Question: How to solve L 3 . 3 Exercises Exercise 3 . Let ( x , Y ) : s ? be the return rates (

How to solve

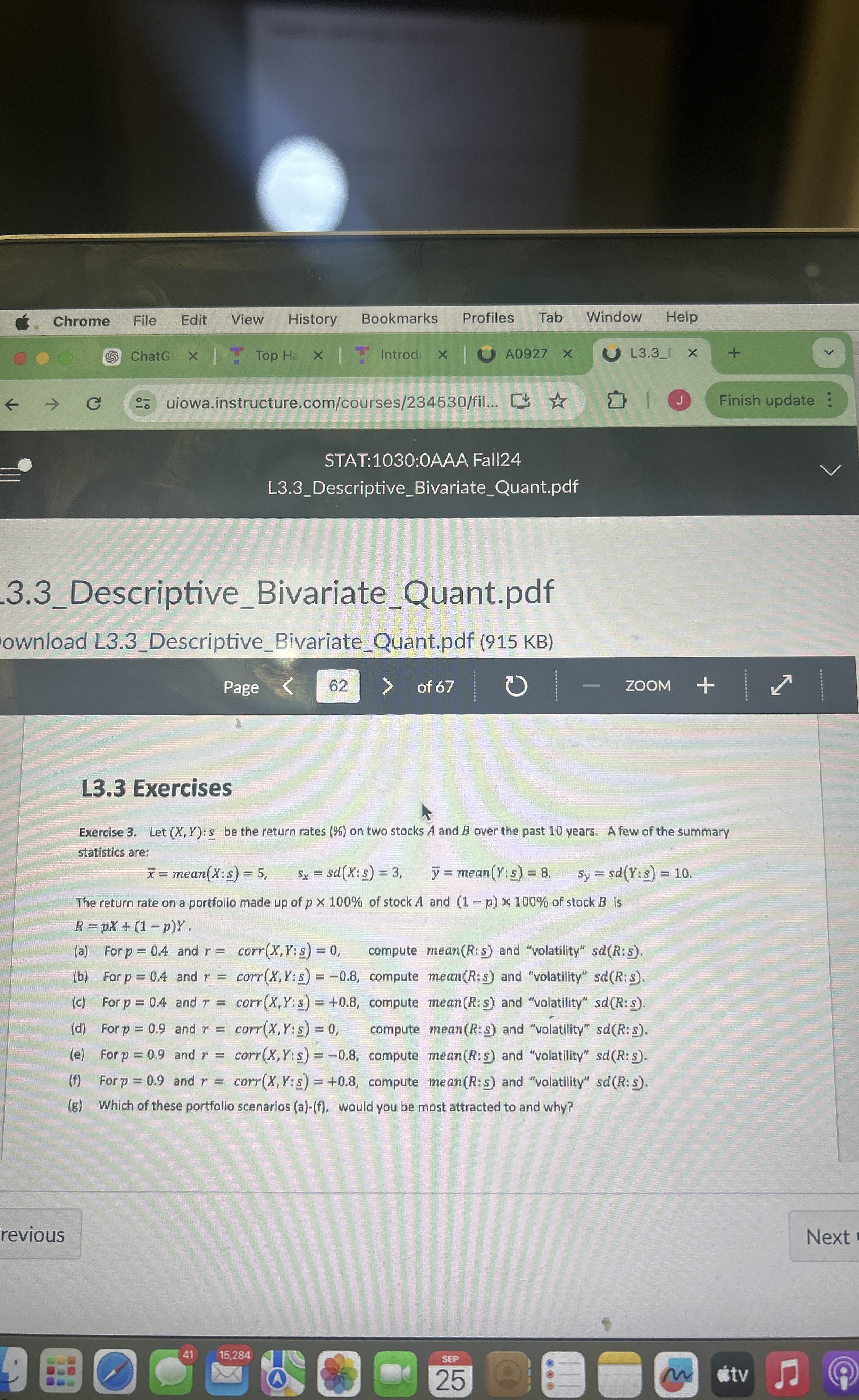

L Exercises

Exercise Let : be the return rates on two stocks A and over the past years. A few of the summary

statistics are:

The return rate on a portfolio made up of of stock A and of stock is

a For and compute mean and "volatility"

b For and compute meanR: and "volatility"

c For and compute mean and "volatility"

d For and compute mean and "volatility"

e For and compute mean and "volatility"

f For and compute mean and "volatility" :

g Which of these portfolio scenarios af would you be most attracted to and why?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock