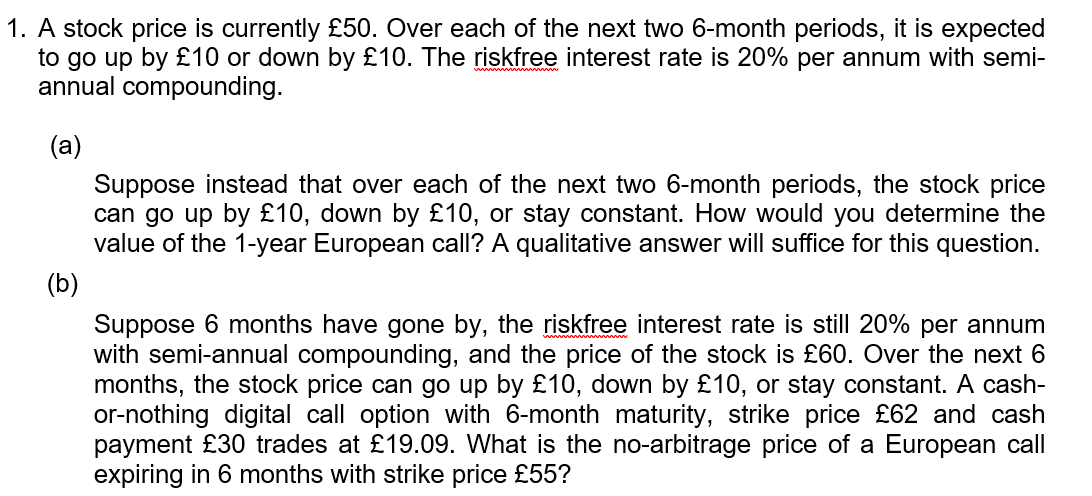

Question: Hi, needed help on this question please. 'i. A stock price is currently 50. Over each of the next two 6-month periods, it is expected

Hi, needed help on this question please.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock