Question: How do I approach this? Question 10 Incorrect Mark 0.00 out of 1.00 P Flag question Qantas wants to hedge a USD 100 million payable

How do I approach this?

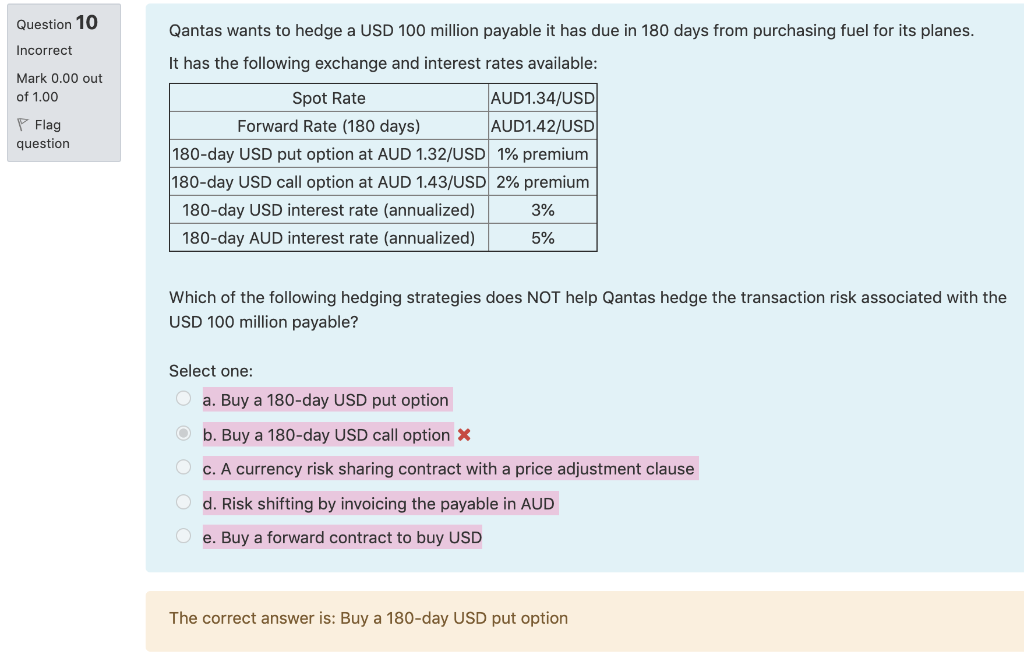

Question 10 Incorrect Mark 0.00 out of 1.00 P Flag question Qantas wants to hedge a USD 100 million payable it has due in 180 days from purchasing fuel for its planes. It has the following exchange and interest rates available: Spot Rate AUD1.34/USD Forward Rate (180 days) AUD1.42/USD 180-day USD put option at AUD 1.32/USD 1% premium 180-day USD call option at AUD 1.43/USD 2% premium 180-day USD interest rate (annualized) 3% 180-day AUD interest rate (annualized) 5% Which of the following hedging strategies does NOT help Qantas hedge the transaction risk associated with the USD 100 million payable? Select one: a. Buy a 180-day USD put option Ob. Buy a 180-day USD call option X c. A currency risk sharing contract with a price adjustment clause O d. Risk shifting by invoicing the payable in AUD O e. Buy a forward contract to buy USD The correct answer is: Buy a 180-day USD put option

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts