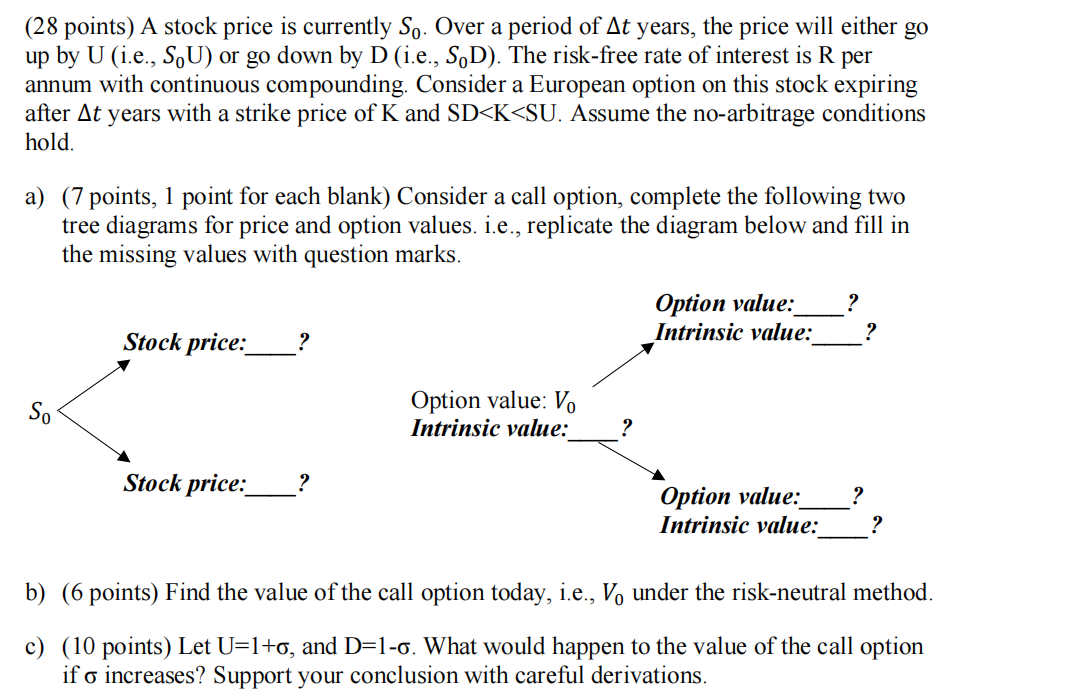

Question: How to derive question C from formula perspective rather than numerical value example? (28 points) A stock price is currently S0. Over a period of

How to derive question C from formula perspective rather than numerical value example?

How to derive question C from formula perspective rather than numerical value example?

(28 points) A stock price is currently S0. Over a period of t years, the price will either go up by U (i.e., S0U) or go down by D (i.e., S0D). The risk-free rate of interest is R per annum with continuous compounding. Consider a European option on this stock expiring after t years with a strike price of K and SD

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock