Question: Hi! Can you help me answer this practice HW. Here is the reading itself as well as the questions. 1. Referring to Carrefour's financials for

Hi!

Can you help me answer this practice HW. Here is the reading itself as well as the questions.

1. Referring to Carrefour's financials for Thailand (see Case Exhibit 19.1), compute the days sales outstanding ratios for accounts receivable (A/Rs) and its payment deferral ratio for accounts payable (A/Ps). What is Carrefour's cash conversion cycle? What does it mean for Carrefour's working capital requirement and financing needs? How would you characterize Carrefour's competitive strategy in Thailand?

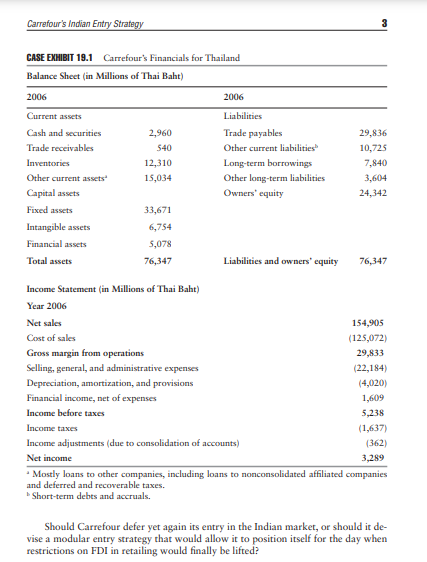

CASE STUDY 19.1 Carrefour's Indian Entry Strategy This case study accompanies Chapter 19 of International Corporate Finance. It is the last and a very big frontier. Brazil is done, China is done. India is the last Shangri-la of retail. Where will Tesco and Walmart get their growth? Sunil B. Mittal, chairman and managing director, Bharti Enterprises Led. Albert Montgolfier is the deputy head of Carrefour's strategic planning depart- ment. He has been charged with a review of Carrefour's options with respect to the Indian market and would submit his preliminary recommendations to Carrefour's board meeting next April (2007). India had been on Carrefour's radar for some time now, and, as late as 2004, Carrefour had been close to entering the Indian mar- ket through franchising but decided to defer any strategic move. Bharti Enterprises' recent announcement, in late November 2006, of a large-scale joint venture with Walmart' changed the competitive landscape in a major way, and Albert knew that Carrefour could not defer and temporize forever, as time was of essence. For "big box" retailers-the likes of Walmart, Ahold, Tesco, or Carrefour-India was the last uncharted frontier. Indeed, with more than 1.1 billion people, half of them 25 years old or younger, an economy growing at an annual rate of 8 to 10 percent, and no major retail chain to speak of, India represented in 2006 a US$250 billion market po- tential, widely expected to double within 10 years. Retail was estimated to contribute 14 percent of India's gross domestic product, employed 21 million people, and was indeed a mainstay of the Indian economy-second only to its agricultural sector. Yet, India's retail sector was highly fragmented, with as many as 12 million outlets-owner-operated general or convenience stores, also known as kirana shops, which included handcart and pavement vendors. This unorganized sector accounted for more than 95 percent of Indian retail and generally operated in floor space of 500 square feet or less. The dearth of organized major retail chains when viewed in a context of a boom- ing economy and an emerging middle class numbering a quarter of a billion people provided a tantalizing opportunity for both domestic firms and multinational retail giants, except that India was closed to foreign direct investment (FDI) in retailing. According to Sunil Mittal, "Government policy allows foreign equity in back-end wholesale, logistics, and real estate, so we'll do a joint venture partnership in those areas and we will own the retail business 100 percent until the government allows FDI (foreign direct investment) there, and then we'll do a joint venture with our partner."CASE STUDY Yet India, long shackled by an overzealous bureaucracy, had since 1991 steadily relaxed restrictions on FDI in most sectors of its economy, including real estate and wholesale trading-but not retailing-which raised speculation as to if and when entry by major foreign retailers would be allowed. An encouraging omen was the lifting of restrictions for single-brand retailers. Indian firms, for their part, were in the early stages of major investment to take ad- vantage of legal entry barriers that-for the time being-kept at bay formidable mul- tinational retailers. For example, the Tata Group owned the Westside group and was developing a retail chain for consumer goods under the name of Croma. Croma was partly a joint venture with Woolworth, which owned the wholesale operation (allowed under FDI law) and supplied the retail stores owned by the Tata group. In a similar vein, Reliance Industries announced in 2006 an ambitious plan to invest US$5.5 bil- lion over five years to open 1,000 hypermarkets and 1,500 convenience stores. As in the cases of all other major markets, big box retailers were perceived by existing mom-and-pop corner stores as a tsunami that would devastate the sector and throw millions of people out of work. Carrefour had waged the same battle over and over again starting with France in the 1960s before turning to similarly at- omistic retail sectors in Spain, Brazil, Thailand, China, and many others. For public authorities the policy conundrum was not easy to resolve: On the one hand modern, large-scale retailers brought economies of scale efficiency gains to distribution and lower prices to end consumers by streamlining the supply chain. For food products, greater sanitation through a modern cold chain for fresh produce and much-reduced waste were obvious welfare benefits for the consumer. On the other hand, large-scale retailers would displace millions of mom-and-pop stores, adding to the 40 million or so of unemployed. Large-scale demonstrations by threatened shopkeepers would only become more militant as more pressure was being applied on the Congress party currently in power. Even if FDI restrictions were lifted, Carrefour was well aware of the daunting hurdles that it would face, especially in the food sector, which accounted for ap- proximately half of its revenue. Absence of modern logistics and a dilapidated infra- structure would be a major part of the challenge. Lacking proper storage facilities and refrigerated trucks, the world's second-largest producer of fresh produce was es- timated to lose to spoilage and waste as much as a third of its output.' To make mat- ters worse, India was weighed down by a byzantine system of government-mandated intermediaries who deployed an army of agents collecting various transit fees along the way from the original farmer to the final consumer.' Needless to say, this cas- cade of fees levied from the farm to the retail store shelf increased the cost of the product as much as fivefold. Would Carrefour be able to exploit the same competi- tive advantage that it had honed in other markets starting in France in the 1960s? One of its recent success stories was Thailand, for which financials are provided in Case Exhibit 19.1. "There were fewer than 5,000 cold storage facilities, providing enough capacity for 10 percent of what India produced. *Nationwide there were approximately 415,000 government-licensed traders and 210,000 licensed commission agents who hawk farmers' goods on their behalf and take a cut of the transaction.Carrefour's Indian Entry Strategy CASE EXHIBIT 19.1 Carrefour's Financials for Thailand Balance Sheet (in Millions of Thai Baht) 2006 2006 Current assets Liabilities Cash and securities 2,960 Trade payables 29,836 Trade receivables $40 Other current liabilities" 10,725 Inventories 12,310 Long-term borrowings 7,840 Other current assets' 15,034 Other long-term liabilities 3,604 Capital assets Owners' equity 24,342 Fixed assets 33,671 Intangible assets 6,754 Financial assets 5,078 Total assets 76,347 Liabilities and owners' equity 76,347 Income Statement (in Millions of Thai Baht) Year 2006 Net sales 154,905 Cost of sales (125,072) Gross margin from operations 29,833 Selling, general, and administrative expenses (22,184) Depreciation, amortization, and provisions (4,020) Financial income, net of expenses 1,609 Income before taxes 5,238 Income taxes (1,637) Income adjustments ( due to consolidation of accounts) (362) Net income 3,289 Mostly loans to other companies, including loans to nonconsolidated affiliated companies and deferred and recoverable taxes. Short-term debts and accruals. Should Carrefour defer yet again its entry in the Indian market, or should it de- vise a modular entry strategy that would allow it to position itself for the day when restrictions on FDI in retailing would finally be lifted

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!