Question: Homework 2 Handwriting is required! Please submit your scanned copy in PDF or WORD to Moodle by 23:59 March 28, 2024. The name of

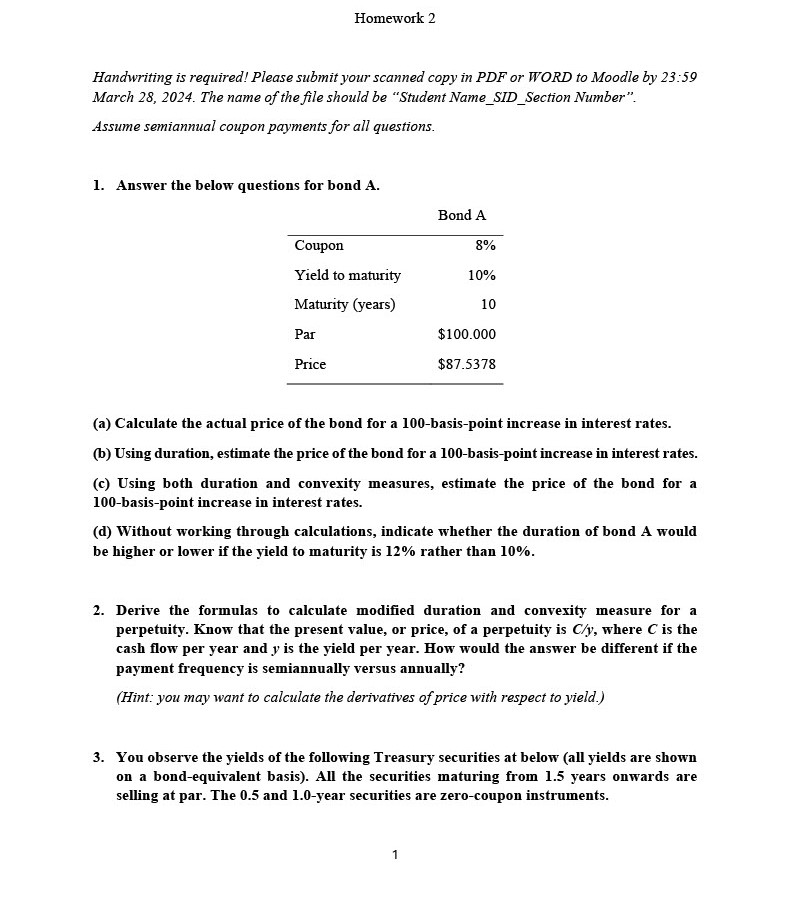

Homework 2 Handwriting is required! Please submit your scanned copy in PDF or WORD to Moodle by 23:59 March 28, 2024. The name of the file should be "Student Name_SID_Section Number". Assume semiannual coupon payments for all questions. 1. Answer the below questions for bond A. Bond A Coupon 8% Yield to maturity 10% Maturity (years) 10 Par $100.000 Price $87.5378 (a) Calculate the actual price of the bond for a 100-basis-point increase in interest rates. (b) Using duration, estimate the price of the bond for a 100-basis-point increase in interest rates. (c) Using both duration and convexity measures, estimate the price of the bond for a 100-basis-point increase in interest rates. (d) Without working through calculations, indicate whether the duration of bond A would be higher or lower if the yield to maturity is 12% rather than 10%. 2. Derive the formulas to calculate modified duration and convexity measure for a perpetuity. Know that the present value, or price, of a perpetuity is C/y, where C is the cash flow per year and y is the yield per year. How would the answer be different if the payment frequency is semiannually versus annually? (Hint: you may want to calculate the derivatives of price with respect to yield.) 3. You observe the yields of the following Treasury securities at below (all yields are shown on a bond-equivalent basis). All the securities maturing from 1.5 years onwards are selling at par. The 0.5 and 1.0-year securities are zero-coupon instruments. 1

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts