Question: How do you get thisanswer? Portfolio Weight 0.25 Correlation w Market Portfolio 0.7 0.6 0.5 Volatility 14% 18% 15% Firm Taggart Transcontinental Wyatt Oi 0.35

How do you get thisanswer?

How do you get thisanswer?

Portfolio Weight 0.25 Correlation w Market Portfolio 0.7 0.6 0.5 Volatility 14% 18% 15% Firm Taggart Transcontinental Wyatt Oi 0.35 0.40 Rearden Metal The volatility of the market portfolio is 10%, the expected return on the market is 12%, and the risk-free rate of interest is 4% The Sharpe Ratio for the market portfolio is closest to O A. 0.40 O B. 0.56 O C. 0.48 D. 0.80

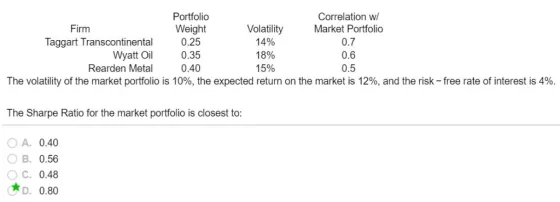

Portfolio Firm Weight Volatility Correlation w/ Market Portfolio Taggart Transcontinental 0.25 14% 0.7 Wyatt Oil 0.35 18% 0.6 Rearden Metal 0.40 15% 0.5 The volatility of the market portfolio is 10%, the expected return on the market is 12%, and the risk-free rate of interest is 4%. The Sharpe Ratio for the market portfolio is closest to: A. 0.40 B. 0.56 C. 0.48 D. 0.80

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock