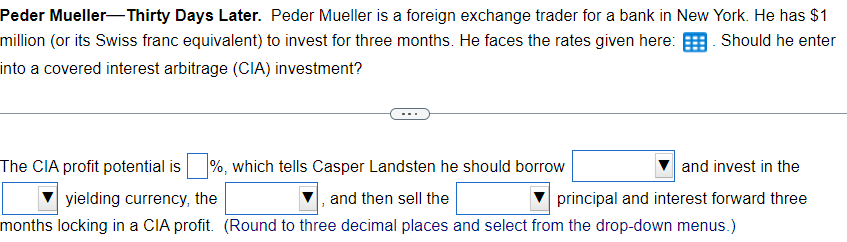

Question: How do I do this? (Data at the bottom) Arbitrage funds available (USD) 1,000,000 Spot exchange rate (CHF=USD1.00) 1.3391 3-month forward rate (CHF=USD1.00) 1.3287 U.S.

How do I do this? (Data at the bottom)

Arbitrage funds available (USD) 1,000,000 Spot exchange rate (CHF=USD1.00) 1.3391 3-month forward rate (CHF=USD1.00) 1.3287 U.S. dollar 3-month interest rate (%) 4.748 Swiss franc 3-month interest rate (%) 3.623

Peder Mueller-Thirty Days Later. Peder Mueller is a foreign exchange trader for a bank in New York. He has $1 million (or its Swiss franc equivalent) to invest for three months. He faces the rates given here: Should he enter into a covered interest arbitrage (CIA) investment? The CIA profit potential is \%, which tells Casper Landsten he should borrow and invest in the yielding currency, the and then sell the principal and interest forward three months locking in a CIA profit. (Round to three decimal places and select from the drop-down menus.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts