Question: Homework: Assignment 10 Pricing bonds Part 2 Save Score: 0.25 of 1 pt 5 of 10 (10 complete) IW Score: 92.5%, 9... Problem 6-25 Question

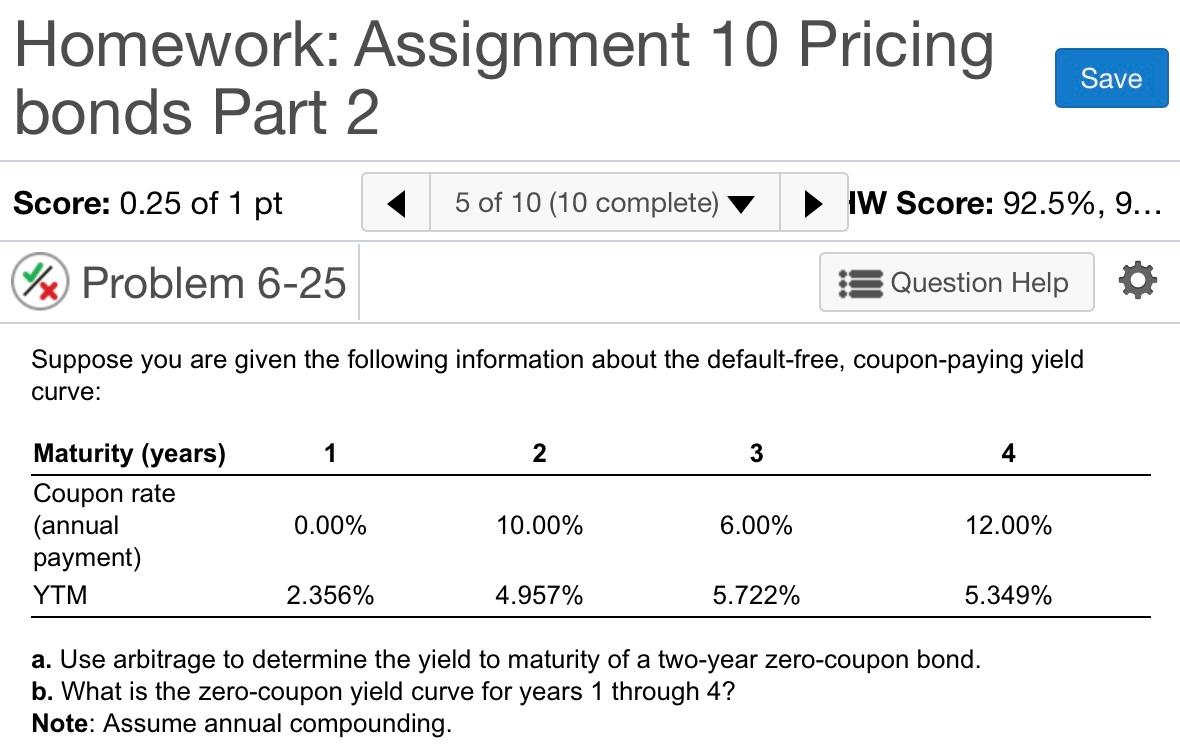

Homework: Assignment 10 Pricing bonds Part 2 Save Score: 0.25 of 1 pt 5 of 10 (10 complete) IW Score: 92.5%, 9... Problem 6-25 Question Help Suppose you are given the following information about the default-free, coupon-paying yield curve: 1 2 3 4 Maturity (years) Coupon rate (annual payment) YTM 0.00% 10.00% 6.00% 12.00% 2.356% 4.957% 5.722% 5.349% a. Use arbitrage to determine the yield to maturity of a two-year zero-coupon bond. b. What is the zero-coupon yield curve for years 1 through 4? Note: Assume annual compounding. Homework: Assignment 10 Pricing bonds Part 2 Save Score: 0.25 of 1 pt 5 of 10 (10 complete) IW Score: 92.5%, 9... Problem 6-25 Question Help Suppose you are given the following information about the default-free, coupon-paying yield curve: 1 2 3 4 Maturity (years) Coupon rate (annual payment) YTM 0.00% 10.00% 6.00% 12.00% 2.356% 4.957% 5.722% 5.349% a. Use arbitrage to determine the yield to maturity of a two-year zero-coupon bond. b. What is the zero-coupon yield curve for years 1 through 4? Note: Assume annual compounding

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts