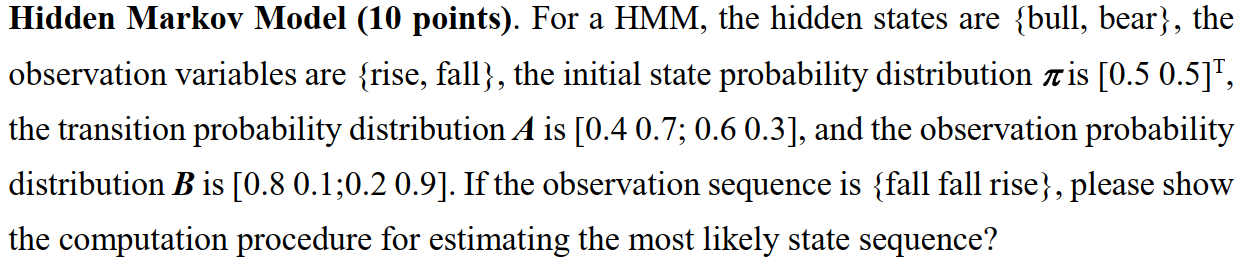

Question: Hidden Markov Model (10 points). For a HMM, the hidden states are {bull, bear}, the observation variables are {rise, fall}, the initial state probability distribution

Hidden Markov Model (10 points). For a HMM, the hidden states are {bull, bear}, the observation variables are {rise, fall}, the initial state probability distribution ais [0.5 0.5]", the transition probability distribution A is [0.4 0.7; 0.6 0.3], and the observation probability distribution B is [0.8 0.1;0.2 0.9]. If the observation sequence is {fall fall rise}, please show the computation procedure for estimating the most likely state sequence

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock