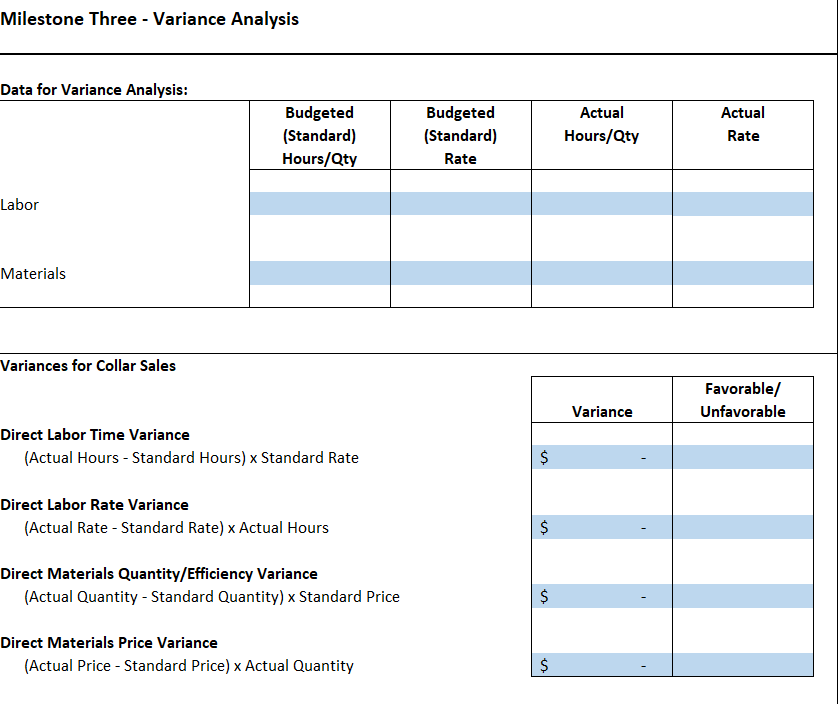

Question: How is this solved for or computed especially for the Budgeted/Standard Hours or Quantity and Budgeted/Standard Rate? One collar maker, who will be paid $16.00

How is this solved for or computed especially for the Budgeted/Standard Hours or Quantity and Budgeted/Standard Rate?

- One collar maker, who will be paid $16.00 per hour and work 40 hours per week

- One leash maker, who will be paid $16.00 per hour and work 40 hours per week

- One harness maker, who will be paid $17.00 per hour and work 40 hours per week

- One receptionist, who will be paid $15.00 per hour and work 30 hours per week

At the end of the month, you find that the labor and materials spent on manufacturing collars was different from what you estimated:

- The collar maker had to work nine hours a day instead of eight due to an increased demand for collars.

- Because of the increased demand, the hourly rate you paid your employee for making the collars increased to $16.50.

- An increase in the cost of raw material led the direct material cost per collar to increase to $10.

- However, you also made and sold 60 more collars than you expected to sell in the month.

You now need to determine the variance in the materials and labor cost from what you estimated in Milestone Two based on the market research data.

Contribution Margin for Collars = $18.9 Contribution Margin for Leashes = $17.9 Contribution Margin for Harnesses = $20.4

Fixed Costs for Collars = $4028 Fixed Costs for Leashes = $4028 Fixed Costs for Harnesses = $4202

Sales Price per unit Collar = $28 Sales Price per unit Leash = $30 Sales Price per unit Harness = $35

Milestone Three - Variance Analysis Data for Variance Analysis: Budgeted (Standard) Hours/Qty Budgeted (Standard) Rate Actual Hours/Qty Actual Rate Labor Materials Variances for Collar Sales Favorable/ Unfavorable Variance Direct Labor Time Variance (Actual Hours - Standard Hours) x Standard Rate $ Direct Labor Rate Variance (Actual Rate - Standard Rate) Actual Hours $ Direct Materials Quantity/Efficiency Variance (Actual Quantity - Standard Quantity) x Standard Price $ Direct Materials Price Variance (Actual Price - Standard Price) Actual Quantity $ $ Milestone Three - Variance Analysis Data for Variance Analysis: Budgeted (Standard) Hours/Qty Budgeted (Standard) Rate Actual Hours/Qty Actual Rate Labor Materials Variances for Collar Sales Favorable/ Unfavorable Variance Direct Labor Time Variance (Actual Hours - Standard Hours) x Standard Rate $ Direct Labor Rate Variance (Actual Rate - Standard Rate) Actual Hours $ Direct Materials Quantity/Efficiency Variance (Actual Quantity - Standard Quantity) x Standard Price $ Direct Materials Price Variance (Actual Price - Standard Price) Actual Quantity $ $

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts