tax inventory valuation error in a recent letter of representation to the auditors. In response, King and Bullock argued that at the time of their letter they had determined that the financial impact of the error was immaterial. Despite an inquiry by the Audit Committee, which concluded that management had not deliberately withheld information from the auditors, Deloitte & Touche was not satisfied. The audit firm insisted that it could no longer rely on Bullock's and King's representations, and would be unable to complete its review of the first quarter results until representations were received from a new CFO and in all likelihood a new CEO. Molex Background and Management Founded in Lisle, Illinois in 1938 by Frederick Krehbiel, Molex Inc. designed, manufactured and distributed electronic connectors that were used by a wide range of industries.! For example, in the computer industry its connectors were used to produce computers, servers and printers; in the telecommunications industry they were used to produce mobile phones and networking equipment; the consumer products industry used Molex connectors to manufacture CD and DVD players, cameras, plasma and LCD televisions; and the automotive industry used them for the production of engine control units and adaptive breaking systems. In 2003, Molex was the second largest firm in the connector industry, with a worldwide share of 6.9%, and production and distribution facilities located throughout the world.? In July 2001, Molex's board of directors appointed Joe King as vice chairman and chief executive officer. Trained as an engineer in Ireland, King had joined Molex as a quality control manager in 1975. Initially responsible for overseeing manufacturing quality at the company's Shannon plant and for working with customers on technical issues, he soon took over material management, including planning, purchasing and inventory control. King was subsequently promoted to assistant head of ! The Krehbiel family continued to have a controlling interest in Molex. Brothers Frederick A. Krehbiel and John H. Krehbiel, Jr. were Co-Chairs of the Board of Directors and former CEOs, and Fred L. Krehbiel, the son of John H. Krehbiel, Jr. was a member of the board. 2 The number one firm in the industry was Tyco Electronics, with a 19.7% market share. See \"Top 100 Connector Manufacturers,\" Market Research Report, Bishop & Associates, September 2004, international operations, which covered the U.S. Export Group and Computer Systems, and then to vice president of operations, where he oversaw most of the company's technical systems and was in charge of developing and implementing a strategic plan for international operations. From 1985 to 1988, as corporate vice president and president of the Far East south region, he opened an operating facility in Malaysia, initiated discussions on operations that would later open in Thailand and China, and developed the region's marketing and engineering capabilities. As competition in the region intensified during the late 1980s, King stressed customer service, quality, and new product development as ways for Molex to compete more effectively. In 1988, he was appointed group vice president-international, responsible for sales and manufacturing operations in Europe, the Far East and new international ventures. Eight years later, King became executive vice president for functional groups worldwide, where he played a key role in integrating domestic and international operations, consolidating global staff functions, and assigning all regions to report to one person, the president and chief operating officer.? In contrast, Molex's chief financial officer, Diane Bullock, had a very brief history with the firm. She had been hired in October of 2003 to replace Bob Mahoney as CFO effective January 1, 2004. Bullock had previously held a variety of global financial positions in the automotive components industry and in public accounting, Molex Financial Performance 2002 and 2003 were challenging years for Molex. The company experienced a sharp downturn in demand for its products, particularly from technology customers. Molex management reacted by reducing its workforce and expenses, and by directing investment into products less affected by recession. Management's task was further complicated by heavy short selling of Molex's stock during the downturn. For example, during 2003, average short-interest was 8 million shares, roughly 12.5 days of average daily share volume.* The first sign of a recovery came during the quarter ended December 31, 2003 (the second quarter of the June 30, 2004 fiscal year), when sales and earnings increased by 21% and 46% respectively over the same quarter one year earlier. In response, Molex's stock price jumped by 6% relative to the Nasdaq Composite Index. However, the stock price increase proved to be temporary. On February 17, an online research firm, CashFlowNews.com, observed that Molex's free cash flow (defined as cash flow from operations minus capital expenditures) had declined 52% for the twelve months ended December 31, 2003, from $240 million to a six-year low of $114 million. Following publication of the report, Molex's stock fell by 8% relative to the Nasdaq Composite Index (see Exhibit 1 for a graph of Molex's stock price performance). Molex showed steady financial improvement during the first six months of 2004. Revenues for the vear ended June 30, 2004 increased by almost 22%, and net income more than doubled from $84.9 million to $176.0 million (see Exhibit 2 for a ten year summary of Molex's financial performance). The company reported fourth quarter earnings per share of $0.30, exceeding its own prior estimates of $0.27 to $0.29, and analyst estimates of $0.285 In a July 27, 2004 press release and in the 2004 10-K filed on September 10, 2004, management estimated that earnings per share for the first quarter of the following year would be between $0.26 and $0.29, compared to analyst forecasts of $0.29. In discussing the company's future prospects, management noted that: The outlook in the majority of the Company's global markets remains strong. ... The Company expects revenue growth of 16 percent to 19 percent during fiscal 2005 and net income is expected to grow faster than revenues due to leverage from the higher volume. Earnings per share are expected in the range of $1.24 to $1.34, an increase of 35 to 45 percent. Yet despite increased sales and earnings for 2004, and management's expectation of continued sales and earnings growth, Molex's stock price lagged the market and short interest in its stock remained high (8 million shares in August 2004). Audit Industry Challenges 2002 and 2003 were also challenging years for the audit industry. Its reputation for independence and high quality audits plunged following a wave of corporate accounting scandals that included Enron, Worldcom, Adelphia, Global Crossing and Freddie Mac in the US, and Ahold and Parmalat in Europe. In mid-2002, Enron's auditor, Arthur Andersen, the fifth largest auditing firm, was convicted of obstruction of justice for shredding documents related to its Enron audit. Since U.S. Securities and Exchange Commission (SEC) rules prohibited convicted felons from auditing public companies, Arthur Andersen was forced to surrender its licenses and its right to practice before the SEC, leaving only four large accounting firms (in order of size, Deloitte & Touche, PriceWaterhouseCooper, Ernst & Young, and KPMG). Although Arthur Andersen was the audit firm most closely identified with the accounting scandals, many of the other leading firms were also affected. For example, several of Deloitte & Touche's largest clients (notably Adelphia, Fortress Re, Parmalat, and Ahold) were hit with fraud and accounting problems, leading the accounting firm to face a string of law suits claiming billions of dollars in potential damages. Following the scandals and the collapse of Arthur Andersen, new regulations were adopted to improve the independence and quality of audits. For example, the Sarbannes Oxley Act of 2003 created a new oversight board (the Public Company Accounting Oversight Board) that was assigned responsibility for reviewing and disciplining accounting firms" audit quality, ethical standards, and independence. In addition, the act required audit partners to be rotated every five years. Audit firms, which had developed large consulting practices during the 1980s and 1990s, were prohibited from selling many of these services (including information systems design and implementation; appraisals, valuation, and actuarial services; and internal audit services) to their audit clients. Finally, audit committees, rather than management, were assigned responsibility for appointing and overseeing the external auditor, and for pre-approving the purchase of any material non-banned consulting services. Molex's Accounting Problem In mid-July 2004, Molex's corporate finance group identified a potential problem with inventory that had affected results for several years. Profits on inventory sales between Molex subsidiaries (but which had not been sold to an external customer by period-end) had not been excluded in computing the consolidated firm's earnings and inventory. Consequently, earnings, inventory and retained earnings were most likely overstated. After the discovery, disclosure of the misstatements to top management, the auditors, the audit committee, and investors took place as follows: July 21, 2004: Diane Bullock (the company's CFO) brought the matter to the attention of other top management at a meeting that included Joe King (the Vice-Chairman of the Board and CEQ). A decision was made to investigate the matter further to assess whether and to what extent there was a problem. But based on subsequently gathered information, management concluded that the amounts involved were not material. July 27. 2004: Fourth quarter results were released with no mention of the problem. September 10, 2004: The management representation letter for the annual financial statements and 10- K, dated August 20 2004 and signed by King and Bullock, was delivered to the external auditors (Deloitte & Touche LLP).\" The letter made no mention of the inventory error. October 15, 2004: Prior to releasing results for the first quarter ending September 30, 2004, Molex's management discussed the error for the first time with Deloitte & Touche and proposed recognizing $2 million of the adjustment during the current quarter with additional amounts recognized in subsequent quarters throughout the year. October 19, 2004: At an Audit Committee meeting where the issue was first discussed, Deloitte & Touche disagreed with management's October 15 proposal and argued that the entire error amount should be recorded in the first quarter. The Audit Committee requested that management and Deloitte & Touche work to determine the appropriate accounting,. October 20, 2004: Molex announced its first quarter results: revenues $640 million, net income $55.6 million, and earnings per share $0.29. The full amount of the accounting error ($8 million before-tax and $5.8 million after-tax, of which approximately $3.0 million before-tax and $2.2 million after-tax was related to the year ended June 30, 2004) was included as an adjustment to current operating results, but the error was not disclosed (see Exhibit 4 for a summary of the first quarter results). October 21, 2004: The Audit Committee met again. After the meeting was adjourned, the engagement partner from Deloitte & Touche questioned Diane Bullock as to whether she was aware of the inventory error before signing the September 10, 2004 representation letter. When she confirmed that she had been aware of the problem at that time, Deloitte & Touche expressed concern For financial reporting purposes, materiality was defined as \"the magnitude of an omission or misstatement in the financial statements that makes it probable that a reasonable person relying on those statements would have been influenced by the information or made a different judgment if the correct information had been known\" (FASB Concept Statement Number 2). Interpreting this definition frequently involved the exercise of professional judgment. TA management representation letter is required as part of the audit engagement. The letter is drafted by the auditor, given to the client's management to print on its letterhead, and signed by the CEOQ and CFO. In the letter, management acknowledges that it is responsible for the financial statements, and commits in writing to prior oral representations made to the auditor that were relied on in conducting the audit. The representations are intended to reduce any misunderstandings between the auditors and management. Exhibit 3 provides a sample representation letter. about the significance of the omission to the Audit Committee. Bullock and King responded that, since the error's effect on the firm's financial performance was immaterial, they did not think that it needed to be addressed in the letter. In an attempt to resolve the dispute, the Audit Committee held an inquiry with the help of independent legal and accounting advisors. The inquiry revealed no additional adjustments were required and that management had not deliberately withheld information from the auditors. The Board's Challenge Deloitte & Touche continued to express dissatisfaction over top management's representations. It argued that management had known about the magnitude of the error as early as July 21 and had expressly decided not to inform Deloitte & Touche at that time. Because of this belief, the auditors concluded that they were no longer willing to rely on Bullock and King's representations. In an attempt to satisfy Deloitte & Touche, Molex removed Bullock as CFO and installed an acting CFO; however, she remained an executive officer of the company having responsibilities in the finance area. Subsequently, Deloitte & Touche advised Molex that it would only be able to complete its review of the first quarter results in connection with the company's 10-Q filing when representations were received from the new CFO and a new CEO and if both King and Bullock were removed as executive officers having no influence over financial reporting or internal controls. In November, Molex's Board convened to discuss the situation (see Exhibit 5 for information on the Board of Directors). It appeared to face three options. (1) It could accede to the auditor's request to remove Bullock and King as executive officers so that they would not have any influence over financial reporting or internal controls. (2) It could ignore Deloitte & Touche's demand, forcing the auditor to either refuse to review the quarterly financial statements or to resign. In either case, Molex would be unable to file its quarterly results on time with the SEC and NASDAQ, violating the Exchange's listing requirements. (3) It could dismiss Deloitte & Touche and hire a new auditor, in which case an 8-K would have to be filed with the SEC to explain the change. \fExhibit 2 Molex Incorporated, Ten-Year Financial Highlights Summary, (in thousands, except per share data) 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 Operations Net revenue $2,246,715 $1,843,098 $1,711,497 $2,365,549 $2,217,096 $1,711,649 $1,622,975 $1,539,712 $1,382,673 $1,197,747 Gross profit 776,746 579,248 536,551 859,610 853,892 668, 125 670,266 640,895 562,731 512,498 Income before income taxes 239,892 110,042 93,221 291,416 323,694 230,214 274,823 262,369 228,953 214,492 Income taxes 63,571 24,762 16,684 87,424 100,810 52,363 92,490 95,581 83,300 90,273 Net income 175,950 84,918 76,479 203,919 222,454 178,029 182,243 166,716 145,586 124,035 Earnings per share: Basic 0.93 0.44 0.39 1.04 1.13 0.92 0.93 0.85 0.74 0.63 Diluted 0.92 0.44 0.39 1.03 1.12 0.91 0.92 0.84 0.74 0.63 Net income - percent of net revenue 7.8% 4.6% 4.5% 8.6% 10.0% 10.4% 11.2% 10.8% 10.5% 10.4% Financial Position Current assets 1, 168,644 962,113 915,343 891,865 1,023,009 881,338 867,791 873,614 734,589 773,036 Current liabilities 428,464 356,148 359,593 374,106 475,449 342,441 336,275 342,026 275, 182 278,046 Working capital 740,180 605,965 555,750 517,759 547,560 538,897 531,516 531,588 459,407 494,990 Current ratio 2.7 2.7 2.5 2.4 2.2 2.6 2.6 2.6 2.7 2.8 Property, plant and equipment, net 1,022,378 1,007,948 1,067,590 1,092,567 980,775 809,602 676,161 665,468 613, 125 567,303 Total assets 2,572,346 2,329,870 2,253,920 2,213,627 2,247,106 1,902,012 1,639,634 1,636,931 1,460,999 1,441,020 Long-term debt 10,243 13,137 14,223 19,351 21,593 20,148 5,566 7,350 7.450 8,122 Capital leases 3,796 3,731 3,626 6, 114 Shareholders' equity 2,065,994 1,896,568 1,827,652 1,765,640 1,705,804 1,500,537 1,261,570 1,235,912 1,131,271 1, 107,268 Return on beginning equity 9.3% 4.6% 4.3% 12.0% 14.8% 14.1% 14.7% 14.7% 13.1% 14.1% Dividends per share 0.1 0.1 0.1 0.1 0.09 0.05 0.05 0.04 0.03 0.02 Average common shares: Basic 190,207 191,873 194,327 195,471 196,060 194,340 195,750 196,389 196,768 195,343 Diluted 192,186 193,229 195,986 197,633 198,208 195,631 197,971 198,349 198,819 197,414 Source: Company 10-K, September 10, 2004. Fiscal 2003 results include a charge of $35.0 million ($24.8 million after-tax) for restructuring costs and $5.1 million ($3.8 million after-tax) for write-down of investments. Fiscal 2002 results included a restructuring charge of $24.2 million ($18.8 million after-tax) and a charge for investment impairment of $10.0 million ($6.5 million after-tax). Fiscal 2001 results included a restructuring charge of $30.8 million ($21.4 million after-tax) and a charge for excess and slow moving inventory of $12.7 million ($8.9 million after-tax). "Restated for the following stock dividends: 25%-January 2000; 25%-November 1997; 25%-February 1997; 25%-August 1995; 25%-November 1994.Exhibit 3 Sample Management Representation Letter, written on client letterhead. (Date) (To the Auditor) We are providing this letter in connection with your review of the financial statements of (name of entity) as of (dates) and for the (periods of review e.g. for the years then ended) for the purpose of expressing limited assurance that there are no material modifications that should be made to the statements in order for them to be in conformity with generally accepted accounting principles. We confirm that we are responsible for the fair presentation in the financial statements of financial position, results of operations, and cash flows in conformity with generally accepted accounting principles. Certain representations in this letter are described as being limited to matters that are material. Items are considered material, regardless of size, if they involve an omission or misstatement of accounting information that, in the light of surrounding circumstances, makes it probable that the judgment of a reasonable person relying on the information would be changed or influenced by the omission or misstatement. 1. We confirm, to the best of our knowledge and belief, [as of (the date of the auditor's review report)] the following representations made to you during your review. 2. The financial statements referred to above are fairly presented in conformity with generally accepted accounting principles. We have made available to you all: a. Financial records and related data. b. Minutes of the meetings of stockholders, directors, and committees of directors, or summaries of actions of recent meetings for which minutes have not yet been prepared. 3. There are no material transactions that have not been properly recorded in the accounting records underlying the financial statements.\"? 4. We acknowledge our responsibility to prevent and detect fraud. 5. We have no knowledge of any fraud or suspected fraud affecting the entity involving management or others where the fraud could have a material effect on the financial statements, including any communications received from employees, former employees or others. 6. We have no plans or intentions that may materially affect the carrying amounts or classification of assets and liabilities. 7. There are no material losses (such as from obsolete inventory or purchase or sales commitments) that have not been properly accrued or disclosed in the financial statements. T A substantially lower materiality threshold is used for determining the materiality of a transaction for the management representation letter than is applied for financial reporting purposes. There are no: a. Violations or possible violations of laws or regulations, whose effects should be considered for disclosure in the financial statements or as a basis for recording a loss contingency Unasserted claims or assessments that our lawyer has advised us are probable of assertion that must be disclosed in accordance with Financial Accounting Standards Board (FASB) Statement No. 5 [AC section C59], Accounting for Contingencies. Other material liabilities or gain or loss contingencies that are required to be accrued or disclosed by FASB Statement No. 5 The company has satisfactory title to all owned assets, and there are no liens or encumbrances on such assets, nor has any asset been pledged as collateral. . We have complied with all aspects of contractual agreements that would have a material effect on the financial statements in the event of noncompliance. . The following have been properly recorded or disclosed in the financial statements: a. Related party transactions, including sales, purchases, loans, transfers, leasing arrangements, and guarantees, and amounts receivable from or payable to related parties. Guarantees, whether written or oral, under which the company is contingently liable. Significant estimates and material concentrations known to management that are required to be disclosed in accordance with the AICPA's Statement of Position 94-6, Disclosure of Certain Significant Risks and Uncertainties [Significant estimates are estimates at the balance sheet date that could change materially within the next year. Concentrations refer to volumes of business, revenues, available sources of supply, or markets or geographic areas for which events could occur that would significantly disrupt normal finances within the next year.] [Add additional representations that are unique fo the entity's business or industry| . We are in agreement with the adjusting journal entries you have recommended, and they have been posted to the company's accounts. (if applicable) . To the best of our knowledge and belief, no events have occurred subsequent to the balance-sheet date and through the date of this letter that would require adjustment to or disclosure in the aforementioned financial statements. . We have responded fully and truthfully to all inquiries made to us by you during your review. (Name of Owner or Chief Executive Officer and Title) (Name of Chief Financial Officer and Title, where applicable) Exhibit 4 Molex First Quarter Financial Results for September 30, 2004 Fiscal First Quarter Results Revenue of $640.2 million increased 29 percent from last year's first quarter of $496.8 million. Revenue in local currencies increased 25 percent, as currency translation increased net revenue by approximately $19 million when compared with last year's first quarter. Revenue for the first quarter included $18 million from the automotive acquisition in Europe that was completed on April 2, 2004. Excluding the acquisition, revenue increased 25 percent from last year's first quarter. Net income was $55.6 million compared with last year's first quarter of $32.1 million, an increase of 74 percent. Earnings per share of $0.29 increased 71 percent, compared with $0.17 reported for the first quarter a year ago. Joe King, Vice-Chairman and Chief Executive Officer, said, \"Revenue growth compared with last vear's first quarter revenue was very strong. Revenue also increased sequentially, an excellent result in this seasonally challenging quarter. We believe we are growing significantly faster than the overall connector market, primarily due to our ongoing investment in new products and our global capabilities. We were also pleased with the strong growth in earnings after absorbing higher costs for many of our raw materials.\" Regional Results Revenue in the Far East South region was $190 million, an increase of 33 percent, primarily driven by the digital consumer, PC, and mobile communication markets. In this region, we continue to gain market share, based on our many new products and increased penetration into our global customers who continue to transfer production to the region. Revenue in the Far East North region (Japan and Korea) was $132 million, an increase of 13 percent in dollars and 6 percent in local currencies. This growth was primarily due to new products for the digital consumer and communication markets. Revenue in the Americas region was $177 million, an increase of 17 percent, due to stronger demand for high-speed, industrial and medical electronics products, which more than offset lower demand in automotive. Revenue in Europe was $128 million, an increase of 73 percent in dollars and 61 percent in local currencies. Excluding the previously mentioned automotive acquisition, revenue increased 49 percent in dollars, as the region recovers from recession. Operating Results Gross profit margin was 35.7 percent compared with last year's first quarter margin of 33.8 percent. Pretax return on sales was 12 percent compared with 8.9 percent in the year ago quarter. The effective tax rate for the first quarter was 27 percent, the same rate as last year's first quarter. The Company now anticipates an effective tax rate of 27 percent for the 2005 fiscal year, compared with previous guidance of 27.5 percent and a 2004 fiscal year rate of 26.5 percent. Net return on sales was 8.7 percent compared with 6.5 percent in last year's first quarter. Cash and marketable securities were $331.4 million at September 30, 2004. The Company's order backlog on September 30, 2004 stood at $313.6 million, a 51 percent increase compared with $208 million for the same period last year. Without the impact of changes in currency rates, the order backlog would have increased 48 percent. New orders for the first quarter were $622.4 million, an increase of 21 percent compared with last year's first quarter. This was a reasonable result, considering an estimated $25 million in orders were advanced by customers into the June quarter, as discussed in the June 30, 2004 earnings release. Research and Development Expenditures and Capital Spending Research and development expenditures for the first quarter were $33.4 million, an increase of 24 percent when compared with the same period last year. Capital expenditures were $48.4 million for the quarter versus $45.3 million last year. Fiscal Second Quarter Outlook King continued, "Our operations in the Far East continue to drive our results. We expect this trend to continue, based on the magnitude of production transferred by our global customers to the region and supported by our technical capabilities and long term history of working in the region.\" It is apparent that many of our customers in the Americas are in the process of adjusting their finished goods inventory to more conservative levels. However, we believe that the amount of actual connector inventory within these channels is reasonable, and therefore the outlook in the majority of our markets remains encouraging. In addition, we expect to gain market share based on our positions within key market segments - such as digital consumer, mobile communication and mobile computing - that are growing faster than the overall connector market, as well as our focus on the emerging medical electronics market. Based on these facts, the Company expects that revenue for the fiscal second quarter ending December 31, 2004, will be in a range of $635 - $650 million. This represents an increase of 16 - 18 percent over last vear's fiscal second quarter. The Company expects that earnings per share will be in a range of $0.29 - $0.31, an increase of 38 - 48 percent over last year's fiscal second quarter earnings per share. Stock Buyback Actions During the quarter, the Company purchased 875,000 shares of MOLXA common stock, at a total cost of $21.9 million. These purchases were done under a $100 million Board authorization for the full fiscal year ending June 30, 2005. Exhibit 4 {(continued) Consolidated Balance Sheet (unaudited, in thousands) Sept. 30, June 30, 2004 2004 ASSETS Current assets: Cash and cash equivalents $238.292 $234 431 Marketable securitics 93,153 104,223 Accounts receivable, net 544,736 329,630 Inventories 283417 265,344 Other current assets 40,027 35,016 Total current assets 1,199,625 1,168,644 Property, plant and equipment, net 1,009,163 1,022 378 Goodwill 164,969 164,915 Other assets 194,930 216,409 Total assets $2,.568.687 $2.572,346 LIABILITIES AND SHAREHOLDERS' EQUITY Current liabilities: Accounts payable $225,731 $234,823 Accrued expenses 132,625 143,160 Other current liabilities 47,508 50.481 Total current liabilities 405,864 428.464 Other non-current liabilities 9,361 10,487 Accrued pension and postretirement benefits 51,435 52,151 Long-term debt 10,075 10,243 Obligations under capital leases 3,143 3,796 Minority interest in subsidiaries 3,383 1,211 Shareholders' equity: Common Stock 10,747 10,734 Paid-in capital 376,518 369,660 Retained earnings 2,209,211 2,160,368 Treasury stock -532,216 -509,161 Deferred unearned compensation -32,722 -32,180 Accumulated other comprehensive income 53,888 66,573 Total shareholders' equity 2,085,426 2,065,994 Total liabilities and shareholders' equity $2.568.687 $2,572,346Exhibit 4 (continued) Consolidated Income Statement (unaudited, in thousands, except per share data) September 30 2004 2003 Net Revenue $640,230 $496.763 Cost of sales 411,558 328,739 GROSS PROFIT 228.672 168,024 Selling, general and administrative expenses: Selling 54,020 44 416 General and administrative 102,192 83,048 Total selling, general and administrative expenses 156,212 127,464 INCOME FROM OPERATIONS 72.460 40,560 Other (income) expense: Equity income (2,029) (2,183) {Gain)/loss on investments (1,152) Interest, net (925) (1,235) Total other (income) expense (4.106) (3.418) INCOME BEFORE INCOME TAXES AND MINORITY INTEREST 76,566 43978 Income taxes and minority interest 20,924 11,916 NET INCOME $55,642 $32,062 EARNINGS PER SHARE: Basic 0.29 $0.17 Diluted 0.29 $0.17 AVERAGE COMMON SHARES OUTSTANDING: Basic 188,763 190,679 Diluted 190,617 192,372 _CASHDIVIDENDSPERSHARE = 8004 $0.03 Source: Company Press Release, 20 October 2004. Exhibit 5 Molex Board of Directors Frederick A. Krehbiel Co-Chairman of the Board of Molex. Director since 1972 and member of the Executive Committee. Age 63. Elected Vice Chairman and Chief Executive Officer in 1988 and Chairman of the Board of Directors in 1993. Became Co-Chairman in 1999 and served as Co-Chief Executive Officer from 1999-2001. Owned 28.0% of voting common stock. Also served on the boards of Tellabs, Inc., W. W. Grainger, Inc. and Devry Inc. John H. Krehbiel, Jr. Co-Chairman of the Board of Molex. Director since 1966 and member of the Executive Committee. Age 67. President of Molex 1975-1999 and Chief Operating Officer 1996- 1999. Became Co-Chairman in 1999 and served as Co-Chief Executive Officer from 1999-2001. Owned 32.8% of voting common stock. Michael J. Birck Director since 1995. Member of the Audit Committee and the Executive Committee. Age 66. Founder and Chairman of the Board of Tellabs, Inc. (telecommunications equipment). Also served on the board of Illinois Tool Works Inc. Douglas K. Carnahan Director since 1997 and Chairman of the Audit Committee. Age 63. Retired former executive of Hewlett-Packard Company (computers, computer peripherals and instrumentation). Michelle L. Collins Director since 2003 and member of the Nominating and Corporate Governance Committee. Age 44. Co-founder and Managing Director of Svoboda, Collins LLC (private equity firm), and former partner of William Blair & Company, LLC (1992-97). Also served on the board of CDW Corporation. Edgar D. Jannotta Director since 1986. Chairman of the Nominating and Corporate Governance Committee and member of the Executive Committee. Age 73. Investment banker and Chairman of William Blair & Company, LLC. (securities and investment banking). Also served on the boards of Bandag, Incorporated, Aon Corporation and Exelon Corporation. J. Joseph King Vice Chairman of the Board and Chief Executive Officer of Molex. Director since 1999 and member of the Executive Committee. Age 60. Owned 0.2% of voting common stock, and 201,293 stock options. Also served on the board of Cabot Microelectronics Corporation. Fred L. Krehbiel Director since 1993. Age 39. President of Molex Connector Products Division (Americas). Worked at Molex since 1988 in various engineering, marketing and managerial capacities. Previously served as Assistant to the Regional President (Americas) for the Global Desktop Business (1998-2000) and President of the Automotive Division (Americas) (2000-2003) Owned 1.0% of voting common stock and 6,250stock options.Joe W. Laymon Director since 2002 and member of the Compensation Committee. Age 51. Group Vice President, Corporate Human Resources & Labor Affairs of Ford Motor Company (automobile manufacturer). Previously worked for U.S. State Department-Agency for International Development, Human Resource at Xerox Corporation (1979-1996) and Eastman Kodak Company (1996-2000). 10 polex's Audit Committee does not have a \"Financial Expert\" as defined (but not required) by the applicable SEC Rules. In its Proxy Statement, the company explained that, \"given the level of financial sophistication and business experience of the Audit Committee members, the board of directors believes that the Audit Committee members can perform the aundit committee functions as required.\" Donald G. Lubin Director since 1994 and member of the Nominating and Corporate Governance Committee. Age 70. Partner of Sonnenschein Nath & Rosenthal (private law practice). Also served on the board of McDonald's Corporation. Masahisa Naitoh Director since 1995 and member of the Compensation Committee. Age 66. Chairman and CEO of The Institute of Energy Economics, Japan (private think tank). Previously held senior positions at The Institute of Energy Economics and Itochu Corporation (a Japanese global trading firm). Also served on the board of E. I. DuPont de Nemours and Company. Robert J. Potter Director since 1981. Chairman of the Compensation Committee and member of the Audit Committee. Age 71. President and Chief Executive Officer of R. ]. Potter Company (consulting business). Also served on the boards of Cree, Inc. and Zebra Technologies Corporation. Martin P. Slark Director since 2000 and member of the Executive Committee. Age 49. President and Chief Operating Officer of Molex. Worked at Molex since 1976 filling various administrative, operational and executive positions both internationally and domestically. Served as Executive Vice President from 1999-2001, and assumed the post of President and Chief Operating Officer on July 1, 2001. Owned 0.1% of voting common stock and 137,623 stock options. Also served on the board of directors of Hub Group, Inc. Source: Company Proxy Statement, September 15, 2004

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Accounting Questions!