Question: How do you solve question a? Consider an economy with two assets and two states of the world such that the matrix of payoffs of

How do you solve question a?

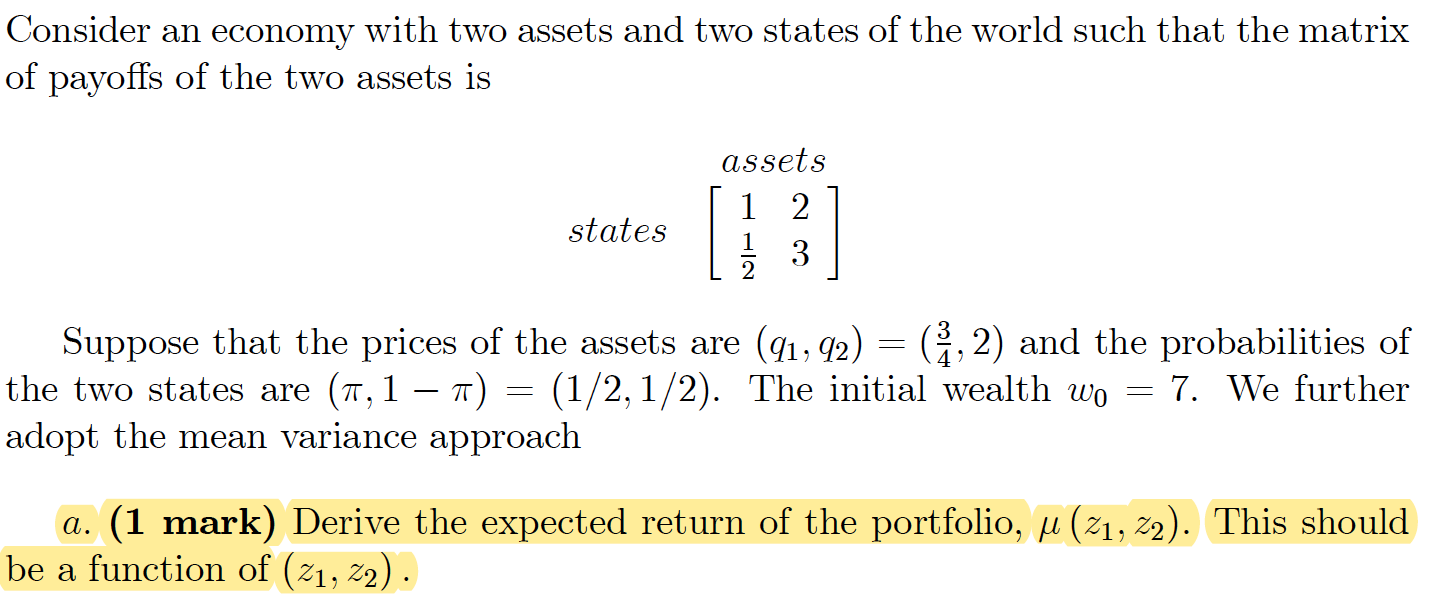

Consider an economy with two assets and two states of the world such that the matrix of payoffs of the two assets is assets states [ 1 2 ] 5 3 Suppose that the prices of the assets are (ql, (12) : (g, 2) and the probabilities of the two states are (7r, 1 7T) : (1/2,1/2). The initial wealth wo : 7. We further adopt the mean variance approach a. (1 mark) Derive the expected return of the portfolio, In (Z1, 22). This should be a function of (21, 22)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock