Question: Homework 8. Consider the one-step Binomial model. Let Pt for t = 0,1 be the price of a put option with strike K and maturity

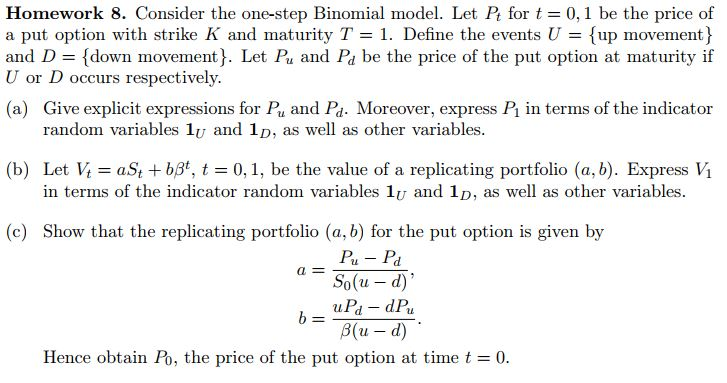

Homework 8. Consider the one-step Binomial model. Let Pt for t = 0,1 be the price of a put option with strike K and maturity T = 1. Define the events U = {up movement} and D = {down movement). Let Py and Pd be the price of the put option at maturity if U or D occurs respectively. (a) Give explicit expressions for P, and Pd. Moreover, express Pi in terms of the indicator random variables lu and 1p, as well as other variables. (b) Let V = aSt + b3*, t = 0,1, be the value of a replicating portfolio (a,b). Express Vi in terms of the indicator random variables ly and 1p, as well as other variables. a = (c) Show that the replicating portfolio (a,b) for the put option is given by Pu - Pa So(u-d) uPd - dP b= Blu-d) Hence obtain Po, the price of the put option at time t = 0. Homework 8. Consider the one-step Binomial model. Let Pt for t = 0,1 be the price of a put option with strike K and maturity T = 1. Define the events U = {up movement} and D = {down movement). Let Py and Pd be the price of the put option at maturity if U or D occurs respectively. (a) Give explicit expressions for P, and Pd. Moreover, express Pi in terms of the indicator random variables lu and 1p, as well as other variables. (b) Let V = aSt + b3*, t = 0,1, be the value of a replicating portfolio (a,b). Express Vi in terms of the indicator random variables ly and 1p, as well as other variables. a = (c) Show that the replicating portfolio (a,b) for the put option is given by Pu - Pa So(u-d) uPd - dP b= Blu-d) Hence obtain Po, the price of the put option at time t = 0

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts