Question: How to do question B 20,000 The controller of Above All Inc. (AA Inc.) provided you with the following selected information related to the 2011

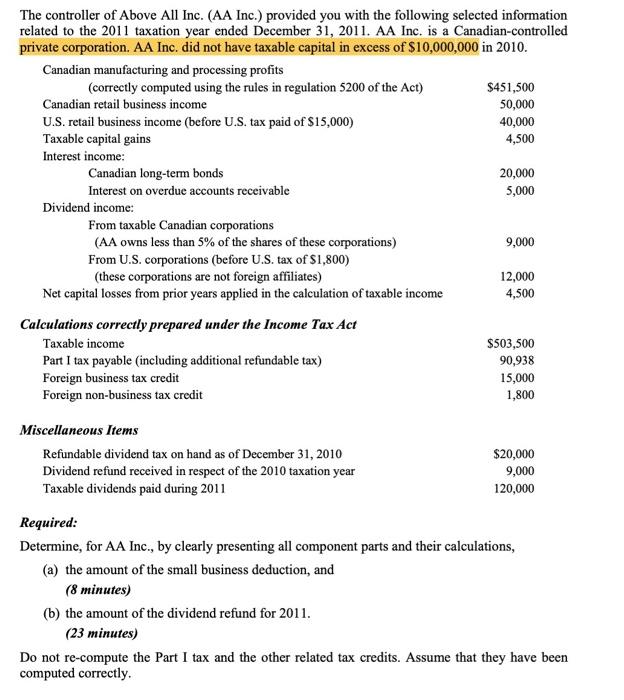

20,000 The controller of Above All Inc. (AA Inc.) provided you with the following selected information related to the 2011 taxation year ended December 31, 2011. AA Inc. is a Canadian-controlled private corporation. AA Inc. did not have taxable capital in excess of $10,000,000 in 2010. Canadian manufacturing and processing profits (correctly computed using the rules in regulation 5200 of the Act) $451,500 Canadian retail business income 50,000 U.S. retail business income (before U.S. tax paid of $15,000) 40,000 Taxable capital gains 4,500 Interest income: Canadian long-term bonds Interest on overdue accounts receivable 5,000 Dividend income: From taxable Canadian corporations (AA owns less than 5% of the shares of these corporations) 9,000 From U.S. corporations (before U.S. tax of $1,800) (these corporations are not foreign affiliates) 12,000 Net capital losses from prior years applied in the calculation of taxable income 4,500 Calculations correctly prepared under the Income Tax Act Taxable income $503,500 Part I tax payable (including additional refundable tax) 90,938 Foreign business tax credit 15,000 Foreign non-business tax credit 1,800 Miscellaneous Items Refundable dividend tax on hand as of December 31, 2010 Dividend refund received in respect of the 2010 taxation year Taxable dividends paid during 2011 $20,000 9,000 120,000 Required: Determine, for AA Inc., by clearly presenting all component parts and their calculations, (a) the amount of the small business deduction, and (8 minutes) (b) the amount of the dividend refund for 2011. (23 minutes) Do not re-compute the Part I tax and the other related tax credits. Assume that they have been computed correctly

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts