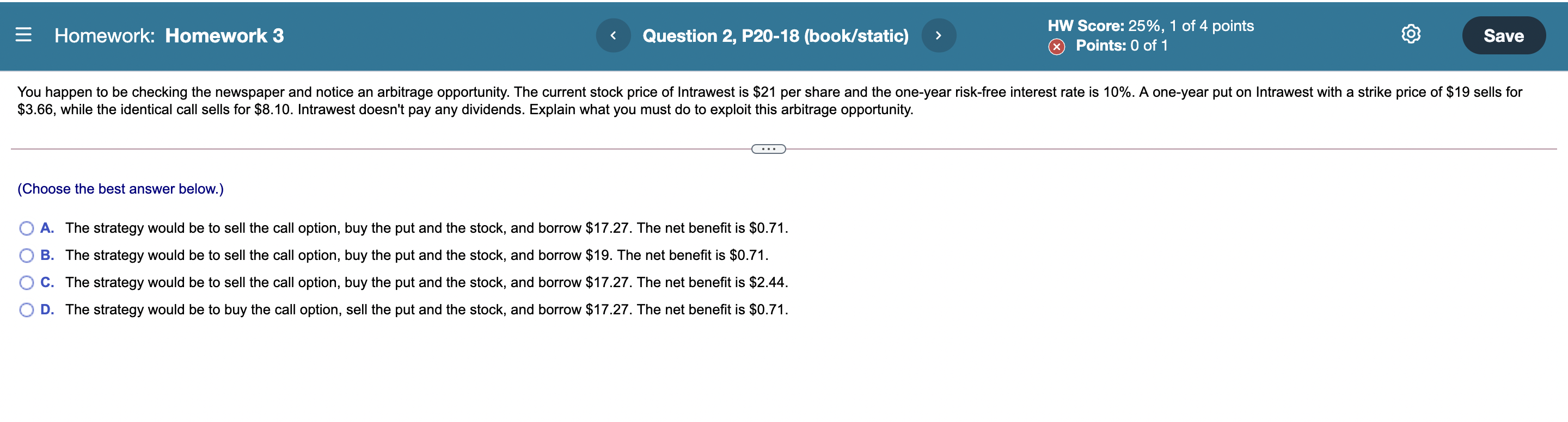

Question: = Homework: Homework 3 Question 2, P20-18 (book/static) HW Score: 25%, 1 of 4 points x Points: 0 of 1 Save You happen to be

= Homework: Homework 3 Question 2, P20-18 (book/static) HW Score: 25%, 1 of 4 points x Points: 0 of 1 Save You happen to be checking the newspaper and notice an arbitrage opportunity. The current stock price of Intrawest is $21 per share and the one-year risk-free interest rate is 10%. A one-year put on Intrawest with a strike price of $19 sells for $3.66, while the identical call sells for $8.10. Intrawest doesn't pay any dividends. Explain what you must do to exploit this arbitrage opportunity. (Choose the best answer below.) O A. The strategy would be to sell the call option, buy the put and the stock, and borrow $17.27. The net benefit is $0.71. B. The strategy would be to sell the call option, buy the put and the stock, and borrow $19. The net benefit is $0.71. C. The strategy would be to sell the call option, buy the put and the stock, and borrow $17.27. The net benefit is $2.44. D. The strategy would be to buy the call option, sell the put and the stock, and borrow $17.27. The net benefit is $0.71

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts