Question: How can I answer question 3b,3c,3d and 4b, 4c? 3. Bruce Willos is producing a new action movie featuring himself but the female star that

How can I answer question 3b,3c,3d and 4b, 4c?

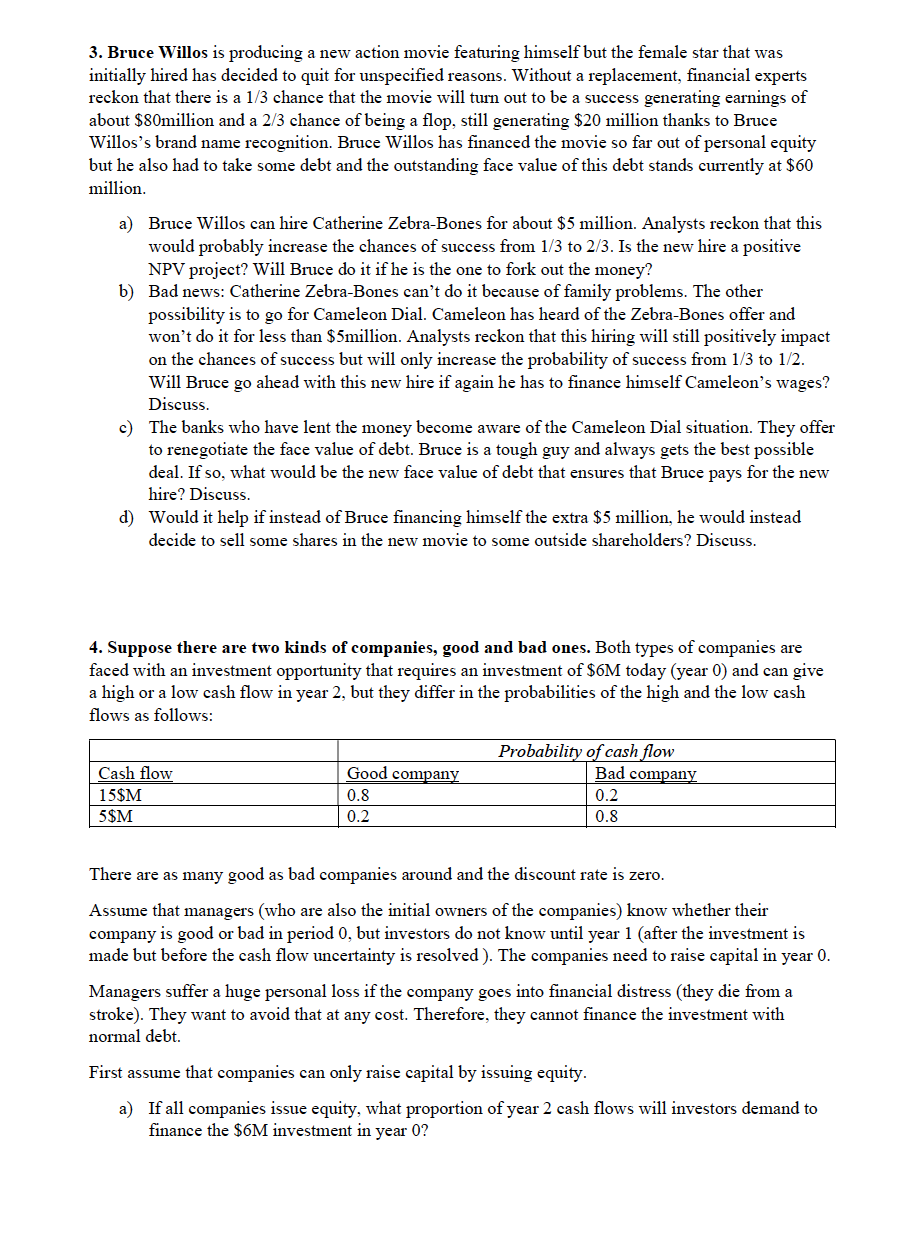

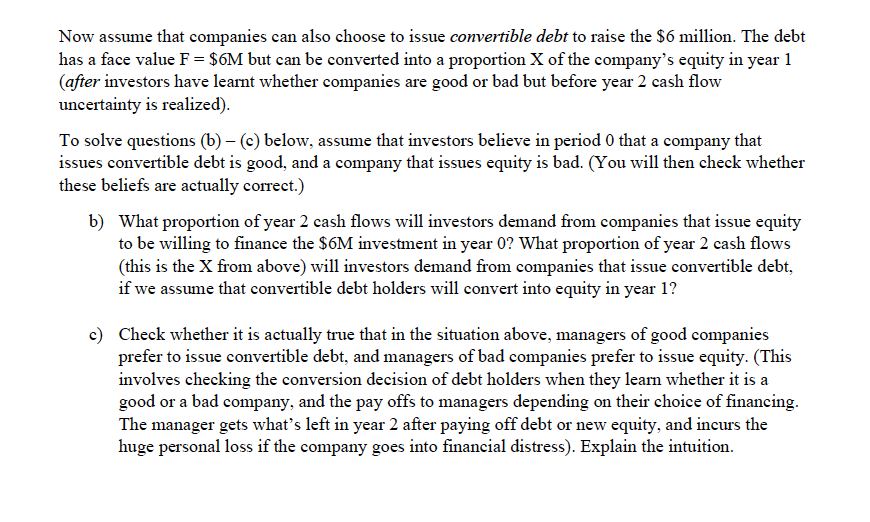

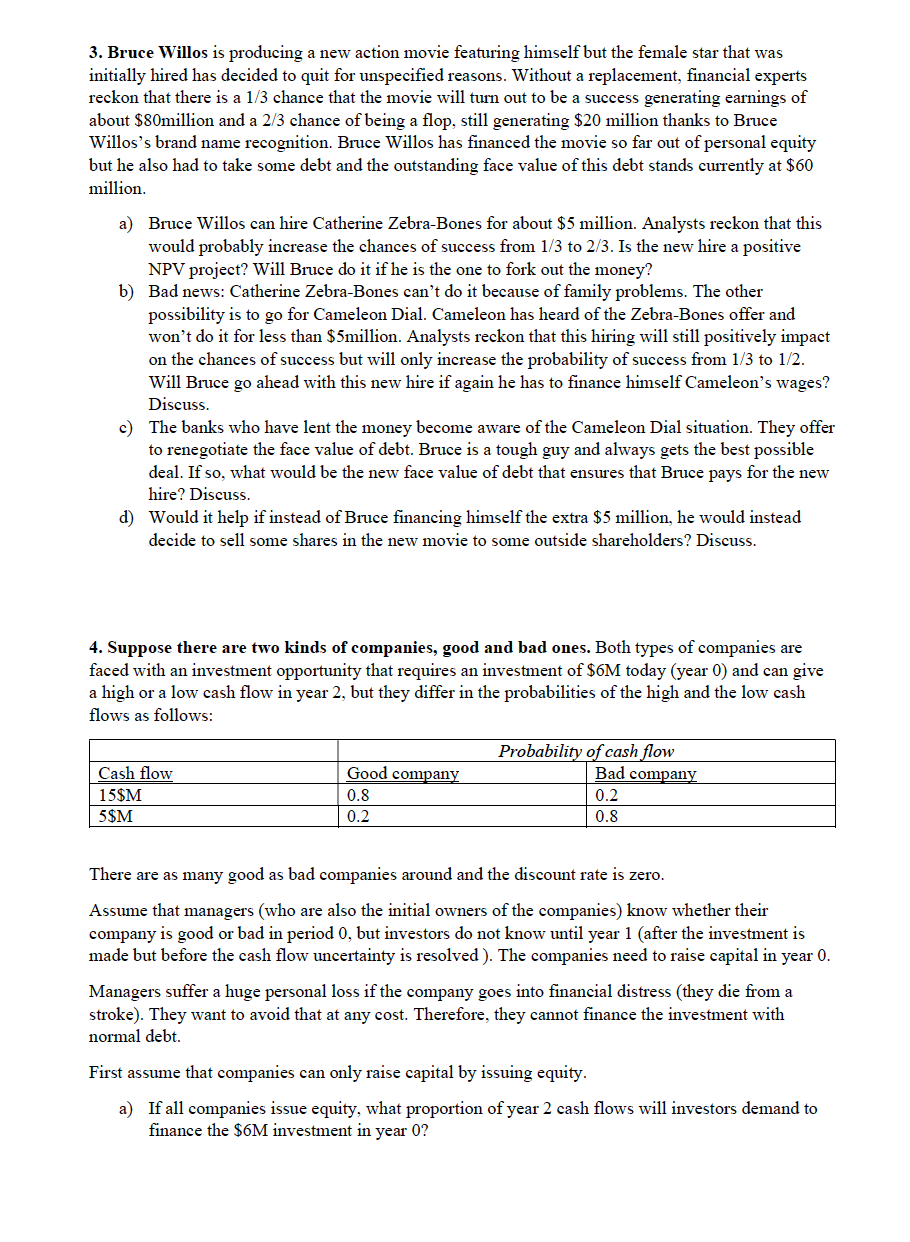

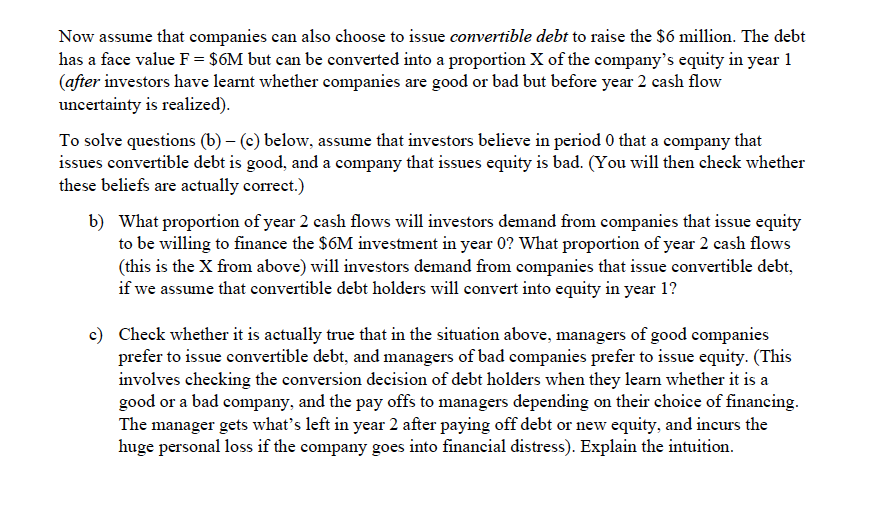

3. Bruce Willos is producing a new action movie featuring himself but the female star that was initially hired has decided to quit for unspecied reasons. Without a replacement, nancial experts reckon that there is a 113 chance that the movie will turn out to be a success generating earnings of about $80million and a 213 chance of being a op, still generating $20 million thanks to Bruce Willos's brand name recognition. Bruce Willos has nanced the movie so far out of personal equity but he also had to take some debt and the outstanding face value of this debt stands currently at $60 million. a) Bruce Willos can hire Catherine ZebraBones for about $5 million. Analysts reckon that this would probably increase the chances of success om US to 28. Is the new hire a positive NPV project? Will Bruce do it if he is the one to fork out the money? b) Bad news: Catherine ZebraBones can't do it because of family problems. The other possibility is to go for Cameleon Dial. Cameleon has heard of the ZebraBones oEer and won't do it for less than $5million. Analysts reckon that this hiring will still positively impact on the chances of success but will only increase the probability of success from US to 112. Will Bruce go ahead with this new hire if again he has to nance himself Cameleon's wages? Discuss. c) The banks who have lent the money become aware of the Cameleon Dial situation. They oa to renegotiate the face value of debt. Bruce is a tough guy and always gets the best possible deal. If so, what would be the new face value of debt that ensures that Bruce pays for the new hire? Discuss. d} Would it help if instead of Bruce nancing himselfthe extra $5 million, he would instead decide to sell some shares in the new movie to some outside shareholders? Discuss. 4. Suppose there are two kinds of companies, good and bad ones. Both types of companies are faced with an investment opportunity that requires an investment of $6M today (year 0) and can give a high or a low cash ow in year 2, but they differ in the probabilities of the high and the low cash ows as follows: Probability ofcashaw Cash ow Good cgpany Bad company 1 5$M 0.3 0 .2 5$M 0.2 0.8 There are as many good as bad companies around and the discount rate is zero. Assume that managers (who are also the initial owners of the companies) know whether their company is good or bad in period 0, but investors do not know until year 1 (after the investment is made but before the cash ow uncertainty is resolved ). The companies need to raise capital in year 0. Managers suer a huge personal loss if the company goes into nancial distress (they die from a stroke). They want to avoid that at any cost. Therefore, they cannot nance the investment with normal debt. First assume that companies can only raise capital by issuing equity. a) Ifall companies issue equity, what proportion of year 2 cash flows will investors demand to nance the $6M investment in year 0? Now assume that companies can also choose to issue convertible debt to raise the $6 million. The debt has a face value F = $m but can be converted into a proportion X of the company's equity in year 1 (aer investors have learnt whether companies are good or bad but before year 2 cash ow uncertainty is realized}. To solve questions (b) (c) below, assume that investors believe in period 0 that a company that issues convertible debt is good, and a company that issues equity is bad. (You will then check whether these beliefs are actually correct.) b) What proportion of year 2 cash ows will investors demand from companies that issue equity to be willing to nance the $6M investment inyear 0? What proportion of year 2 cash flows (this is the X from above) will investors demand from companies that issue convertible debt, if we assume that convertible debt holders will convert into equity in year 1? c} Check whether it is actually true that in the situation above, managers of good companies prefer to issue convertible debt, and managers of bad companies prefer to issue equity. (This involves checking the conversion decision of debt holders when they learn whether it is a good or a bad company, and the pay offs to managers depending on their choice of nancing. The manager gets what's le in year 2 aer paying off debt or new equity, and incurs the huge personal loss if the company goes into nancial distress). Explain the intuition

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts