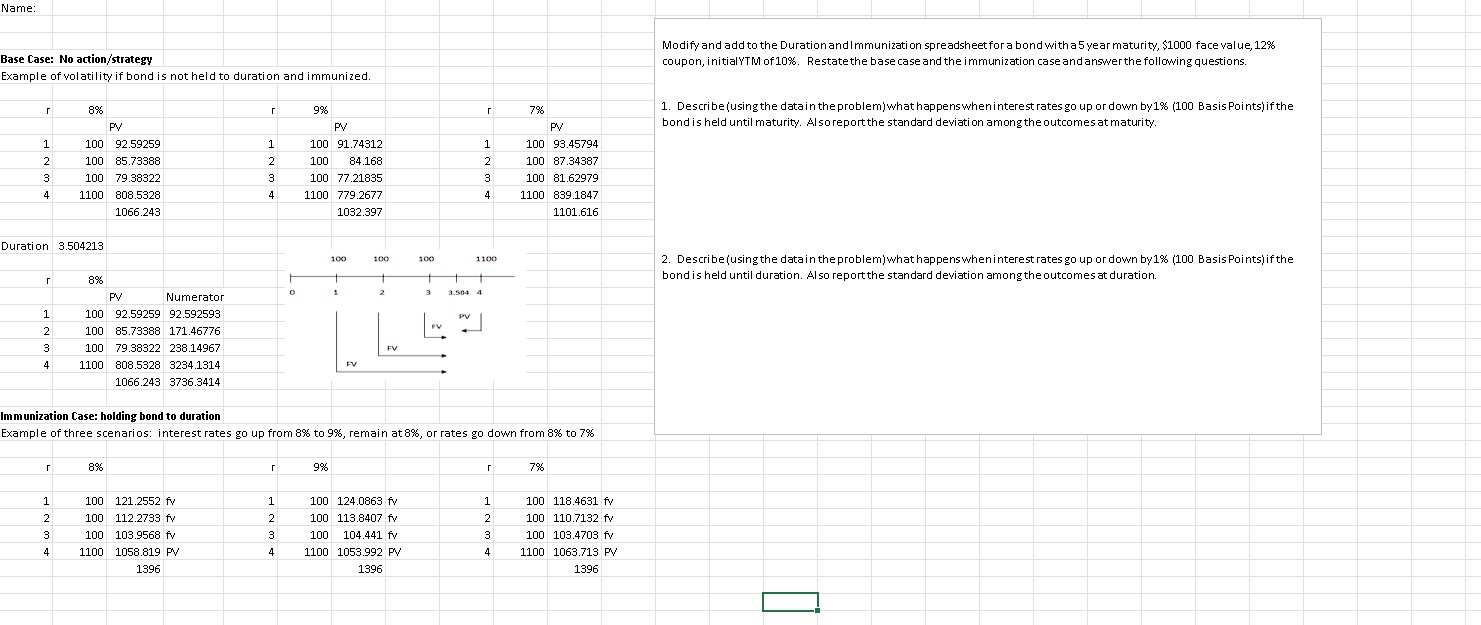

Question: Hi for this problem I need to modify and add to the Duration and Immunization spreadsheet for a bond with a 5 year maturity, $

Hi for this problem I need to modify and add to the Duration and Immunization spreadsheet for a bond with a year maturity, $ face value, coupon, initial YTM of Restate the base case and the immunization case and answer the following questions.

Describe using the data in the problem what happens when interest rates go up or down by Basis Points if the bond is held until maturity. Also report the standard deviation among the outcomes at maturity.

Describe using the data in the problem what happens when interest rates go up or down by Basis Points if the bond is held until duration. Also report the standard deviation among the outcomes at duration.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock