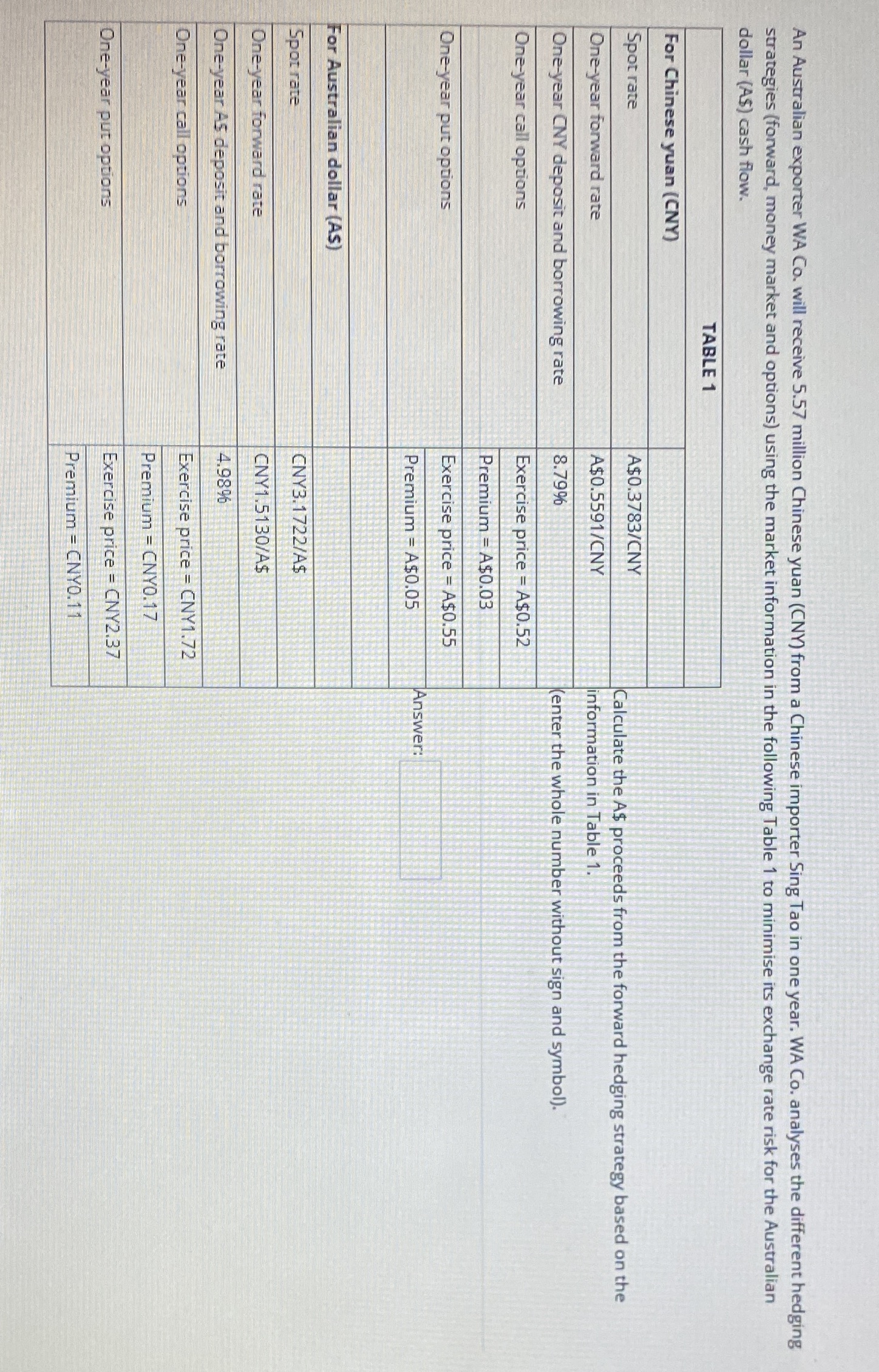

Question: How do I calculate the minimum A$ proceeds for the options hedging strategy based on the market information in Table 1?? An Australian exporter WA

How do I calculate the minimum A$ proceeds for the options hedging strategy based on the market information in Table 1??

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock