Question: How do I solve part A. 23. (40 points) You have run a couple of regressions using 5 years of data (the appropriate val- ues

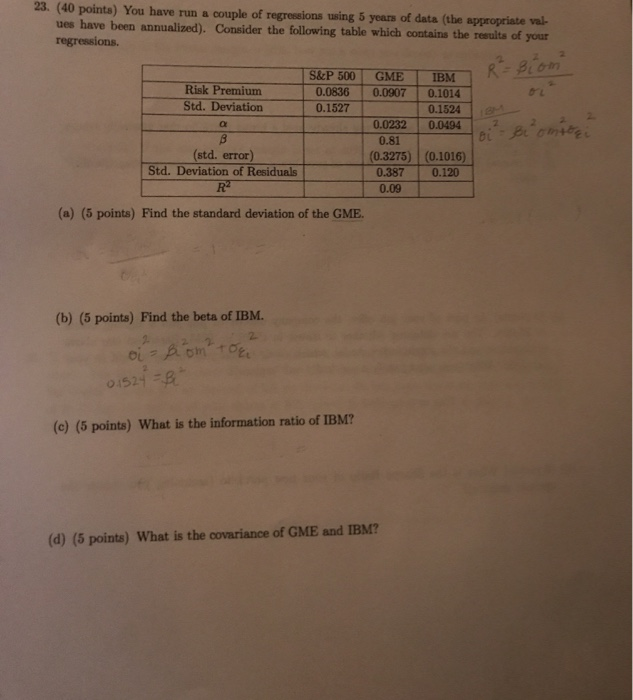

23. (40 points) You have run a couple of regressions using 5 years of data (the appropriate val- ues have been annualized). Consider the following table which contains the results of your regressions. R Biom S&P 500 GME IBM Risk Premium Std. Deviation 0.0836 0.0907 0.1014 0.1527 0.1524 0.0232 0.0494 Biomiogi 0.81 (0.3275) (0.1016) (std. error) Std. Deviation of Residuals 0.387 0.120 0.09 (a) (5 points) Find the standard deviation of the GME. (b) (5 points) Find the beta of IBM. 01524 -B (c) (5 points) What is the information ratio of IBM? (d) (5 points) What is the covariance of GME and IBM? 23. (40 points) You have run a couple of regressions using 5 years of data (the appropriate val- ues have been annualized). Consider the following table which contains the results of your regressions. R Biom S&P 500 GME IBM Risk Premium Std. Deviation 0.0836 0.0907 0.1014 0.1527 0.1524 0.0232 0.0494 Biomiogi 0.81 (0.3275) (0.1016) (std. error) Std. Deviation of Residuals 0.387 0.120 0.09 (a) (5 points) Find the standard deviation of the GME. (b) (5 points) Find the beta of IBM. 01524 -B (c) (5 points) What is the information ratio of IBM? (d) (5 points) What is the covariance of GME and IBM

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts