Question: How to complete a general journal, worksheet, income statement, changed in owners equity and balance sheet 01. 02. 03. 04. 05. 06. 07. June 1:

How to complete a general journal, worksheet, income statement, changed in owners equity and balance sheet

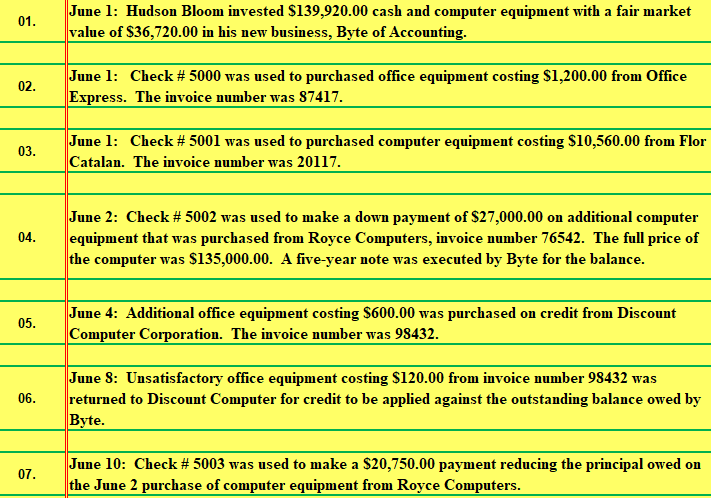

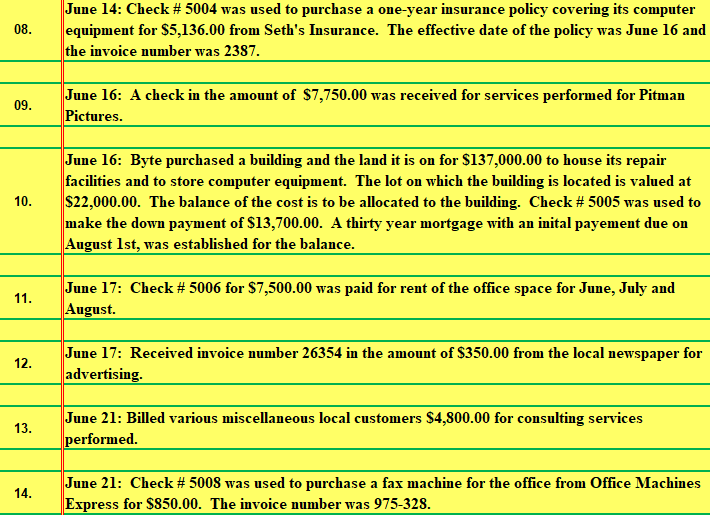

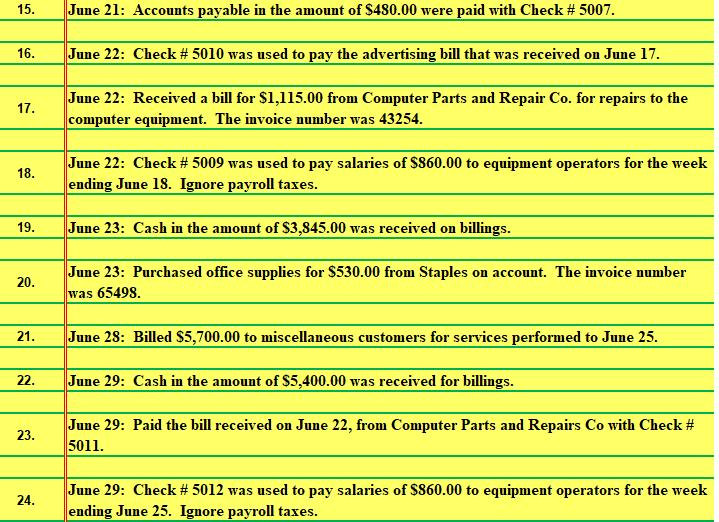

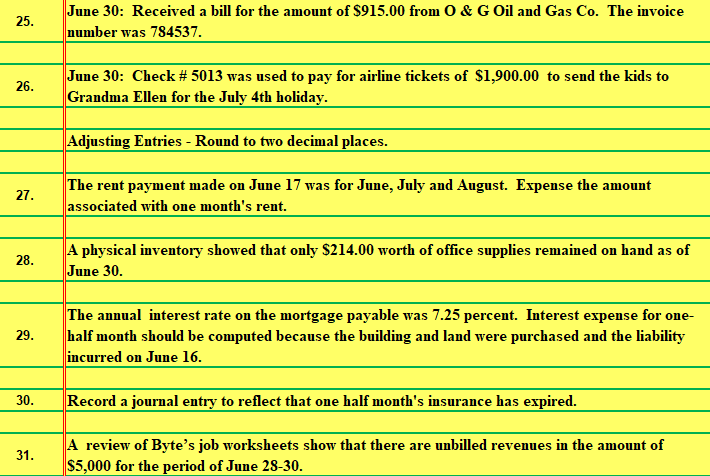

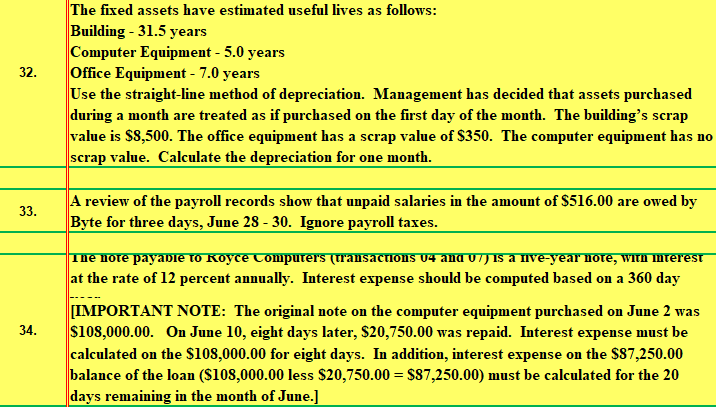

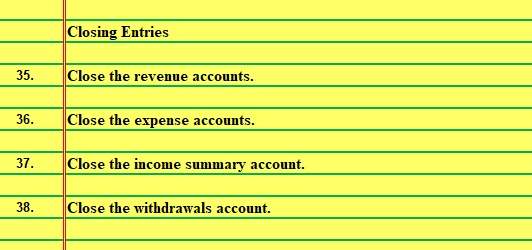

01. 02. 03. 04. 05. 06. 07. June 1: Hudson Bloom invested $139,920.00 cash and computer equipment with a fair market value of $36,720.00 in his new business, Byte of Accounting. June 1: Check # 5000 was used to purchased office equipment costing $1,200.00 from Office Express. The invoice number was 87417. June 1: Check # 5001 was used to purchased computer equipment costing $10,560.00 from Flor Catalan. The invoice number was 20117. June 2: Check # 5002 was used to make a down payment of $27,000.00 on additional computer equipment that was purchased from Royce Computers, invoice number 76542. The full price of the computer was $135,000.00. A five-year note was executed by Byte for the balance. June 4: Additional office equipment costing $600.00 was purchased on credit from Discount Computer Corporation. The invoice number was 98432. June 8: Unsatisfactory office equipment costing $120.00 from invoice number 98432 was returned to Discount Computer for credit to be applied against the outstanding balance owed by Byte. June 10: Check # 5003 was used to make a $20,750.00 payment reducing the principal owed on the June 2 purchase of computer equipment from Royce Computers. 08. 09. 10. 11. 12. 13. 14. June 14: Check # 5004 was used to purchase a one-year insurance policy covering its computer equipment for $5,136.00 from Seth's Insurance. The effective date of the policy was June 16 and the invoice number was 2387. June 16: A check in the amount of $7,750.00 was received for services performed for Pitman Pictures. June 16: Byte purchased a building and the land it is on for $137,000.00 to house its repair facilities and to store computer equipment. The lot on which the building is located is valued at $22,000.00. The balance of the cost is to be allocated to the building. Check # 5005 was used to make the down payment of $13,700.00. A thirty year mortgage with an inital payement due on August 1st, was established for the balance. June 17: Check # 5006 for $7,500.00 was paid for rent of the office space for June, July and August. June 17: Received invoice number 26354 in the amount of $350.00 from the local newspaper for advertising. June 21: Billed various miscellaneous local customers $4,800.00 for consulting services performed. June 21: Check # 5008 was used to purchase a fax machine for the office from Office Machines Express for $850.00. The invoice number was 975-328. 15. 16. 17. 18. 19. 20. 21. 22. 23. 24. June 21: Accounts payable in the amount of $480.00 were paid with Check # 5007. June 22: Check # 5010 was used to pay the advertising bill that was received on June 17. June 22: Received a bill for $1,115.00 from Computer Parts and Repair Co. for repairs to the computer equipment. The invoice number was 43254. June 22: Check # 5009 was used to pay salaries of $860.00 to equipment operators for the week ending June 18. Ignore payroll taxes. June 23: Cash in the amount of $3,845.00 was received on billings. June 23: Purchased office supplies for $530.00 from Staples on account. The invoice number was 65498. June 28: Billed $5,700.00 to miscellaneous customers for services performed to June 25. June 29: Cash in the amount of $5,400.00 was received for billings. June 29: Paid the bill received on June 22, from Computer Parts and Repairs Co with Check # 5011. June 29: Check # 5012 was used to pay salaries of $860.00 to equipment operators for the week ending June 25. Ignore payroll taxes. 25. 26. 27. 28. 29. 30. 31. June 30: Received a bill for the amount of $915.00 from O & G Oil and Gas Co. The invoice number was 784537. June 30: Check # 5013 was used to pay for airline tickets of $1,900.00 to send the kids to Grandma Ellen for the July 4th holiday. Adjusting Entries - Round to two decimal places. The rent payment made on June 17 was for June, July and August. Expense the amount associated with one month's rent. A physical inventory showed that only $214.00 worth of office supplies remained on hand as of June 30. The annual interest rate on the mortgage payable was 7.25 percent. Interest expense for one- half month should be computed because the building and land were purchased and the liability incurred on June 16. Record a journal entry to reflect that one half month's insurance has expired. A review of Byte's job worksheets show that there are unbilled revenues in the amount of $5,000 for the period of June 28-30. 32. 33. 34. The fixed assets have estimated useful lives as follows: Building - 31.5 years Computer Equipment - 5.0 years Office Equipment - 7.0 years Use the straight-line method of depreciation. Management has decided that assets purchased during a month are treated as if purchased on the first day of the month. The building's scrap value is $8,500. The office equipment has a scrap value of $350. The computer equipment has no scrap value. Calculate the depreciation for one month. A review of the payroll records show that unpaid salaries in the amount of $516.00 are owed by Byte for three days, June 28 - 30. Ignore payroll taxes. Ine note payable to Koyce Computers (transactions 04 and 07) is a nive-year note, with interest at the rate of 12 percent annually. Interest expense should be computed based on a 360 day [IMPORTANT NOTE: The original note on the computer equipment purchased on June 2 was $108,000.00. On June 10, eight days later, $20,750.00 was repaid. Interest expense must be calculated on the $108,000.00 for eight days. In addition, interest expense on the $87,250.00 balance of the loan ($108,000.00 less $20,750.00 = $87,250.00) must be calculated for the 20 days remaining in the month of June.] 35. 36. 37. 38. Closing Entries Close the revenue accounts. Close the expense accounts. Close the income summary account. Close the withdrawals account

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts