Question: how to solve part one Problem 11 Intro You have $7,000 and want to invest it in the two stocks below and the risk-free asset,

how to solve part one

how to solve part one

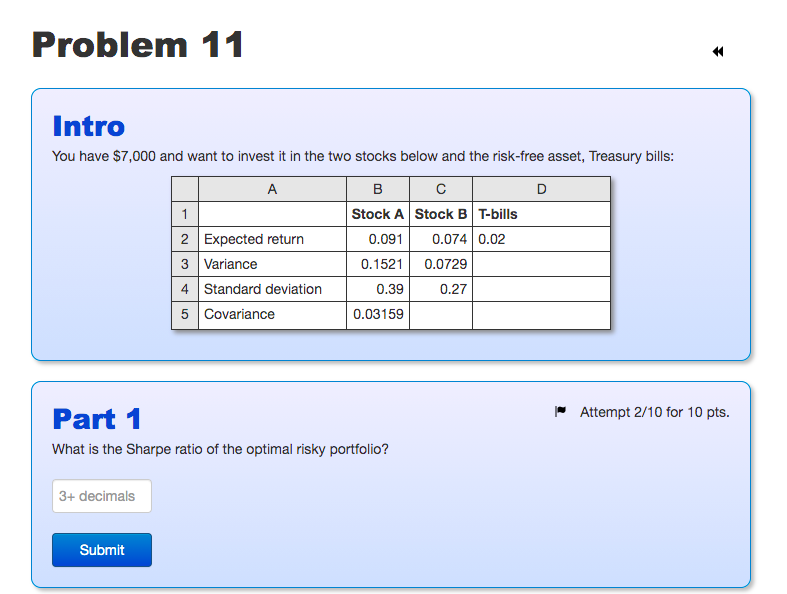

Problem 11 Intro You have $7,000 and want to invest it in the two stocks below and the risk-free asset, Treasury bills: A B D 1 Stock A Stock B T-bills 2 Expected return 0.091 0.074 0.02 3 Variance 0.1521 0.0729 4 Standard deviation 0.39 0.27 5 Covariance 0.03159 Attempt 2/10 for 10 pts. Part 1 What is the Sharpe ratio of the optimal risky portfolio? 3+ decimals Submit

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock