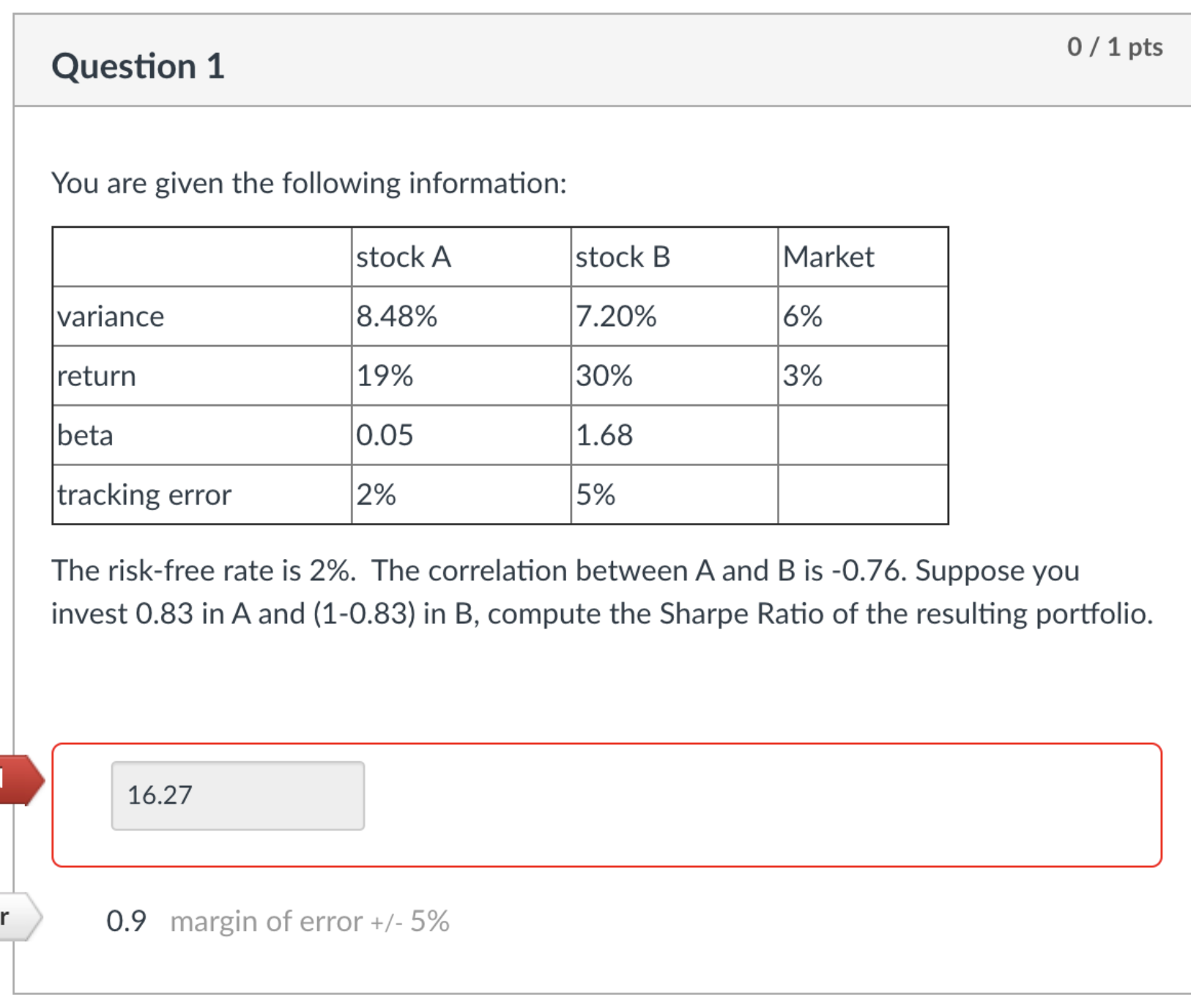

Question: How to calculate this problem? 0/1Dts Question 1 You are given the following information: - - - The risk-free rate is 2%. The correlation between

How to calculate this problem?

0/1Dts Question 1 You are given the following information: - - - The risk-free rate is 2%. The correlation between A and B is -0.76. Suppose you invest 0.83 in A and (1-0.83) in B, compute the Sharpe Ratio of the resulting portfolio. r i 0.9 margin of error +/ 5%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock