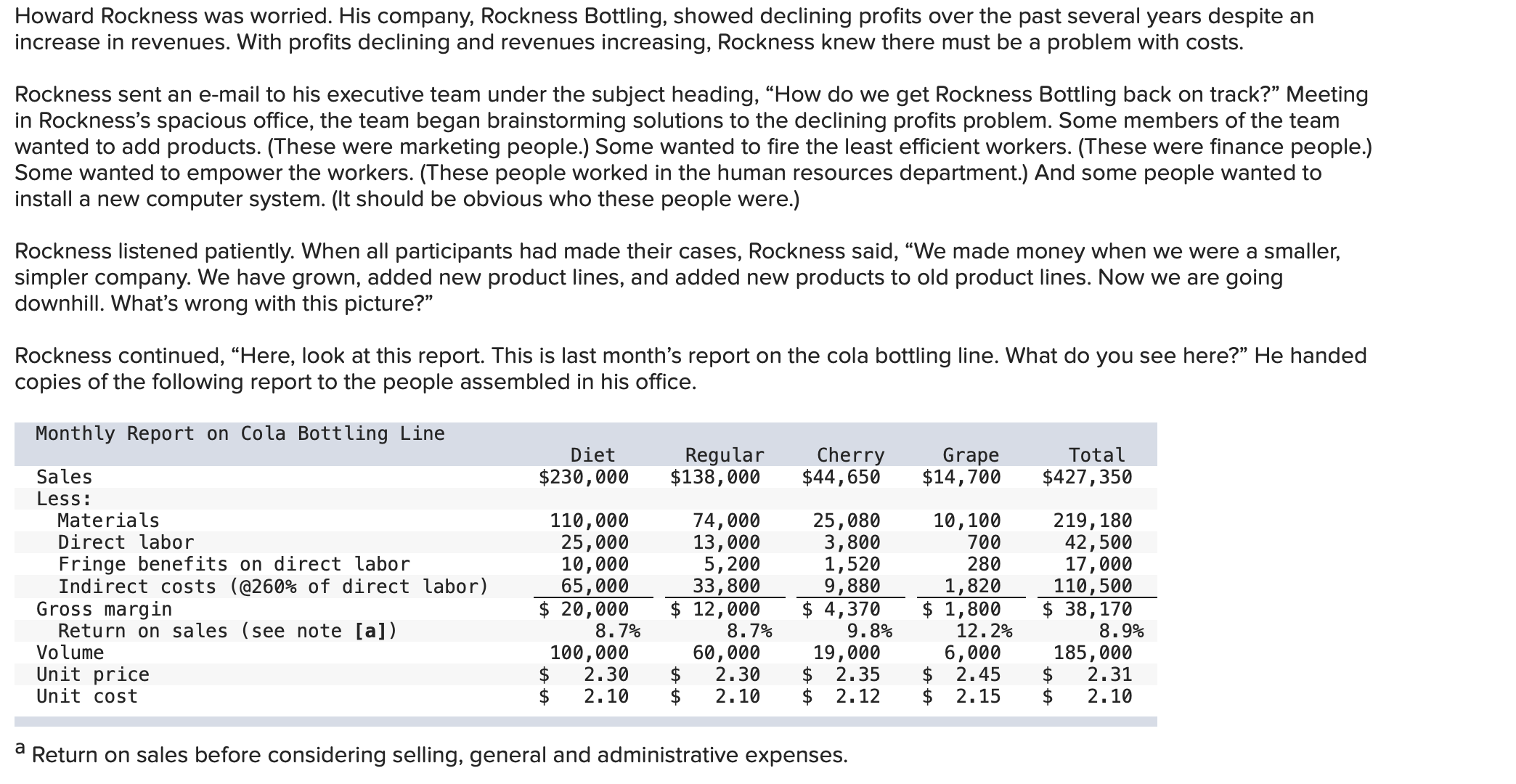

Howard Rockness was worried. His company, Rockness Bottling, showed declining profits over the past several years...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

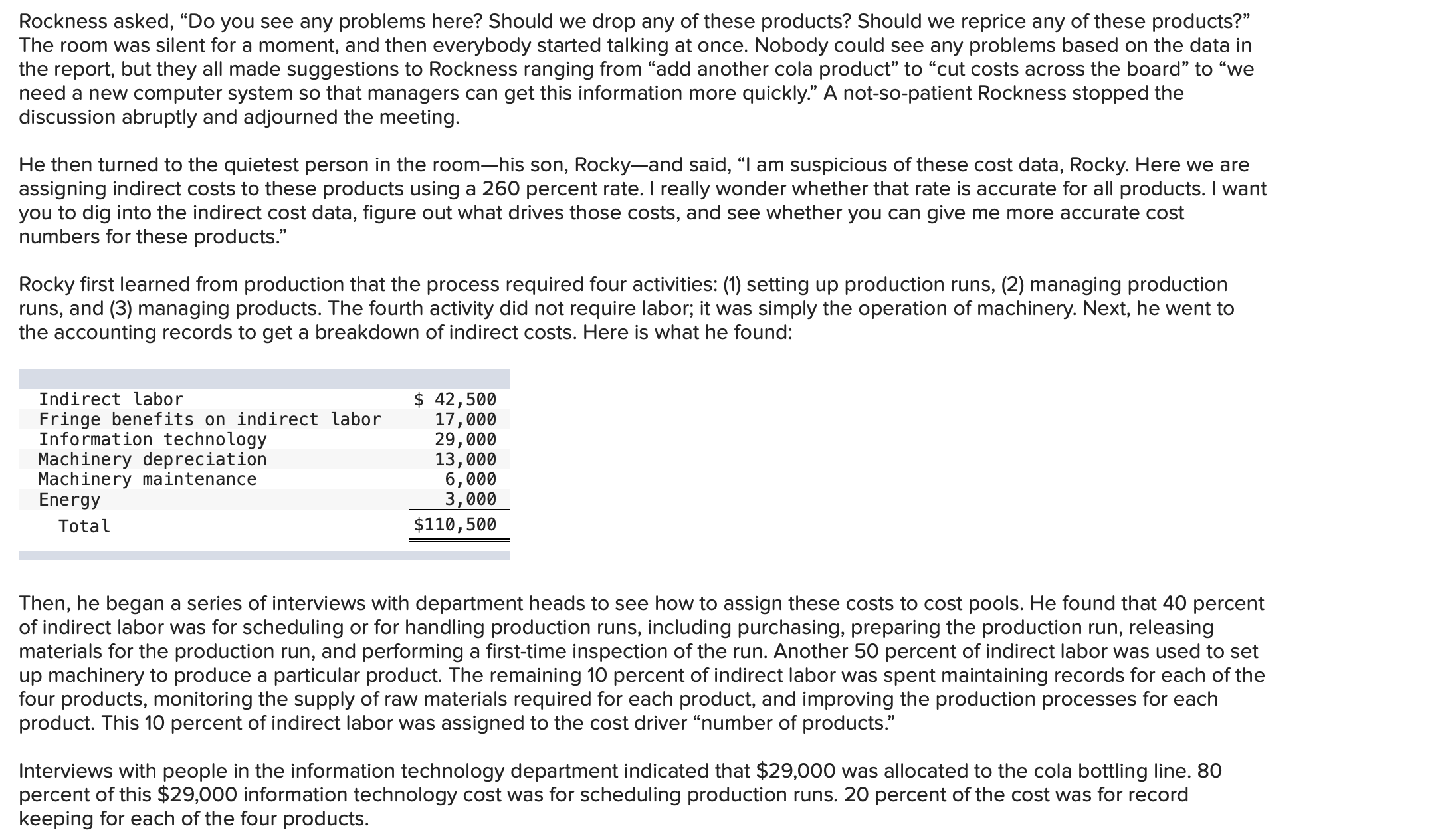

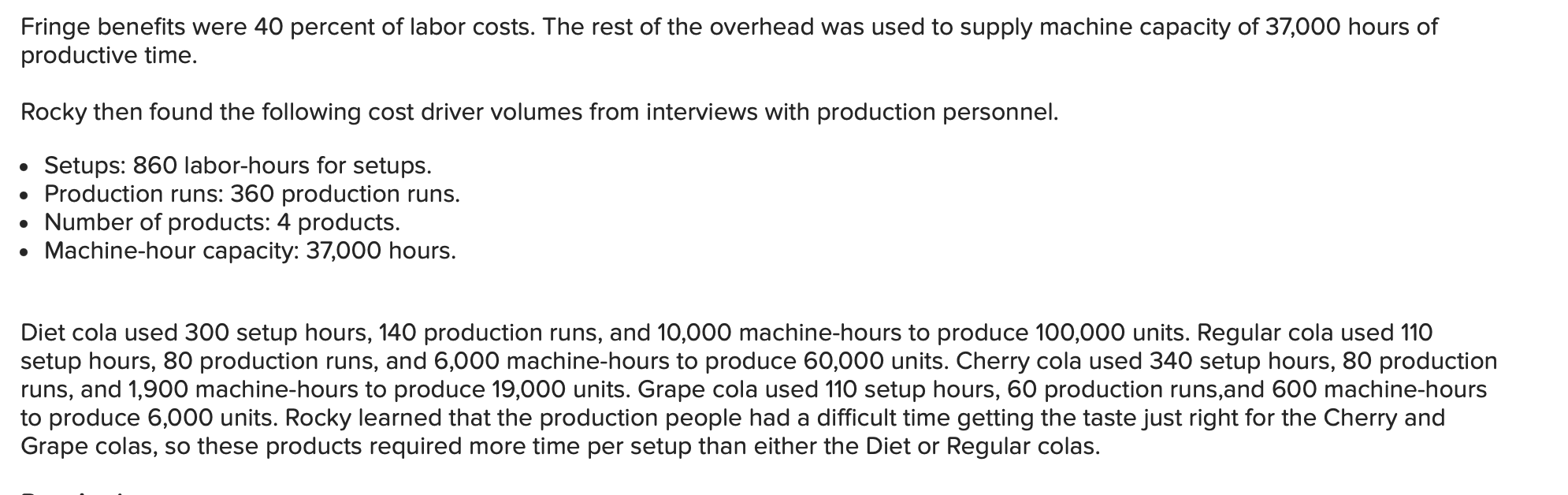

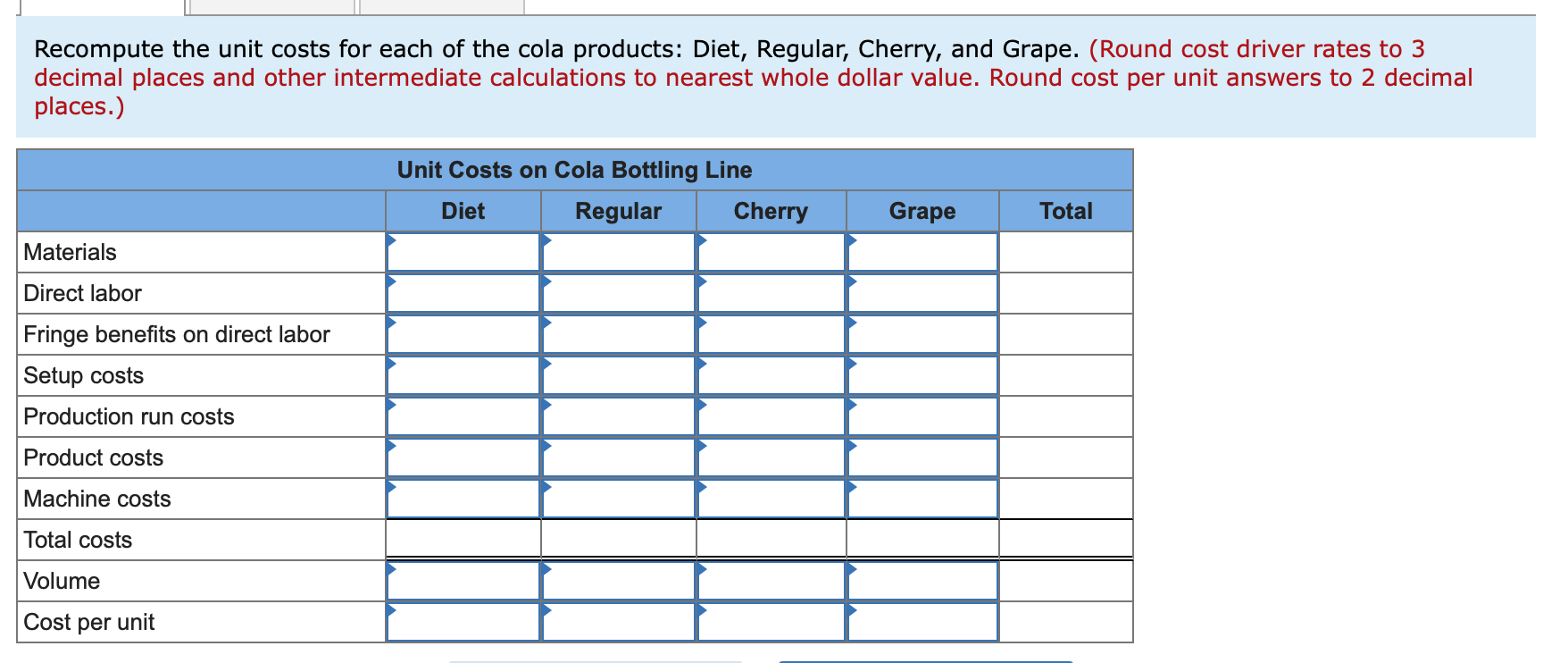

Howard Rockness was worried. His company, Rockness Bottling, showed declining profits over the past several years despite an increase in revenues. With profits declining and revenues increasing, Rockness knew there must be a problem with costs. Rockness sent an e-mail to his executive team under the subject heading, "How do we get Rockness Bottling back on track? Meeting in Rockness's spacious office, the team began brainstorming solutions to the declining profits problem. Some members of the team wanted to add products. (These were marketing people.) Some wanted to fire the least efficient workers. (These were finance people.) Some wanted to empower the workers. (These people worked in the human resources department.) And some people wanted to install a new computer system. (It should be obvious who these people were.) Rockness listened patiently. When all participants had made their cases, Rockness said, We made money when we were a smaller, simpler company. We have grown, added new product lines, and added new products to old product lines. Now we are going downhill. What's wrong with this picture?" Rockness continued, Here, look at this report. This is last month's report on the cola bottling line. What do you see here?" He handed copies of the following report to the people assembled in his office. Monthly Report on Cola Bottling Line Sales Diet $230,000 Regular $138,000 Cherry $44,650 Grape $14,700 Total $427,350 Less: Materials Direct labor Fringe benefits on direct labor Indirect costs (@260% of direct labor) Gross margin Return on sales (see note [a]) 110,000 74,000 25,080 10,100 219,180 25,000 13,000 3,800 700 42,500 10,000 5,200 1,520 280 65,000 33,800 9,880 1,820 17,000 110,500 $ 20,000 Volume 8.7% 100,000 60,000 $ 12,000 8.7% $ 4,370 9.8% 19,000 $ 1,800 $ 38,170 12.2% 6,000 8.9% 185,000 Unit price 2.30 $ 2.30 Unit cost $ 2.10 $ 2.10 $ 2.35 2.12 $ 2.45 $ 2.31 $ 2.15 $ 2.10 a Return on sales before considering selling, general and administrative expenses. Rockness asked, Do you see any problems here? Should we drop any of these products? Should we reprice any of these products?" The room was silent for a moment, and then everybody started talking at once. Nobody could see any problems based on the data in the report, but they all made suggestions to Rockness ranging from add another cola product to cut costs across the board" to "we need a new computer system so that managers can get this information more quickly." A not-so-patient Rockness stopped the discussion abruptly and adjourned the meeting. He then turned to the quietest person in the roomhis son, Rockyand said, I am suspicious of these cost data, Rocky. Here we are assigning indirect costs to these products using a 260 percent rate. I really wonder whether that rate is accurate for all products. I want you to dig into the indirect cost data, figure out what drives those costs, and see whether you can give me more accurate cost numbers for these products." Rocky first learned from production that the process required four activities: (1) setting up production runs, (2) managing production runs, and (3) managing products. The fourth activity did not require labor; it was simply the operation of machinery. Next, he went to the accounting records to get a breakdown of indirect costs. Here is what he found: Indirect labor Fringe benefits on indirect labor Information technology Machinery depreciation Machinery maintenance Energy Total $ 42,500 17,000 29,000 13,000 6,000 3,000 $110,500 Then, he began a series of interviews with department heads to see how to assign these costs to cost pools. He found that 40 percent of indirect labor was for scheduling or for handling production runs, including purchasing, preparing the production run, releasing materials for the production run, and performing a first-time inspection of the run. Another 50 percent of indirect labor was used to set up machinery to produce a particular product. The remaining 10 percent of indirect labor was spent maintaining records for each of the four products, monitoring the supply of raw materials required for each product, and improving the production processes for each product. This 10 percent of indirect labor was assigned to the cost driver "number of products." Interviews with people in the information technology department indicated that $29,000 was allocated to the cola bottling line. 80 percent of this $29,000 information technology cost was for scheduling production runs. 20 percent of the cost was for record keeping for each of the four products. Fringe benefits were 40 percent of labor costs. The rest of the overhead was used to supply machine capacity of 37,000 hours of productive time. Rocky then found the following cost driver volumes from interviews with production personnel. Setups: 860 labor-hours for setups. Production runs: 360 production runs. Number of products: 4 products. Machine-hour capacity: 37,000 hours. Diet cola used 300 setup hours, 140 production runs, and 10,000 machine-hours to produce 100,000 units. Regular cola used 110 setup hours, 80 production runs, and 6,000 machine-hours to produce 60,000 units. Cherry cola used 340 setup hours, 80 production runs, and 1,900 machine-hours to produce 19,000 units. Grape cola used 110 setup hours, 60 production runs,and 600 machine-hours to produce 6,000 units. Rocky learned that the production people had a difficult time getting the taste just right for the Cherry and Grape colas, so these products required more time per setup than either the Diet or Regular colas. Recompute the unit costs for each of the cola products: Diet, Regular, Cherry, and Grape. (Round cost driver rates to 3 decimal places and other intermediate calculations to nearest whole dollar value. Round cost per unit answers to 2 decimal places.) Materials Direct labor Fringe benefits on direct labor Setup costs Production run costs Product costs Machine costs Total costs Volume Cost per unit Unit Costs on Cola Bottling Line Diet Regular Cherry Grape Total What is the cost of unused capacity? Cost of the unused capacity Now assume that Rockness is considering producing a fifth product: Vanilla cola. Because Vanilla cola is in high demand in Rockness Bottling's market, assume that it would use 18,500 hours of machine time to make 185,000 units. (Recall that the machine capacity in this case is 37,000 hours, while Diet, Regular, Cherry, and Grape consume only 18,500 hours.) Vanilla cola's per unit costs would be identical to those of Diet cola except for the machine usage costs. What would be the cost of Vanilla cola? Calculate on a per-unit basis, and then in total. (Do not round intermediate calculations. Round "Per unit" to 5 decimal places.) Cost of vanilla cola per unit Total cost of vanilla cola produced Show less Howard Rockness was worried. His company, Rockness Bottling, showed declining profits over the past several years despite an increase in revenues. With profits declining and revenues increasing, Rockness knew there must be a problem with costs. Rockness sent an e-mail to his executive team under the subject heading, "How do we get Rockness Bottling back on track? Meeting in Rockness's spacious office, the team began brainstorming solutions to the declining profits problem. Some members of the team wanted to add products. (These were marketing people.) Some wanted to fire the least efficient workers. (These were finance people.) Some wanted to empower the workers. (These people worked in the human resources department.) And some people wanted to install a new computer system. (It should be obvious who these people were.) Rockness listened patiently. When all participants had made their cases, Rockness said, We made money when we were a smaller, simpler company. We have grown, added new product lines, and added new products to old product lines. Now we are going downhill. What's wrong with this picture?" Rockness continued, Here, look at this report. This is last month's report on the cola bottling line. What do you see here?" He handed copies of the following report to the people assembled in his office. Monthly Report on Cola Bottling Line Sales Diet $230,000 Regular $138,000 Cherry $44,650 Grape $14,700 Total $427,350 Less: Materials Direct labor Fringe benefits on direct labor Indirect costs (@260% of direct labor) Gross margin Return on sales (see note [a]) 110,000 74,000 25,080 10,100 219,180 25,000 13,000 3,800 700 42,500 10,000 5,200 1,520 280 65,000 33,800 9,880 1,820 17,000 110,500 $ 20,000 Volume 8.7% 100,000 60,000 $ 12,000 8.7% $ 4,370 9.8% 19,000 $ 1,800 $ 38,170 12.2% 6,000 8.9% 185,000 Unit price 2.30 $ 2.30 Unit cost $ 2.10 $ 2.10 $ 2.35 2.12 $ 2.45 $ 2.31 $ 2.15 $ 2.10 a Return on sales before considering selling, general and administrative expenses. Rockness asked, Do you see any problems here? Should we drop any of these products? Should we reprice any of these products?" The room was silent for a moment, and then everybody started talking at once. Nobody could see any problems based on the data in the report, but they all made suggestions to Rockness ranging from add another cola product to cut costs across the board" to "we need a new computer system so that managers can get this information more quickly." A not-so-patient Rockness stopped the discussion abruptly and adjourned the meeting. He then turned to the quietest person in the roomhis son, Rockyand said, I am suspicious of these cost data, Rocky. Here we are assigning indirect costs to these products using a 260 percent rate. I really wonder whether that rate is accurate for all products. I want you to dig into the indirect cost data, figure out what drives those costs, and see whether you can give me more accurate cost numbers for these products." Rocky first learned from production that the process required four activities: (1) setting up production runs, (2) managing production runs, and (3) managing products. The fourth activity did not require labor; it was simply the operation of machinery. Next, he went to the accounting records to get a breakdown of indirect costs. Here is what he found: Indirect labor Fringe benefits on indirect labor Information technology Machinery depreciation Machinery maintenance Energy Total $ 42,500 17,000 29,000 13,000 6,000 3,000 $110,500 Then, he began a series of interviews with department heads to see how to assign these costs to cost pools. He found that 40 percent of indirect labor was for scheduling or for handling production runs, including purchasing, preparing the production run, releasing materials for the production run, and performing a first-time inspection of the run. Another 50 percent of indirect labor was used to set up machinery to produce a particular product. The remaining 10 percent of indirect labor was spent maintaining records for each of the four products, monitoring the supply of raw materials required for each product, and improving the production processes for each product. This 10 percent of indirect labor was assigned to the cost driver "number of products." Interviews with people in the information technology department indicated that $29,000 was allocated to the cola bottling line. 80 percent of this $29,000 information technology cost was for scheduling production runs. 20 percent of the cost was for record keeping for each of the four products. Fringe benefits were 40 percent of labor costs. The rest of the overhead was used to supply machine capacity of 37,000 hours of productive time. Rocky then found the following cost driver volumes from interviews with production personnel. Setups: 860 labor-hours for setups. Production runs: 360 production runs. Number of products: 4 products. Machine-hour capacity: 37,000 hours. Diet cola used 300 setup hours, 140 production runs, and 10,000 machine-hours to produce 100,000 units. Regular cola used 110 setup hours, 80 production runs, and 6,000 machine-hours to produce 60,000 units. Cherry cola used 340 setup hours, 80 production runs, and 1,900 machine-hours to produce 19,000 units. Grape cola used 110 setup hours, 60 production runs,and 600 machine-hours to produce 6,000 units. Rocky learned that the production people had a difficult time getting the taste just right for the Cherry and Grape colas, so these products required more time per setup than either the Diet or Regular colas. Recompute the unit costs for each of the cola products: Diet, Regular, Cherry, and Grape. (Round cost driver rates to 3 decimal places and other intermediate calculations to nearest whole dollar value. Round cost per unit answers to 2 decimal places.) Materials Direct labor Fringe benefits on direct labor Setup costs Production run costs Product costs Machine costs Total costs Volume Cost per unit Unit Costs on Cola Bottling Line Diet Regular Cherry Grape Total What is the cost of unused capacity? Cost of the unused capacity Now assume that Rockness is considering producing a fifth product: Vanilla cola. Because Vanilla cola is in high demand in Rockness Bottling's market, assume that it would use 18,500 hours of machine time to make 185,000 units. (Recall that the machine capacity in this case is 37,000 hours, while Diet, Regular, Cherry, and Grape consume only 18,500 hours.) Vanilla cola's per unit costs would be identical to those of Diet cola except for the machine usage costs. What would be the cost of Vanilla cola? Calculate on a per-unit basis, and then in total. (Do not round intermediate calculations. Round "Per unit" to 5 decimal places.) Cost of vanilla cola per unit Total cost of vanilla cola produced Show less

Expert Answer:

Posted Date:

Students also viewed these accounting questions

-

Howard Rockness was worried. His company, Rockness Bottling, showed declining profits over the past several years despite an increase in revenues. With profits declining and revenues increasing,...

-

Managing Scope Changes Case Study Scope changes on a project can occur regardless of how well the project is planned or executed. Scope changes can be the result of something that was omitted during...

-

An examiners close inspection of the annual financial statements and the accounting records revealed that Mawani Inc. may have violated some accounting principles. The examiner questioned the...

-

As a group, develop your promotional objectives. What are the initial objectives of your promotional campaign? Will these change over time?

-

Magnetic field values are often determined by using a device known as a search coil. This technique depends on the measurement of the total charge passing through a coil in a time interval during...

-

Use the data for Great Gadget, Inc., from 4-32B. Requirements 1. Prepare Great Gadgets multi-step income statement. 2. Calculate the gross profit percentage. 3. The gross profit percentage for 2009...

-

1. How serious were the alleged accounting misstatements? As part of your answer, consider whether they were material and whether they were fraudulent. 2. Suppose you were defending Mr. Rand. Could...

-

Exercise 13-12 (Algo) Volume Trade-Off Decisions [LO13-5] Benoit Company produces three products-A, B, and C. Data concerning the three products follow (per unit): Selling price Variable expenses:...

-

In the analyses of Karl Marx and Hardt, how do they articulate the intricate interrelationship between labor dynamics and political frameworks?"

-

What are the essential points to be included in the accountant's report on the review of the financial statements of a nonpublic entity?

-

Identify the four circumstances in which the CPA may report on internal accounting control.

-

a. Indicate the nature of additional information that an auditor may submit with his audit report. b. How does the auditor indicate the responsibility he is taking for the additional information? c....

-

What two types of procedures are generally involved in the performance of a review service?

-

Enumerate the elements that should be included in a report on interim financial information (IFI) for a public entity.

-

A) Using the Easton Model of the political system to assist you in illustrating and clarifying the approaches that you discuss. Compare the domestic political environment and how it differs from the...

-

Suppose the market is semistrong form efficient. Can you expect to earn excess returns if you make trades based on? a. Your brokers information about record earnings for a stock? b. Rumors about a...

-

How does a firms corporate strategy affect its operations management?

-

How do production management and service operations management differ?

-

What basic set of factors must a firm consider when selecting a location for a production facility?

Study smarter with the SolutionInn App