Question: Hi , can you please help me answer this case study by using the handitax? 1) Case Study John Waite isan Australian resident. He works

Hi , can you please help me answer this case study by using the handitax?

1) Case Study

John Waite isan Australian resident. He works full-time as a civil engineer foran engineering firm, Odyssey Engineering, based in Brisbane City. John lives in a three-bedroom house in Indooroopilly with his wife of seventeen years, Alison, and their two children, Zac, aged ten and Imogen, aged seven. John and Alison purchased this property in joint names in June 2016 for $1,250,000 and have lived there with their children since that date. As such, they regard this property as their main residence.

John has various investments, including shares in listed Australian companies and a rental property at Nundah, which was bought in his own name during the 2022 income year.

Required:Prepare his 2022 income tax return usingHandiTaxsoftware program with full copy and minimise his 2022 taxable income wherever legally possible.

2) Capital Gain/Losses

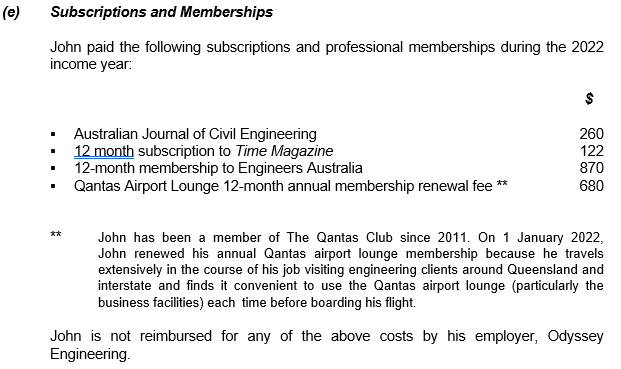

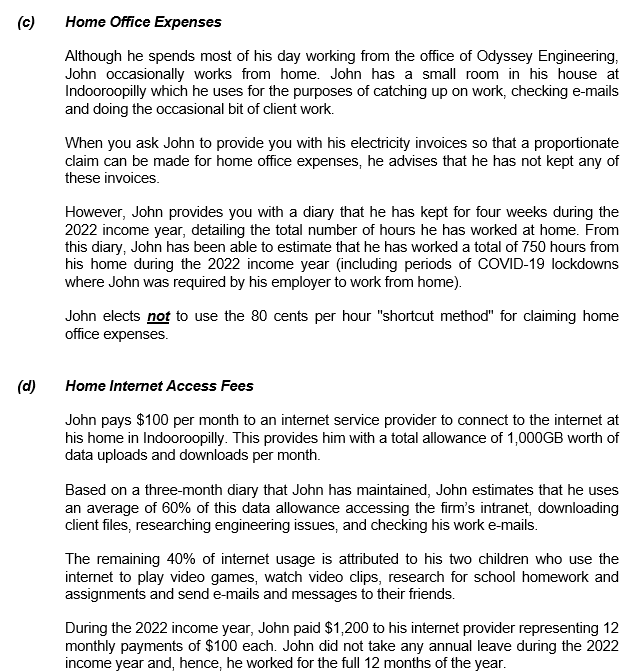

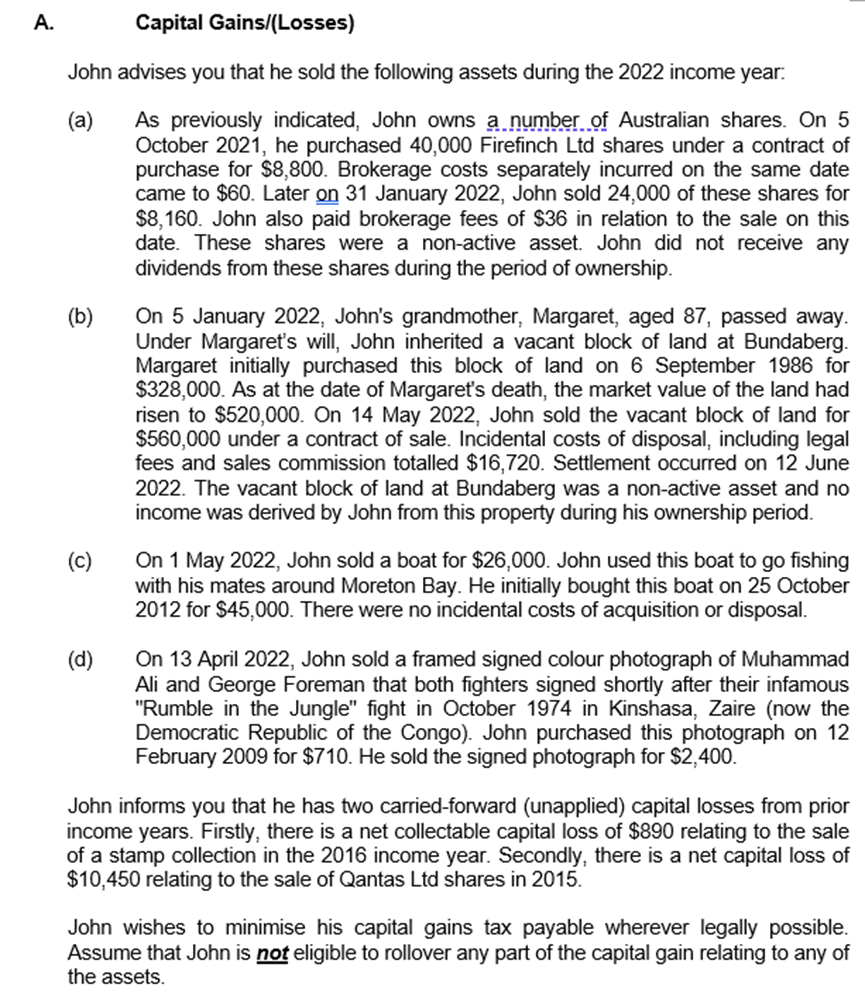

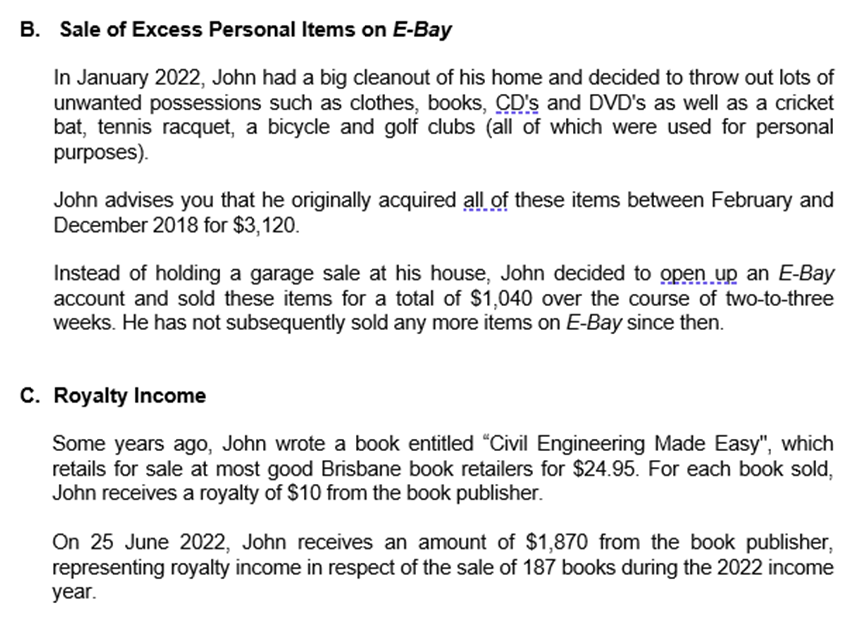

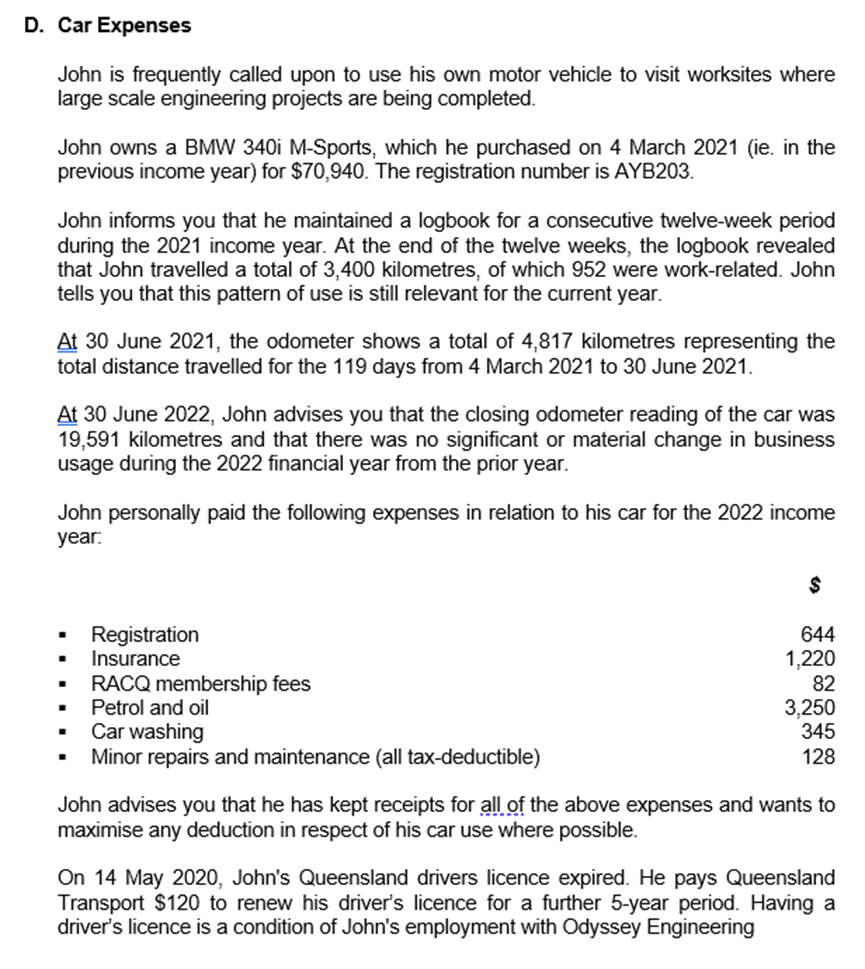

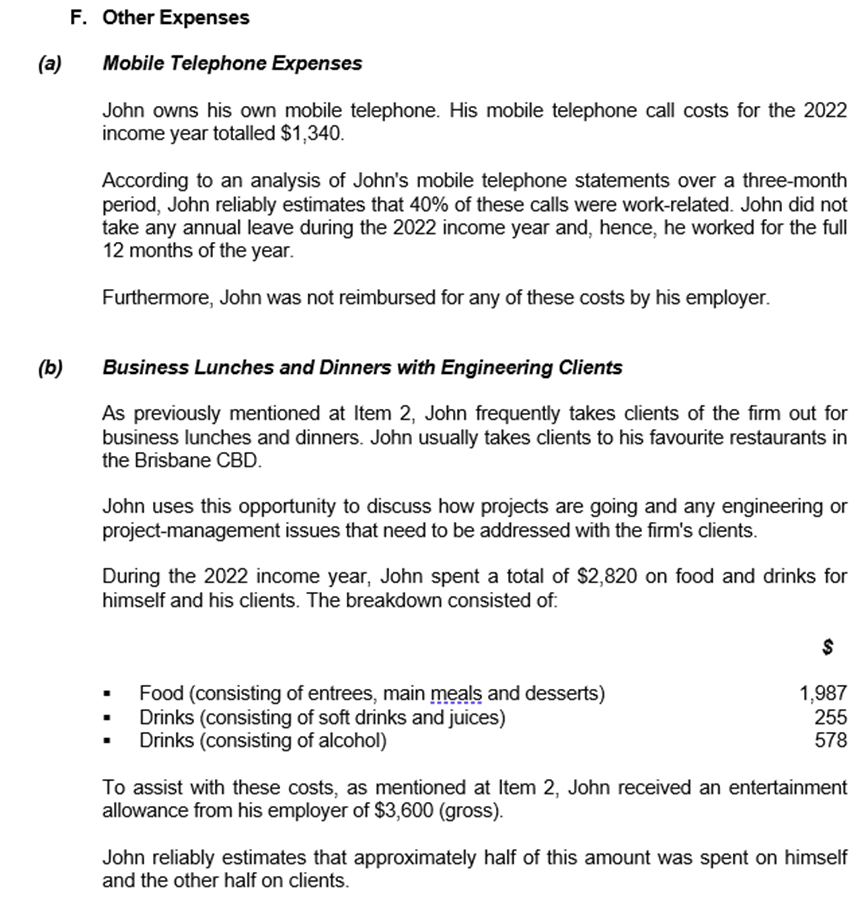

(Fr) Subscriptions and Memberships John paid the following subscriptions and professional memberships during the 2U22 income year: 3 - Australian Journal of Civil Engineering 26G - 133351th subscription to Time Magazine 122 - 12month membership to Engineers Australia STE - Qantas Airport Lounge 12month annual membership renewal fee \"1 68G '1 John has been a member of The Qantas Club since 2D'l1. On 1 January 2022, John renewed his annual Qantas airport lounge membership because he travels extensively in the course of his job visiting engineering clients around Queensland and interstate and nds it convenient to use the Qantas airport lounge {particulady the business facilities} each time before boarding his ight. John is not reimbursed for any of the above costs by his employer, Odyssey Engineering. (G) (d) Home Ofce Expenses Although he spends most of his day worldng from the ofce of Odyssey Engineering, John occasionally works from home. John has a small room in his house at Indooroopilly which he uses for the purposes of catching up on work, checking e-mails and doing the occasional bit of clientwork. When you ask John to proyide you with his electricity inyoices so that a proportionate claim can be made for home ofce expenses, he adyises that he has not kept any of these inyoices. Howeyer, John proyides you with a diary that he has kept for four weeks during the 2022 income year, detailing the total number of hours he has worked at home. From this diary, John has been able to estimate that he has worked a total of ?50 hours from his home during the 2022 income year {including periods of CD'y'lD10 lockdowns where John was required by his employer to work from home}. John elects n_ot to use the 80 cents per hour "shortcut method" for claiming home of ce expenses. Home internet Access Fees John pays $100 per month to an internet seryice provider to connect to the internet at his home in Indooroopilly. This provides him with a total allowance of 1,000GB worth of data uploads and downloads per month. Based on a threemonth diary that John has maintained, John estimates that he uses an average of 00% of this data allowance accessing the n'n's intranet, downloading client les, researching engineering issues, and checking his work emails. The remaining 40% of internet usage is attributed to his two children who use the internet to play yideo games, watch yideo clips, research for school homework and assignments and send emails and messages to their friends. During the 2022 income year, John paid $1,200 to his internet proyider representing 12 monthly payments of $100 each. John did not take any annual leaye during the 2022 income year and, hence, he worked for the full 12 months of the year. Capital Gainsl(Losses) John advises you that he sold the following assets during the 2022 income yeah (a) (b) (C) (d) October 2021, he purchased 40,000 Firench Ltd shares under a contract of purchase for $8,800. Brokerage costs separately incurred on the same date came to $60. Later g 31 January 2022, John sold 24,000 of these shares for $8,160. John also paid brokerage fees of $36 in relation to the sale on this date. These shares were a non-active asset. John did not receive any dividends from these shares during the period of ownership On 5 January 2022, John's grandmother, Margaret, aged 87, passed away. Under Margaret's will, John inherited a vacant block of land at Bundaberg. Margaret initially purchased this block of land on 6 September 1986 for $328,000. As at the date of Margaret's death, the market value of the land had risen to $520,000. On 14 May 2022, John sold the vacant block of land for $560,000 under a oontract of sale. Incidentat costs of disposal, including legal fees and sales commission totalled $16,720. Settlement occurred on 12 June 2022. The vacant block oi land at Bundaberg was a non-active asset and no income was derived by John from this property during his ownership period. On 1 May 2022, John sold a boat for $26,000. John used this boat to go shing with his mates around Moreton Bay. He initially bought this boat on 25 October 2012 for $45,000. There were no incidental costs of acquisition or disposal. On 13 April 2022, John sold a framed signed colour photograph of Muhammad Ali and George Foreman that both ghters signed shortly after their infamous "Rumble in the Jungle" ght in October 19?4 in Kinshasa, Zaire (now the Democratic Republic of the Congo). John purchased this photograph on 12 February 2009 for $710. He sold the signed photograph for $2,400. John informs you that he has two carried-toward (unapplied) capital losses from prior income years. Firstly, there is a net collectable capital loss of $890 relating to the sale of a stamp collection in the 2016 income year. Secondly, there is a net capital loss of $10,450 relating to the sale of Qantas Ltd shares in 2015. John wishes to minimise his capital gains tax payable wherever legally possible. Assume that John is n_ot eligible to rollover any part of the capital gain relating to any of the assets. B. Sale of Excess Personal Items on 582:}! In January 2022, John had a big cleanout of his home and decided to throw out lots of unwanted possessions such as clothes, books, 9122's and DVD's as well as a cricket bat, tennis racquet. a bicycle and golf clubs (all of which were used for personal purposes). John advises you that he originally acquired aI_I__Qf these items between February and December 2018 for $3,120. Instead of holding a garage sale at his house, John decided to pygmy]; an EBay account and sold these items for a total of $1.040 over the course of two-to-three weeks. He has not subsequently sold any more items on EBay since then. C. Royalty Income Some years ago, John wrote a book entitled \"Civil Engineering Made Easy". which retails for sale at most good Brisbane book retailers for $24.95. For each book sold, John receives a royalty of $10 from the book publisher. On 25 June 2022, John receives an amount of 31,8?0 from the book publisher, representing royalty income in respect of the sale of 187 books during the 2022 income year D. Car Expenses John is frequently called upon to use his own motor vehicle to visit worksites where large scale engineering projects are being completed. John owns a BMW 340i hit-Sports, which he purchased on 4 March 2021 (ie. in the previous income year) for $70,940. The registration number is AYB203. John informs you that he maintained a logbook for a consecutive twelve-week period during the 2021 income year. At the end of the twelve weeks, the logbook revealed that John travelled a total of 3,400 kilometres, of which 952 were work-related. John tells you that this pattern of use is still relevant for the current year. Q 30 June 2021, the odometer shows a total of 4,817 kilometres representing the total distance travelled for the 119 days from 4 March 2021 to 30 June 2021. g 30 June 2022, John advises you that the closing odometer reading of the car was 19,591 kilometres and that there was no signicant or material change in business usage during the 2022 nancial year from the prior year. John personally paid the following expenses in relation to his car for the 2022 income yeac S - Registration 644 - Insurance 1,220 - RACQ membership fees 82 - Petrol and oil 3,250 - Car washing 345 - Minor repairs and maintenance (all tax-deductible) 128 John advises you that he has kept receipts for aligf the above expenses and wants to maximise any deduction in respect of his car use where possible. On 14 May 2020, John's Queensland drivers licence expired. He pays Queensland Transport $120 to renew his driver's licence for a further 5-year period. Having a driver's licence is a condition of John's employment with Odyssey Engineering \f(a) (b) F. Other Expenses Mobile Telephone Expenses John owns his own mobile telephone. His mobile telephone call costs for the 2022 income year totalled $1 ,340. According to an analysis of John's mobile telephone statements over a three-month period, John reliably estimates that 40% of these calls were work-related. John did not take any annual leave during the 2022 income year and, hence, he worked for the full 12 months of the year. Furthermore, John was not reimbursed for any of these costs by his employer. Business Lunches and Dinners mm Engineering Ciients As previously mentioned at Item 2, John frequently takes clients of the rm out for business lunches and dinners. John usually takes clients to his favourite restaurants in the Brisbane CEO. John uses this opportunity to discuss how projects are going and any engineering or project-management issues that need to be addressed with the nn's clients. During the 2022 income year, John spent a total of $2,820 on food and drinks for himself and his clients. The breakdown consisted of: $ - Food (consisting of entrees, main [meals and desserts) 1:987 - Drinks (consisting of soft drinks and juices) 255 - Drinks (consisting of alcohol) 578 To assist with these costs, as mentioned at Item 2. John received an entertainment allowance from his employer of $3,600 (gross). John reliably estimates that approximately half of this amount was spent on himself and the other half on clients

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock

Students Have Also Explored These Related Finance Questions!