Question: How does debt affect CPK? To answer this question, you have to calculate the variables listed under Exhibit 9 of the Excel file (those that

How does debt affect CPK? To answer this question, you have to calculate the variables listed under Exhibit 9 of the Excel file (those that I have shaded yellow) when CPK is unlevered, and is levered at 10%, 20%, and 30%. After calculating these variables, analyze how debt affects CPK.

Calculate 1. Return on equity 2. Price per share 3. Shares repurchased

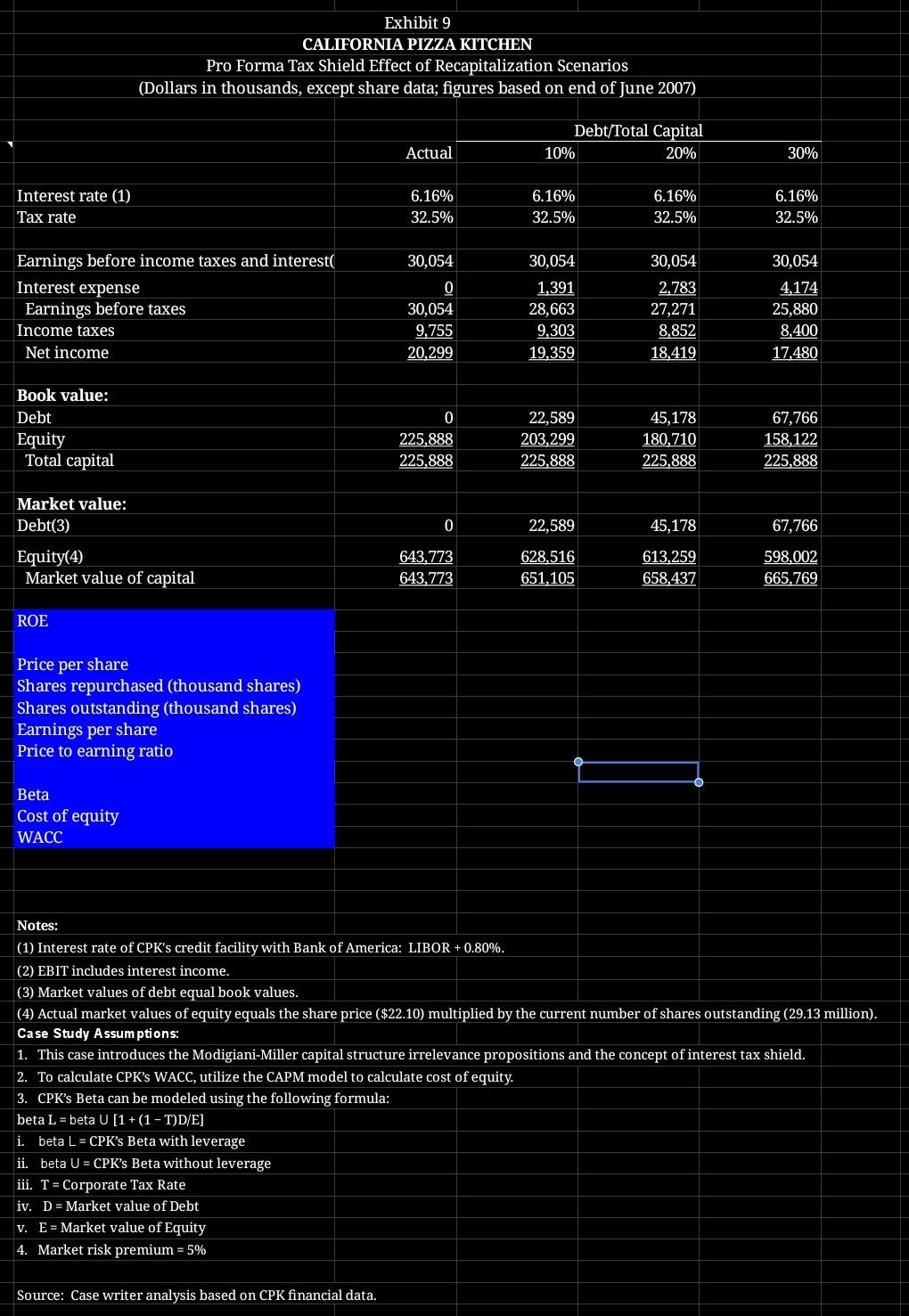

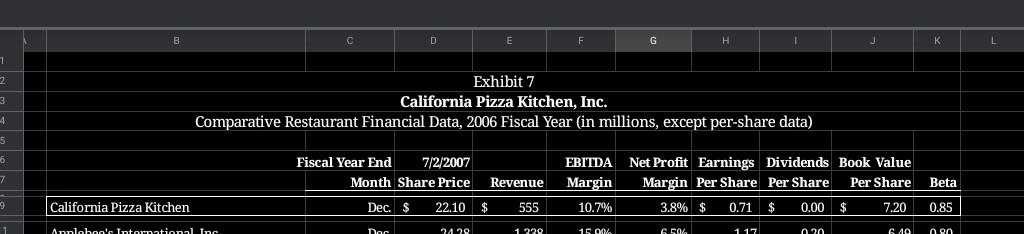

Exhibit 9 CALIFORNIA PIZZA KITCHEN Pro Forma Tax Shield Effect of Recapitalization Scenarios (Dollars in thousands, except share data; figures based on end of June 2007) Debt/Total Capital 10% 20% Actual 30% Interest rate (1) Tax rate 6.16% 32.5% 6.16% 32.5% 6.16% 32.5% 6.16% 32.5% 30,054 30,054 30,054 30,054 Earnings before income taxes and interest Interest expense Earnings before taxes Income taxes Net income 0 30,054 9,755 20,299 1,391 28,663 9,303 19,359 2,783 27,271 8,852 18,419 4,174 25,880 8,400 17,480 Book value: Debt Equity Total capital 0 225,888 225,888 22,589 203,299 225,888 45,178 180,710 225,888 67,766 158,122 225,888 Market value: Debt(3) 0 22,589 45,178 67,766 Equity(4) Market value of capital 643,773 643,773 628,516 651,105 613,259 658,437 598.002 665,769 ROE Price per share Shares repurchased (thousand shares) Shares outstanding (thousand shares) Earnings per share Price to earning ratio Beta Cost of equity WACC Notes: (1) Interest rate of CPK's credit facility with Bank of America: LIBOR + 0.80%. (2) EBIT includes interest income. (3) Market values of debt equal book values. (4) Actual market values of equity equals the share price ($22.10) multiplied by the current number of shares outstanding (29.13 million). Case Study Assumptions: 1. This case introduces the Modigiani-Miller capital structure irrelevance propositions and the concept of interest tax shield. 2. To calculate CPK's WACC, utilize the CAPM model to calculate cost of equity. 3. CPK's Beta can be modeled using the following formula: beta L = beta U (1 + (1 - T)D/E] i. beta L = CPK's Beta with leverage ii. beta U = CPK's Beta without leverage iii. T = Corporate Tax Rate iv. D = Market value of Debt v. E = Market value of Equity 4. Market risk premium = 5% Source: Case writer analysis based on CPK financial data. D G 1 2 3 4 5 6 7 Exhibit 7 California Pizza Kitchen, Inc. Comparative Restaurant Financial Data, 2006 Fiscal Year (in millions, except per-share data) Fiscal Year End 7/2/2007 Month Share Price Revenue EBITDA Net Profit Earnings Dividends Book Value Margin Margin Per Share Per Share Per Share 10.7% 3.8% $ 0.71 $ 0.00 $ 7.20 Beta 9 California Pizza Kitchen Dec. $ 22.10 555 0.85 Apoloboo's International Inc Doc 2429 1 229 15 00 6 50% 1 17 20 64 no Exhibit 9 CALIFORNIA PIZZA KITCHEN Pro Forma Tax Shield Effect of Recapitalization Scenarios (Dollars in thousands, except share data; figures based on end of June 2007) Debt/Total Capital 10% 20% Actual 30% Interest rate (1) Tax rate 6.16% 32.5% 6.16% 32.5% 6.16% 32.5% 6.16% 32.5% 30,054 30,054 30,054 30,054 Earnings before income taxes and interest Interest expense Earnings before taxes Income taxes Net income 0 30,054 9,755 20,299 1,391 28,663 9,303 19,359 2,783 27,271 8,852 18,419 4,174 25,880 8,400 17,480 Book value: Debt Equity Total capital 0 225,888 225,888 22,589 203,299 225,888 45,178 180,710 225,888 67,766 158,122 225,888 Market value: Debt(3) 0 22,589 45,178 67,766 Equity(4) Market value of capital 643,773 643,773 628,516 651,105 613,259 658,437 598.002 665,769 ROE Price per share Shares repurchased (thousand shares) Shares outstanding (thousand shares) Earnings per share Price to earning ratio Beta Cost of equity WACC Notes: (1) Interest rate of CPK's credit facility with Bank of America: LIBOR + 0.80%. (2) EBIT includes interest income. (3) Market values of debt equal book values. (4) Actual market values of equity equals the share price ($22.10) multiplied by the current number of shares outstanding (29.13 million). Case Study Assumptions: 1. This case introduces the Modigiani-Miller capital structure irrelevance propositions and the concept of interest tax shield. 2. To calculate CPK's WACC, utilize the CAPM model to calculate cost of equity. 3. CPK's Beta can be modeled using the following formula: beta L = beta U (1 + (1 - T)D/E] i. beta L = CPK's Beta with leverage ii. beta U = CPK's Beta without leverage iii. T = Corporate Tax Rate iv. D = Market value of Debt v. E = Market value of Equity 4. Market risk premium = 5% Source: Case writer analysis based on CPK financial data. D G 1 2 3 4 5 6 7 Exhibit 7 California Pizza Kitchen, Inc. Comparative Restaurant Financial Data, 2006 Fiscal Year (in millions, except per-share data) Fiscal Year End 7/2/2007 Month Share Price Revenue EBITDA Net Profit Earnings Dividends Book Value Margin Margin Per Share Per Share Per Share 10.7% 3.8% $ 0.71 $ 0.00 $ 7.20 Beta 9 California Pizza Kitchen Dec. $ 22.10 555 0.85 Apoloboo's International Inc Doc 2429 1 229 15 00 6 50% 1 17 20 64 no

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts