Homer Homes Pty Ltd (HH) is an Australian tax resident company and the head company of the

Question:

Homer Homes Pty Ltd (HH) is an Australian tax resident company and the head company of the HH income tax consolidated group. HH sells electronics and home appliances. HH also provides installation and repair services for goods sold to customers. HH has retail shops throughout Australia.

HH was founded by Ellie in 1974. Ellie was the sole shareholder until she sold the majority of her shareholding to a private equity firm in 2000. HH has had aggregated turnover exceeding $1 billion in the past two income years.

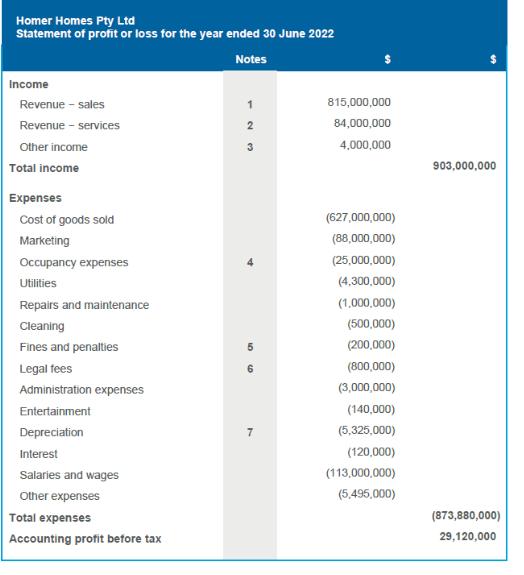

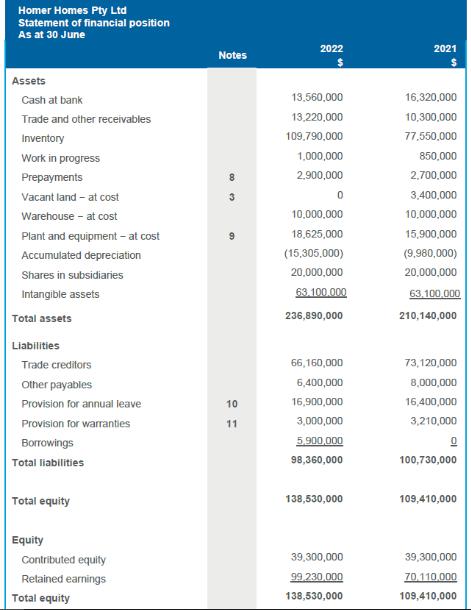

HH's Financial Accountant, Claire, has provided you with HH's standalone (before consolidation) draft financial statements for the income year ended 30 June 2022, which includes the following:

• Draft standalone statement of profit or loss.

• Draft standalone statement of financial position.

Claire has also provided additional notes to help you calculate HH's taxable income (which will ultimately be included in the taxable income of the HH income tax consolidated group) for the income year ended 30 June 2022.

Notes

1. HH donated stock with a cost of $125,000 to deductible gift recipient charities. The stock had a retail value of $155,000. No amount was recorded in revenue, although the cost was included in cost of goods sold. HH regularly donates stock to local charities.

2. On 30 June 2022, HH sold unbilled work-in-progress (WIP) for $63,000 to another repair business. The unbilled WIP related to repairs booked for July 2022. HH estimated it would have received $77,000 if it had completed the work. HH recorded the sold WIP of $63,000 in Revenue − services.

3. Other income includes:

(a) $1,700,000 cash dividend, unfranked, from Good Lyfe Pty Ltd (Good Lyfe), an Australian tax resident company. HH owns 100% of the shares in Good Lyfe.

(b) $1,200,000 cash dividend, franked to 75%, from East Meadow Pty Ltd (East Meadow), an Australian tax resident company. East Meadow has a corporate tax rate of 30% for imputation purposes for the income year ended 30 June 2022. HH has a 7% shareholding in East Meadow.

(c) $1,100,000 profit from the sale of vacant land. The land was purchased in 1982 for $3,400,000 for long-term investment purposes. It had a market value of $4,100,000 in 2000 when Ellie sold her HH shares to the private equity firm. The land was sold for $4,500,000. There were no transaction costs.

4. On 1 May 2022, HH terminated the lease of an underperforming store. It cost $3,300,000 to terminate the lease, which had three years left in the contract. This cost was included in Occupancy expenses.

5. HH paid the following amounts, which were recorded in Fines and penalties:

(a) $137,500 penalty for the late lodgement of its income tax return for the income year ended 30 June 2021.

(b) $62,500 in general interest charge on the late payment of tax.

6. On 1 July 2021, HH paid $52,000 in legal fees to conduct a legal due diligence on an Australian resident company that HH considered purchasing. HH did not proceed with the purchase. The $52,000 was recorded in Legal fees.

7. Based on HH's tax fixed asset register, HH's tax depreciation was $6,000,000.

8. During the income year ended 30 June 2022, HH made the following payments:

(a) On 27 June 2022, HH paid $240,000 of land tax relating to its warehouse in Victoria for the period 1 July 2022 to 30 June 2023. The payment was due in August 2022 and this was the first time HH prepaid its land tax obligations.

(b) On 1 June 2022, HH paid $880,000 of rent for its head office for the period 1 July 2022 to 30 June 2023. HH always prepays its next year's rent on 1 June. Its opening prepayment balance for rent was $810,000.

9. HH purchased $2,725,000 of new equipment for its warehouses and stores. Each item cost less than $50,000 and was used in the business immediately. For accounting purposes, the new equipment was recorded in HH's fixed asset register. As HH is still considering the depreciation rates to apply, no depreciation was recorded in the profit and loss. For tax purposes, the new equipment and the tax depreciation have not yet been included in HH's tax fixed asset register (see item 7). The maximum capital allowance deduction available based on applying the Commissioner's rates in TR 2021/3 was calculated by HH to be $850,000.

10. The provision for annual leave represents the amount of accrued expenditure for employees' annual leave entitlements that have not yet been taken by employees.

11. The provision for warranties represents HH's estimated costs to replace goods sold or redo repair work.

Task

For only the notes listed above (items 1−11), calculate HH's taxable income for the income year ended 30 June 2022 by preparing a reconciliation from accounting profit to taxable income and calculating the correct tax adjustment/s (even if the adjustment is nil).

For each adjustment (including nil adjustments) in items 1-11, provide the most relevant legislative reference.

Expert Answer:

To calculate Homer Homes Pty Ltds taxable income for the income year ended 30 June 2022 we need to make adjustments to the accounting profit provided in the financial statements Lets go through each o... View the full answer