Question: here is the question, Suppose that you are given the following zero-curve (interest rates are per year rates, and compounded semi-annually): Question A: Trading on

here is the question, Suppose that you are given the following zero-curve (interest rates are per year rates, and compounded semi-annually):

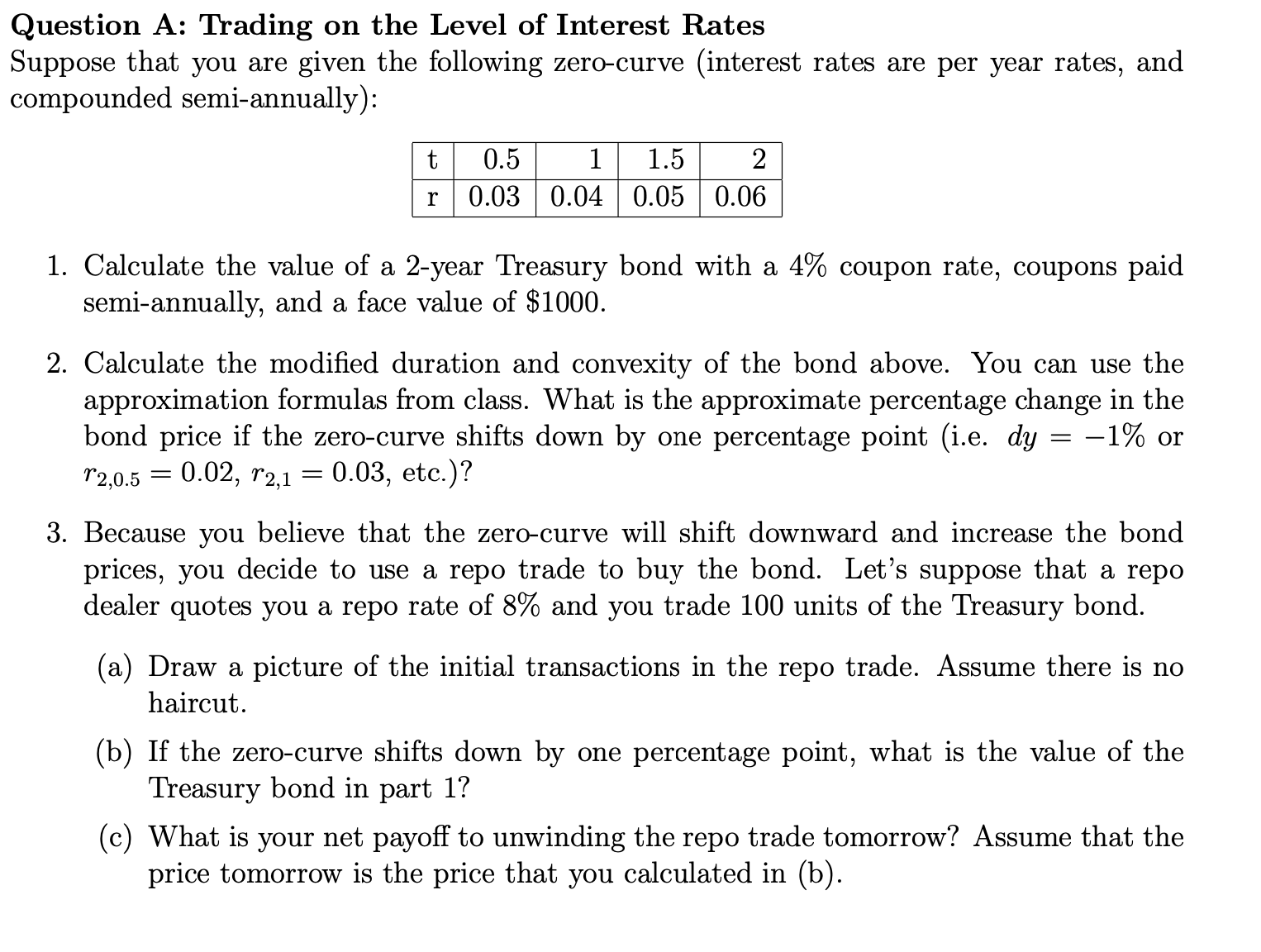

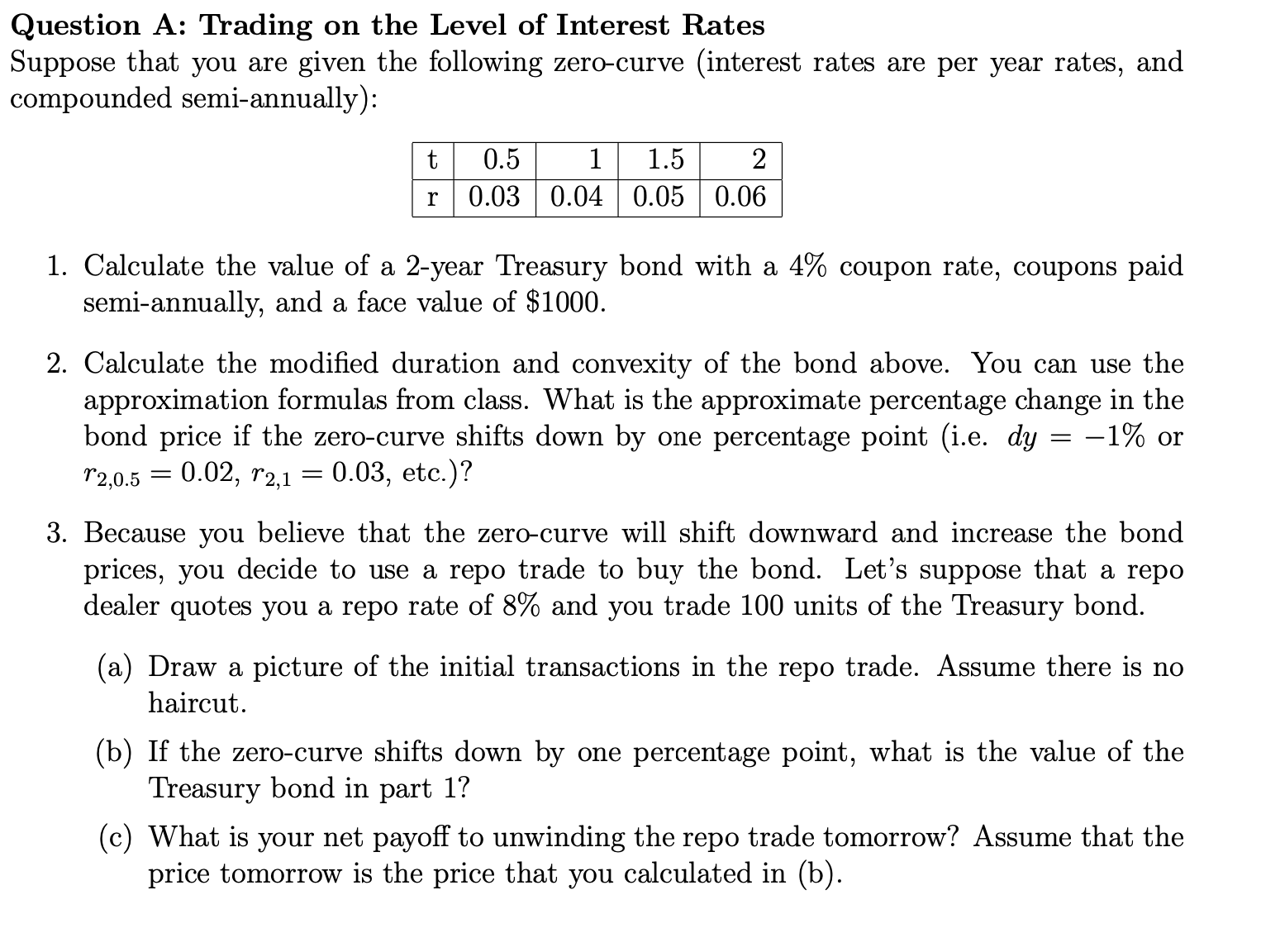

Question A: Trading on the Level of Interest Rates Suppose that you are given the following zero-curve (interest rates are per year rates, and compounded semi-annually): |t 0.5 1 | r 0.03 0.04 1.5 0.05 2 0.06 1. Calculate the value of a 2-year Treasury bond with a 4% coupon rate, coupons paid semi-annually, and a face value of $1000. 2. Calculate the modied duration and convexity of the bond above. You can use the approximation formulas from class. What is the approximate percentage change in the bond price if the zero-curve shifts down by one percentage point (i.e. dy = 1% or T2415 = 0.027 T2; = 0.03, etc.)? 3. Because you believe that the zero-curve will shift downward and increase the bond prices, you decide to use a repo trade to buy the bond. Let's suppose that a repo dealer quotes you a repo rate of 8% and you trade 100 units of the Treasury bond. (a) Draw a picture of the initial transactions in the repo trade. Assume there is no haircut. (b) If the zero-curve shifts down by one percentage point, what is the value of the Treasury bond in part 1? (c) What is your net payoff to unwinding the repo trade tomorrow? Assume that the price tomorrow is the price that you calculated in (b)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts