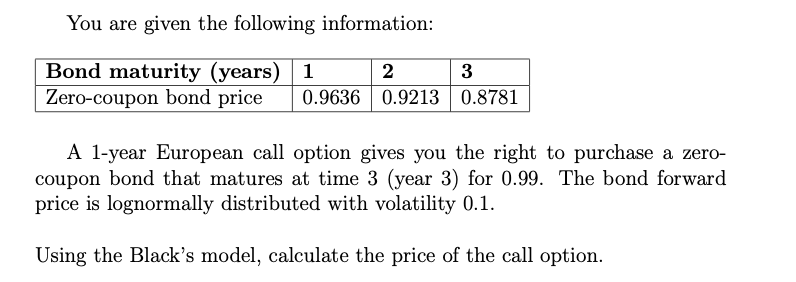

Question: Hi, could I please get help with this problem? Thank you :) You are given the following information: -_E- 0.9636 {3.9213 {3.3731 A 1-year European

Hi, could I please get help with this problem? Thank you :)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock