Question: How would I compute this? I believe that this question is the one I keep getting wrong and I think that the answer I have

How would I compute this? I believe that this question is the one I keep getting wrong and I think that the answer I have selected for this question is incorrect.

How would I compute this? I believe that this question is the one I keep getting wrong and I think that the answer I have selected for this question is incorrect.

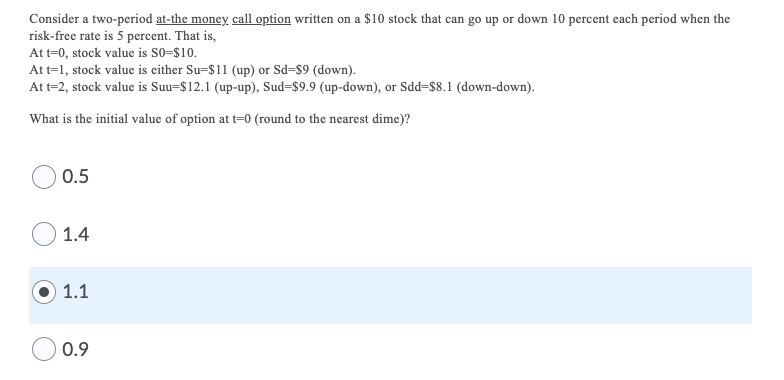

Consider a two-period at-the money call option written on a $10 stock that can go up or down 10 percent each period when the risk-free rate is 5 percent. That is, At t=0, stock value is So=$10. At t=1, stock value is either Su=$11 (up) or Sd=$9 (down). At t=2, stock value is Suu=$12.1 (up-up), Sud=$9.9 (up-down), or Sdd=$8.1 (down-down). What is the initial value of option at t=0 (round to the nearest dime)? 0.5 1.4 1.1 0.9

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock