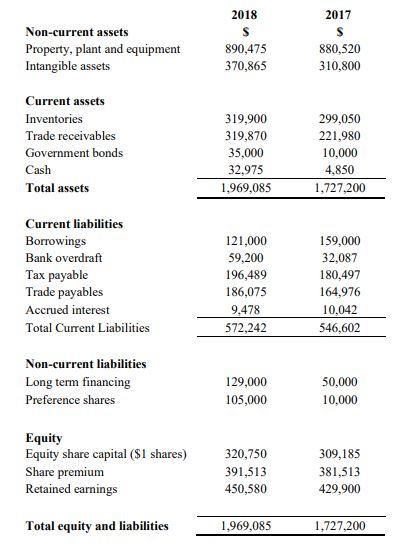

Question: How would the cash flow statement look like? 2018 Non-current assets Property, plant and equipment Intangible assets 890,475 370,865 2017 S 880,520 310,800 Current assets

How would the cash flow statement look like?

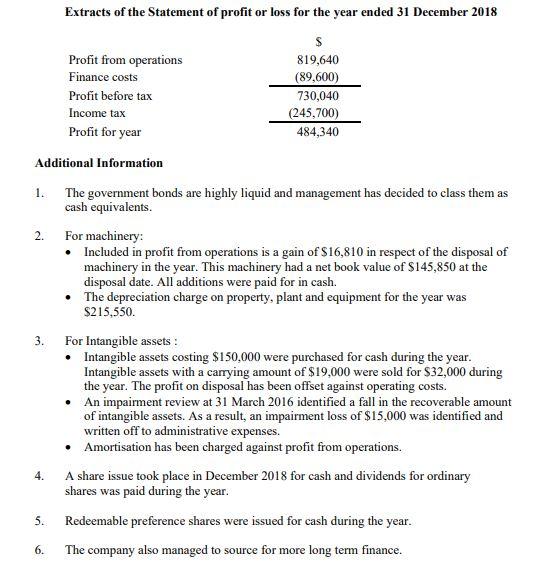

2018 Non-current assets Property, plant and equipment Intangible assets 890,475 370,865 2017 S 880,520 310,800 Current assets Inventories Trade receivables Government bonds Cash Total assets 319,900 319,870 35,000 32,975 1,969,085 299,050 221.980 10,000 4,850 1,727,200 Current liabilities Borrowings Bank overdraft Tax payable Trade payables Accrued interest Total Current Liabilities 121,000 59,200 196,489 186,075 9.478 572,242 159,000 32,087 180,497 164,976 10,042 546,602 Non-current liabilities Long term financing Preference shares 129,000 105,000 50,000 10,000 Equity Equity share capital ($1 shares) Share premium Retained earnings 320,750 391,513 450,580 309,185 381,513 429,900 Total equity and liabilities 1,969,085 1.727,200 Extracts of the Statement of profit or loss for the year ended 31 December 2018 $ Profit from operations 819,640 Finance costs (89,600) Profit before tax 730,040 Income tax (245,700) Profit for year 484,340 2. 3. Additional Information 1. The government bonds are highly liquid and management has decided to class them as cash equivalents. For machinery: Included in profit from operations is a gain of $16,810 in respect of the disposal of machinery in the year. This machinery had a net book value of $145,850 at the disposal date. All additions were paid for in cash. The depreciation charge on property, plant and equipment for the year was $215,550. For Intangible assets: Intangible assets costing $150,000 were purchased for cash during the year. Intangible assets with a carrying amount of $19,000 were sold for $32,000 during the year. The profit on disposal has been offset against operating costs. An impairment review at 31 March 2016 identified a fall in the recoverable amount of intangible assets. As a result, an impairment loss of $15,000 was identified and written off to administrative expenses. Amortisation has been charged against profit from operations. A share issue took place in December 2018 for cash and dividends for ordinary shares was paid during the year. Redeemable preference shares were issued for cash during the year. The company also managed to source for more long term finance. 5. 6

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts