Question: How to calculate this problem? Question 4 1 / 1 pts You have the following information: stock A stock B risk-free return 3% 13% 3%

How to calculate this problem?

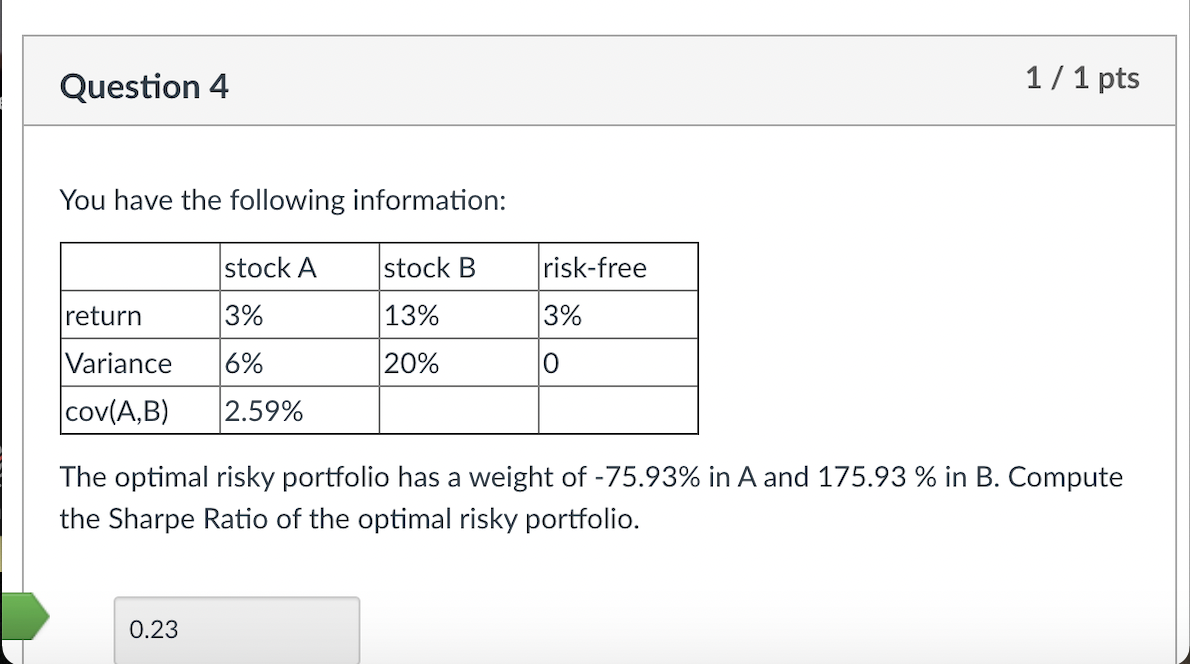

Question 4 1 / 1 pts You have the following information: stock A stock B risk-free return 3% 13% 3% Variance 6% 20% O cov(A,B) 2.59% The optimal risky portfolio has a weight of -75.93% in A and 175.93 % in B. Compute the Sharpe Ratio of the optimal risky portfolio. 0.23

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock