Question: How do I approach this question? L is the loss-at-issue random variable for a fully continuous n-year term insurance of 1 on the life of

How do I approach this question?

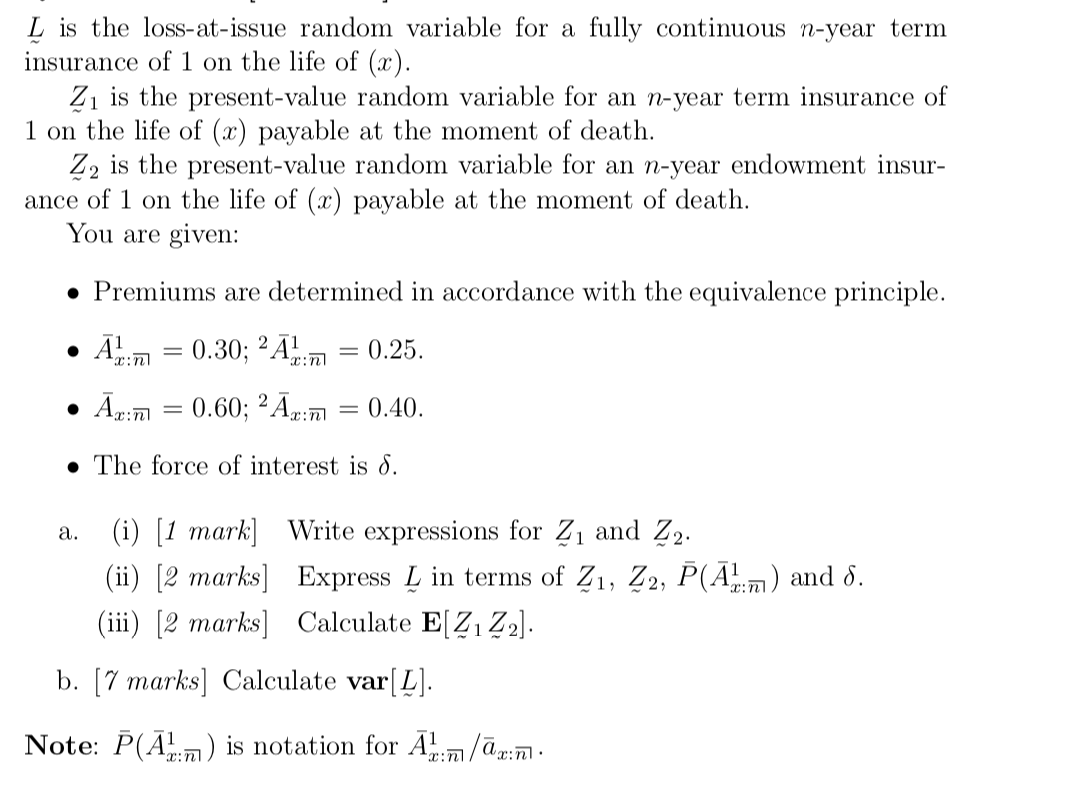

L is the loss-at-issue random variable for a fully continuous n-year term insurance of 1 on the life of (x). Z1 is the present-value random variable for an n-year term insurance of 1 on the life of (x) payable at the moment of death. Z2 is the present-value random variable for an n-year endowment insur- ance of 1 on the life of (x) payable at the moment of death. You are given: . Premiums are determined in accordance with the equivalence principle. . Am = 0.30; 2A = 0.25. . At:ml = 0.60; 2 Ax:m = 0.40. . The force of interest is 6. a. (i) [1 mark] Write expressions for Z1 and Z2. (ii) [2 marks] Express L in terms of Z1, Z2, P(A! ) and 6. (iii) [2 marks] Calculate E[Z , Z2]. b. [7 marks] Calculate var [ L]. Note: P(A) ) is notation for A

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts