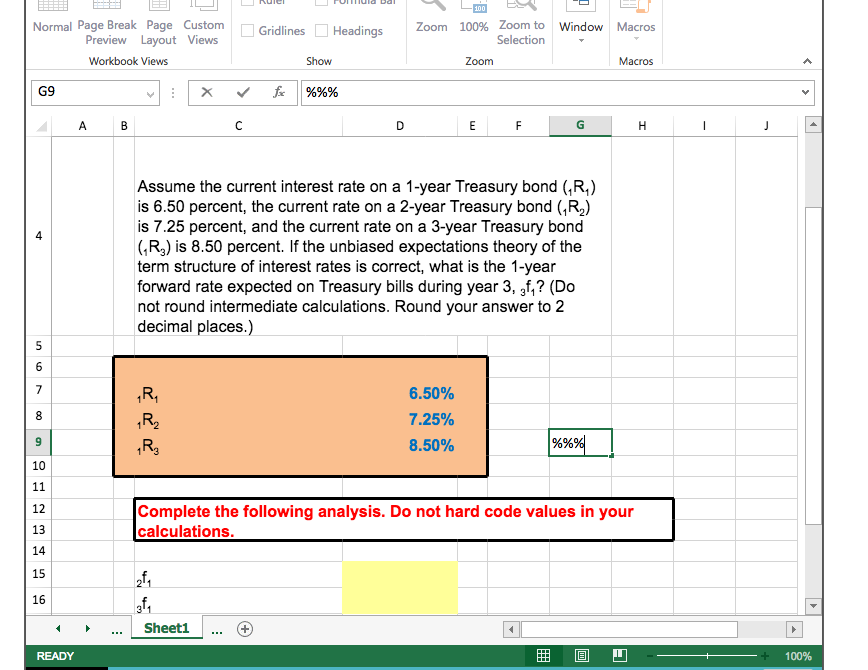

Question: Hi Can you answer this question for me. I do not understand it? End w lg] l|_l |_| nulltrl |_| rullllula Bill '5' LE lit-

Hi Can you answer this question for me. I do not understand it?

![understand it? End w lg] "l|_l |_| nulltrl |_| rullllula Bill '5'](https://s3.amazonaws.com/si.experts.images/answers/2024/06/666224a45ece8_940666224a43d7d5.jpg)

End w lg] "l|_l |_| nulltrl |_| rullllula Bill '5' LE lit- 'EI ELI MurmalPageBreak Page Custom DGridline-s DHeavdings Zoom 100% Zoomto \i'll'indaw Macros Preview Layout Views Selection v Workbookm Show Zoom Macros A '59 v E x v' fr 969% v A e c . c . E . F G H 1 Assume the cun'ent interest rate on a 1-year Treasury bond (1R1) is 8.50 percent. the current rate on a 2-year Treasury bond [1 R2) 4 is 7.25 percent. and the current rate on a 3-year Treasury bond (1R3) is 8.50 percent If the unbiased expectations theory of the term structure of interest rates is ccn'ect. what is the 1-year forward rate expected on Treasury bills during year 3. J1? (Do not round intermediate mlwlaticns. Round your answer to 2 decimal - laces. .- - -m-- I-- I Complete the following analysis. Do not hard code values In your I calculations

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts